ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

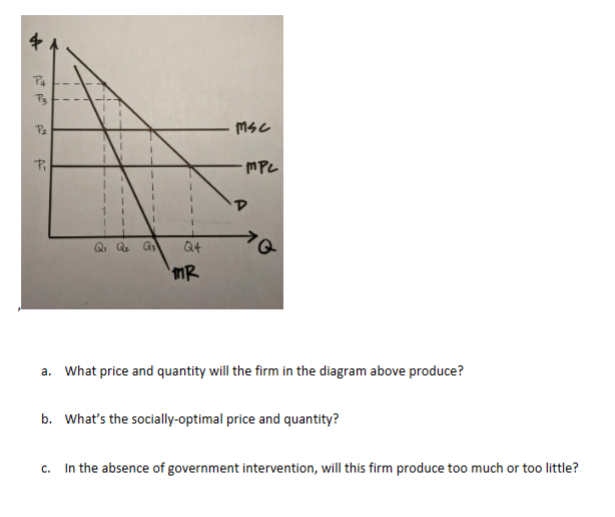

Transcribed Image Text:Pu

P3

P₂

A

Pi

Q₁ Q₂

Q4

MR

MSC

тре

D

10

a. What price and quantity will the firm in the diagram above produce?

b. What's the socially-optimal price and quantity?

c. In the absence of government intervention, will this firm produce too much or too little?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- When we see ______________ on a graph, it is an indication of economic inefficiency. A.High prices B.Deadweight Loss C.High production costsarrow_forwardThe process is _ constrained when _ exceeds _ and the flow rate is equal to the demand rate.A. Demand, supply, demandB. Capacity, supply, demandC. Demand, demand, supplyD. Capacity, demand, supplyarrow_forwardQuestion 2 The government has imposed an effective price control for an agricultural product of $12. The equilibrium price for this market is $8. Ainswer the followving question? a. Describle what type of price control is this? b. Draw the market (demand and supply) for this market and show the price control. c. What are the consequences of this price controlarrow_forward

- 'Qs=35+8p Qd=106-2p' Find equilibrium rice and equilibrium quantityarrow_forwardPrice (dollars per sandwich) 0 | -234 SST 0 5 6 7 Quantity supplied (sandwiches per week) 0 Quantity demanded 400 350 300 250 200 150 100 50 0 5. After the shift in demand, is this market still efficient? Why or why not? 50 100 150 200 250 300 350 400arrow_forward) What happened to supply curve and equilibrium price and quantity when Government provides subsidy to corn grower. Show graphically and explain by using 4 -steps Process.arrow_forward

- Help pleasearrow_forwardpe diagram below shows the market for some agricultural product, X. 6.00 5.00 4.00 3.00 2.00 1.00 300 600 900 1200 1500 1800 Quantity of X (units per week) IGURE 5-8 Refer to Figure 5-8. Assume the market for product X is at its free-market equilibrium. What is the weekly amount of producer surplus in this market? $1800 $2700 $1350 $900 $450arrow_forwardQ20 In Canada we have government intervention in the dairy market in the form of quotas on milk production. What are two predicted economic effects of this policy? a. A redistribution of income from dairy farmers to consumers of dairy products and an increase in the total amount of economic surplus in the dairy market. b. An equitable distribution of income between dairy farmers and consumers of dairy products and a reduction in the total amount of economic surplus in the dairy market. c. A redistribution of income from consumers of dairy products to dairy farmers and a reduction in deadweight loss in the dairy market. d. A redistribution of income from dairy farmers to consumers of dairy products and a reduction in the total amount of economic surplus in the dairy market. e. A redistribution of income from consumers of dairy products to dairy farmers and a reduction in the total amount of economic surplus in the dairy market. Clear my choicearrow_forward

- Marginal cost and marginal benefit (dollars per pound) 5 3 2 - MC M8 100 200 300 400 500 600 Quantity (pounds of coffee perday) The above figure shows the marginal benefit and marginal cost curves of coffee in the nation of Kaffenia. Which of the following would result in the quantity of coffee in Kaffenia differing from the efficient quantity? O The existence of price control in the market. The existence of many producers and sellers of coffee. The existence of a single producer and seller of coffee. Both "The existence of a single producer and seller of coffee." and "The existence of price control in the market." are correct.arrow_forwardAs prices rise, why will producers increase production of a product? O They are required to by law. O They are spending less money on resources. O They want to decrease the volume of sales. O They want to obtain higher profits. vc.k12.com/learnx-svc/getIndex/token/6241afc7ef9a221020a640c5_a5107a05-ec20-47e8-bf05-9a035c6efc38/conceptld/HST MAR 1 28 MacBook Ai 000 D00 FA F1 F2 F3 # 2$ % %24arrow_forwardExtra Problems - I - In a given market the supply curve is based on the following: producers an suppy at a price of 10 up to a quantity of 100. No more than 100 can be applied. Producers will not supply if price is below 10. The demand curve QD=A-20p. Graph the supply curve and interpret it. . Now determine A such that the market "just exists" - this the smallest value of A such that an infinitesimal amount will be sold. You can use graphs to help with this; for example, graph the demand curve for a given guess at A and see whether or not the market exists. . Determine the range of values of A for which the market "maxes out" and the maximum feasible amount is sold.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education