ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

Textbook Exercises ... please help

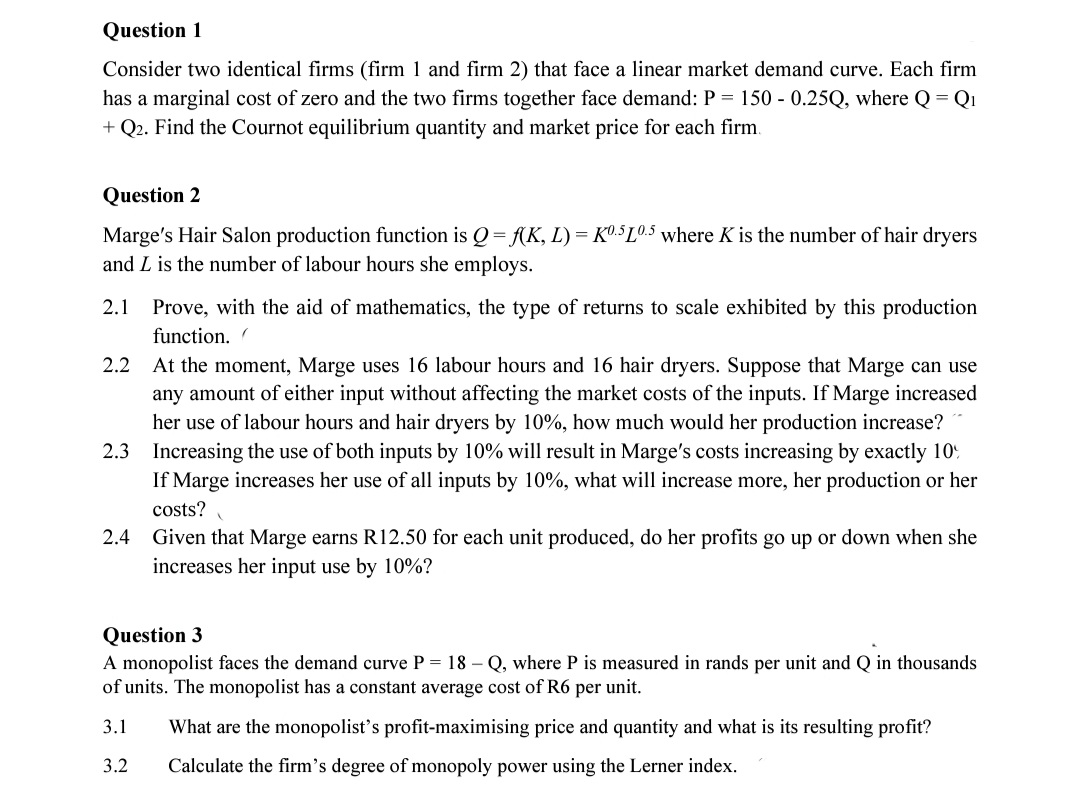

Transcribed Image Text:Question 1

Consider two identical firms (firm 1 and firm 2) that face a linear market demand curve. Each firm

has a marginal cost of zero and the two firms together face demand: P = 150 - 0.25Q, where Q = Q₁

+ Q2. Find the Cournot equilibrium quantity and market price for each firm.

Question 2

Marge's Hair Salon production function is Q = f(K, L) = K0.5 10.5 where K is the number of hair dryers

and L is the number of labour hours she employs.

2.1 Prove, with the aid of mathematics, the type of returns to scale exhibited by this production

function. (

2.2 At the moment, Marge uses 16 labour hours and 16 hair dryers. Suppose that Marge can use

any amount of either input without affecting the market costs of the inputs. If Marge increased

her use of labour hours and hair dryers by 10%, how much would her production increase?

2.3 Increasing the use of both inputs by 10% will result in Marge's costs increasing by exactly 10%

If Marge increases her use of all inputs by 10%, what will increase more, her production or her

costs?

2.4

Given that Marge earns R12.50 for each unit produced, do her profits go up or down when she

increases her input use by 10%?

Question 3

A monopolist faces the demand curve P = 18-Q, where P is measured in rands per unit and Q in thousands

of units. The monopolist has a constant average cost of R6 per unit.

3.1

What are the monopolist's profit-maximising price and quantity and what is its resulting profit?

3.2 Calculate the firm's degree of monopoly power using the Lerner index.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- What is the nature of elasticity?arrow_forward(a)Diagrammatically show and explain how oil prices dropped as concerns over fuel demand in the near term in COVID-19 pandemic hit Europe and the United States. (b)Diagrammatically show and explain what happened to the oil market if the price remained unchanged despite the concerns over the fuel demand. (c)You sell two different goods: printers and toner cartridges. The price elasticity of demand for the printers is -3.4, and you earn a revenue of RM15,000 per month from the good. You earn a revenue of RM5,000 per month from the toner cartridges. The cross price elasticity of demand for both of the goods is -2.5. If you decide to decrease the price of the printers by 5%, calculate your new total revenues for…arrow_forwardYpsilanti Market Research conducted a survey to find out whether people who earn more money purchase more expensive goods. The following graph indicates the relationship between income the survey subjects earned and the price of the home that they purchased. PRICE (Thousands of dollars per home) 500 450 400 350 300 250 200 150 100 50 L 0 10 20 30 40 50 60 70 80 INCOME (Thousands of dollars per year) 90 100arrow_forward

- Typed plz and quality solution for up vote and take care of plagiarism alsoarrow_forwardЕОC 6.03 A 45% fall in the price of computers leads to a 20% rise in the amount of computers purchased by customers. Using this information, we would expect total revenue to when prices drop. Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer. decrease increase not change d increase or decrease (not enough information)arrow_forward1) Give an example of a product that is elastic and explain why. 2) Give an example of a product that is inelastic and explain why. Thank you !!arrow_forward

- please help with #4arrow_forwardNile.com, the online bookseller, wants to increase its total revenue. One strategy is to offer a 10% discount on every book it sells. Nile.com knows that its customers can be divided into two distinct groups according to their likely responses to the discount. The accompanying table shows how the two groups respond to the discount. Group A Group B(sales per week) (sales per week) Volume of sales beforethe 10% discount 1.55 million 1.50 million Volume of sales afterthe 10% discount 1.65 million 1.70 million A. Using the midpoint method, calculate the price elasticities of demand for group A and group B. B. Explain how the discount will affect total revenue from each group. C. Suppose Nile.com knows which group each customer belongs to when he or she logs on and can choose whether or not to offer the 10% discount. If Nile.com wants to increase its total revenue, should discounts be offered to group A or to group B, to neither group, or to both groups?arrow_forwardHow is elasticity related to logarithms?arrow_forward

- For each example listed, decide if the good is a normal good or an inferior good. Make sure you answer from the perspective of the individual or individuals doing the buying or consuming. Billy's mom increases his weekly allowance by %5. As a result, Billy increases the number of apps he downloads on his smartphone. Smartphone apps arearrow_forwardWhat are some other examples of elasticity that can be affected by time?arrow_forwardONLY TYPED SOLUTIONarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education