ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

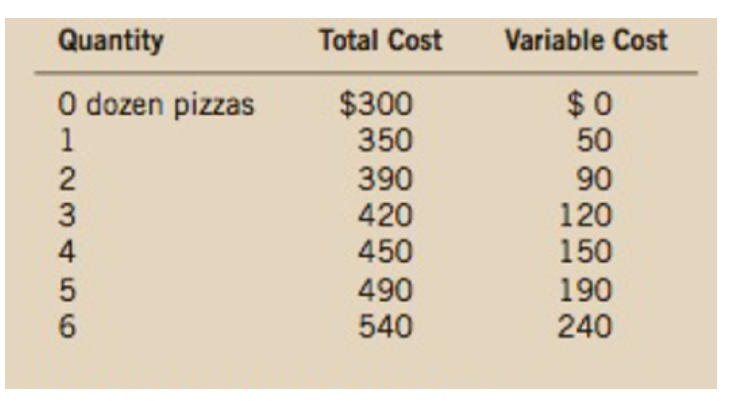

Consider the following cost information for a pizzeria:

a. What is the pizzeria’s fixed cost?

b. Construct a table in which you calculate the marginal cost per dozen pizzas using the information on total cost. Also, calculate the marginal cost per dozen pizzas using the information on variable cost. What is the relationship between these sets of numbers? Explain.

Transcribed Image Text:Quantity

Total Cost

Variable Cost

O dozen pizzas

$0

50

$300

350

390

420

450

90

120

150

490

540

190

240

P123456

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a small photography studio with 8 workers and 5 The total cost of labor and capital is $3,200. In order to reduce total operating costs, the owner leases 5 additional printers and fires 5 workers. After these changes, the salary of each worker increases by $30, the cost of using each of the printers (both new and old) remains constant, and the total cost of labor and capital decreases to $2,900. What is the cost of using one printer?arrow_forwardAssume the following total cost function: Total Cost $75 1 105 128 What is the average fixed cost of producing 2 units? What is the marginal cost of producing 2 units?arrow_forwardUsing the numbers representing short run costs in the chart below, calculate the number that belongs in the blank space. q = quantity, TFC = Total Fixed Cost, TVC = Total Variable Cost, AVC = %3D %3D Average Variable Cost Recall that an "X" in the chart means that no number goes in that space. TFC TVC AVC 300 300 150 75 300 270 135 3. 300 370 123.33 4 300 480 300 650 130 300 840 140 1. 2. 6arrow_forward

- What is the relationship between average variable cost and marginal cost? a) They are always equal b) Marginal cost is always higher than average variable cost c) Marginal cost is always lower than average variable cost d) The relationship varies depending on the production levelarrow_forwardQuestion 6: For each of the total cost functions, write the expressions for the average cost, average fixed cost, average variable cost, and marginal cost: 1. TC (Q) = 5Q 2. TC (Q) = 120 +6Q 3. TC (Q) = 6Q² 4. TC (Q) = 140 +5Q²arrow_forwardCalculate total costs at 4 units of output. Do not put a dollar sign in your answer. (The 6 columns are Quantity, Total Fixed Cost, Total Variable Cost, Total Cost, Average Total Cost, and Marginal Cost. The Quantity and Total Variable Cost columns have been filled in along with the first row for Total Fixed Cost. Average Total Costs and Marginal Costs are not calculated at a quantity of 0.) Quantity Total Fixed Cost Total Variable Cost Total Cost Average Total Cost Marginal Cost 0 15 0 XXXXX XXXXX 1 25 2 40 3 50 4 55 5 65 Calculate average total costs at 2 units of output. Calculate average total cost at 5 units of output. Calculate marginal cost at 4 units of output (moving from 3 units to 4 units). Can you tell if this is the short run or long run? Can you tell at which level of output profits will be maximized?arrow_forward

- Fill in the following cost table. For the first few rows, you can work from left to right. However, as you get to the last two rows, you will need to use the information from the right side of the table to work back to the left side. We do not calculate average costs at a quantity of 0. Q TFC TVC TC AFC AVC ATC MC 0 5,000 0 XXXXXX XXXXXX XXXXXX XXXXXX 1 3.000 3,000 2 5,000 3 11,000 4 3,250 5 4,000 Can you tell if this is the short run or long run? Can you tell which level of output yields the highest profit? If so, what is the output level? If not, explain. Economists define the “Break-even Price” as the lowest point on the average total cost curve or the lowest average total cost given in a table. What is the break-even price in this problem? Economists define the “Shutdown Price” as the…arrow_forwardThe Santa Clara County increases the property taxes for all fast food restaurants. Which cost curves will be affected as a result of this policy? 1. average total cost and average fixed cost. 2. average variable cost and average total cost. 3. average variable cost and marginal cost. 4. average variable cost and average fixed cost.arrow_forwardConsider the following cost function. a. Find the average cost and marginal cost functions. C(x) = 1700 + 0.4x, 1700 +0.4. a. The average cost function is C(x) = The marginal cost function is C'(x) = 0.4|.arrow_forward

- 16. The total cost to make q quilts is C(q) = 73 +1.2q +0.05q2. a. What is a function for the marginal cost? b. Find a quantity that minimizes the average cost.arrow_forwardMarginal cost, average total cost and average variable cost Marginal cost and average total cost are always equal. Do you agree? Explain. If you disagree then write under what situation they are equal. b. Marginal cost and average variable cost are always equal. Do you agree? Explain. If you disagree then write under what situation they are equal.arrow_forwardUse your knowledge of cost functions to calculate the missed cost data in the accompanying table. Round your answers to two digits after the decimal. Quantity Marginal cost Fixed cost Variable cost Total cost Average fixed cost Average variable cost Average total cost 0 --- --- --- --- 1 $50.00$50.00 2 $68.00$68.00 3 $95.00$95.00 4 $50.00$50.00 $360.00$360.00 What is the total cost when producing zero units?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education