FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

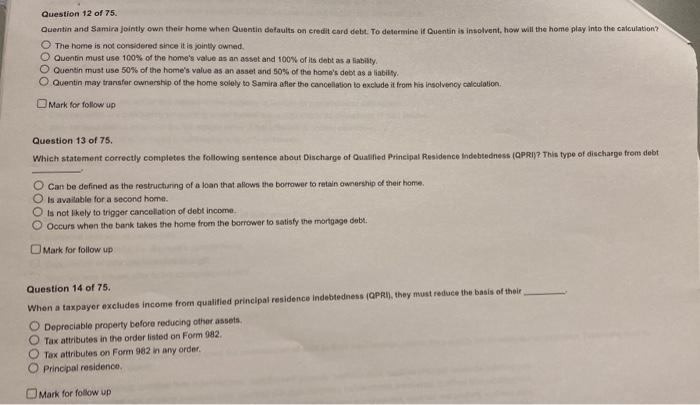

Transcribed Image Text:Question 12 of 75.

Quentin and Samira jointly own their home when Quentin defaults on eredit card debe To determine if Duentin is insolvent, how will the home play into the calculation?

O The home is not considered since it is jointly owned.

O Quentin must use 100% of the home's value as an asset and 100% of its debt as a labilty.

O Quentin must use 50% of the home's value as an asset and 50% of the home's debt as a liability.

O Quentin may transfer ownership of the home solely to Samira after the cancellation to exclude it from his insolvency caliculation.

OMark for follow up

Question 13 of 75.

Which statement correctly completes the following sentence about Discharge of Qualified Principal Residence Indebtedness (QPRI)? This type of discharge from debt

O Can be defined as the restructuring of a loan that allown the borrower to retain ownership of their home.

O is available for a second home.

O is not likely to trigger cancellation of debt income.

O Occurs when the bank takes the home from the borrower to satisfy the mortgage debt.

OMark for follow up

Question 14 of 75.

When a taxpayer excludes income from qualified principal residence indebtedness (QPRI), they must reduce the basis of their

Depreciable property before reducing other assets.

O Tax attributes in the order listed on Form 982.

Tax attributes on Form 982 in any order.

Principal residence.

OMark for folow up

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Question 27 of 50. Mark and Carrie are married, and they will file a joint return. They both work full-time, and their 2021 income totaled $89,000, all from wages. They have one dependent child, Aubrey (5). During the year, they spent $9,000 for Aubrey's child care. Neither Mark nor Carrie received any dependent care benefits from their employer. What amount may they use to calculate the Child and Dependent Care Credit? $0 $3,000 $8,000 $9,000 Mark for follow uparrow_forwardV1arrow_forwardAgnes transfers a four-apartment investment condominium subject to a non-recourse mortgage to Brad. Brad, in return, transfers to Agnes a residential rental apartment building subject to a non-recourse mortgage. Agnes's condo cost $500,000 and she has taken depreciation of $25,000. The amount of the non-recourse debt is $475,000. The fair market value of the condo is $600,000. Brad's apartment building cost $700,000 and has a current fair market value of $600,000. He has taken depreciation deductions of $100,000 and the amount of the non-recourse debt is $600,000. As a result of this exchange transaction Brad has received boot of $125,000. Agnes has received boot of $125,000. Brad has given up boot of $125,000. Agnes has given up boot of $475,000.arrow_forward

- Joyce is a widowed taxpayer whose husband Willard passed away on March 31, 2020. Joyce and Willard had purchased a home for $215,000 on September 12, 2004, lived in the home as their main home until Willard's death. Joyce moved in with her daughter after Willard's death, and sold the home on November 30, 2020 , for $595,000. How much of the gain on the sale can Joyce exclude from taxable income? Select one: O a. $500,000, the maximum exclusion for an unmarried surviving spouse O b. $380,000, the amount of gain on the sale of the home O C. $250,000, the maximum exclusion amount for a single taxpayer O d. $0, because she moved out before she sold the homearrow_forwardProblem 13-84 (LO. 8, 9) Karl purchased his residence on January 2, 2019, for $260,000, after having lived in it during 2018 as a tenant under a lease with an option to buy clause. On August 1, 2020, Karl sells the residence for $315,000. On June 13, 2020, Karl purchases a new residence for $367,000. If an amount is zero, enter "0". a. What is Karl's recognized gain? His basis for the new residence?Karl's recognized gain is $fill in the blank aa8a5403c02a012_1, and his basis for the new residence is $fill in the blank aa8a5403c02a012_2. b. Assume that Karl purchased his original residence on January 2, 2018 (rather than January 2, 2019). What is Karl's recognized gain? His basis for the new residence? Karl's recognized gain is $fill in the blank f8cfe3ffcff0ffc_1, and his basis for the new residence is $fill in the blank f8cfe3ffcff0ffc_2. c. In part (a), what could Karl do to minimize his recognized gain?To minimize his recognized gain, he can continue to…arrow_forwardGodoarrow_forward

- 2Aarrow_forwardHarold and Kumar own a tax preparation business that they value at 1,000,000 based on their latest official valuation which includes $ 500,000 of real property. They are purchasing life insurance to fund their buy /sell agreement as neither one wants to work with the other one's spouse. The amount of life insurance that they should purchase on each other is? A. $250,000 each B. $500,000 each $1,000,000 each D. Nonearrow_forward(Case Study Question) Henry's oldest son has few financial resources. Henry would like to contribute annually to a trust, with his son only receiving the trust income. The remainder of the trust would go to his grandchildren (his son's children) at his son's death. Henry wants his son to receive all the earnings from the trust with no restrictions. He realizes that his son will likely squander trust income he receives but wants to otherwise protect his son from his creditors. Which of the following trusts would you recommend that Henry establish for the benefit of his son? A) An irrevocable trust, including spendthrift provisions B) A support trust C) A Section 2503(b) trustarrow_forward

- Nonearrow_forward18 Sandy is seeking child support under the Divorce Act from her former husband, Raymond. Her daughter, Kalia is a normal healthy child who attends daycare while Sandy works. Sandy hopes that the court will order an amount in addition to the basic amount to help her defray some of her unique expenses. Which of the following purchases or expenses may result in Raymond having to pay an amount greater than the basic amount under the federal Child Support Guidelines? a) expenses for Kalia's daycare b) Kalia's new clothes c) the loan on Sandy's new car, which has a built-in car seat for Kalia Od) the child-sized, electric Barbie-mobile that Sandy bought for Kalia's third birthdayarrow_forward6arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education