FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

Need help with this two part question. Thank you!

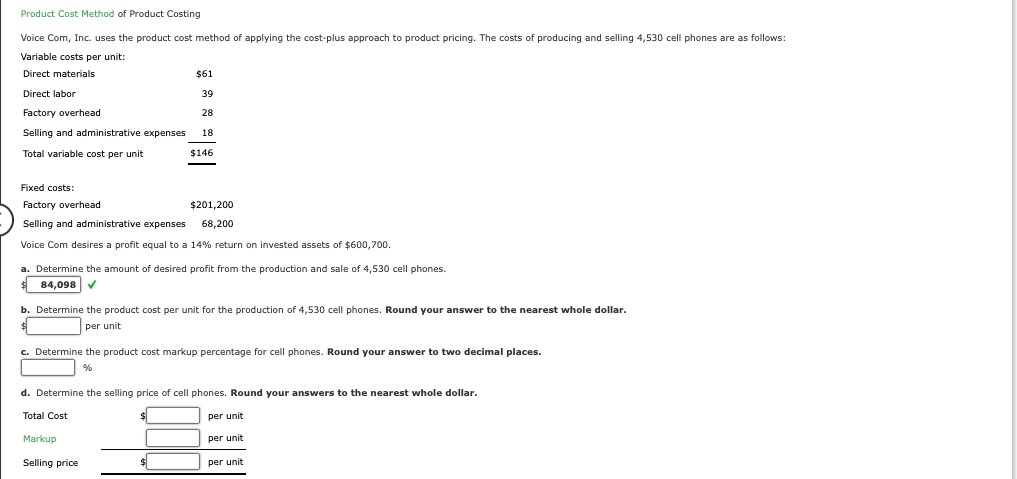

Transcribed Image Text:Product Cost Method of Product Costing

Voice Com, Inc. uses the product cost method of applying the cost-plus approach to product pricing. The costs of producing and selling 4,530 cell phones are as follows:

Variable costs per unit:

Direct materials

Direct labor

Factory overhead

Selling and administrative expenses

Total variable cost per unit

$61

39

28

18

$146

Fixed costs:

Factory overhead

$201,200

Selling and administrative expenses 68,200

Voice Com desires a profit equal to a 14% return on invested assets of $600,700.

a. Determine the amount of desired profit from the production and sale of 4,530 cell phones.

84,098

b. Determine the product cost per unit for the production of 4,530 cell phones. Round your answer to the nearest whole dollar.

per unit

c. Determine the product cost markup percentage for cell phones. Round your answer to two decimal places.

%

d. Determine the selling price of cell phones. Round your answers to the nearest whole dollar.

Total Cost

Markup

Selling price

per unit

per unit

per unit

Transcribed Image Text:Ridgeway Digital Components Company assembles circuit boards by using a manually operated machine to insert electronic components. The original cost of the machine is $52,700, the accumulated depreciation is

$21,100, its remaining useful life is 5 years, and its residual value is negligible. On October 1 of the current year, a proposal was made to replace the present manufacturing procedure with a fully automatic machine

that has a purchase price of $109,600. The automatic machine has an estimated useful life of 5 years and no significant residual value. For use in evaluating the proposal, the managerial accountant accumulated the

following annual data on present and proposed operations:

Sales

Direct materials

Direct labor

Power and maintenance

Taxes, insurance, etc.

Selling and administrative expenses

Total expenses

fan

a. Prepare a differential analysis dated October 1 to determine whether to continue with (Alternative 1) or replace (Alternative 2) the old machine. Prepare the analysis over the useful life of the new machine. If a

amount is zero, enter "0". If required, use a minus sign to indicate a loss.

Revenues:

Line Item Description

Sales (5 years)

Costs:

Differential Analysis

Continue with (Alt. 1) or Replace (Alt. 2) Old Machine

October 1

Purchase price

Direct materials (5 years)

Direct labor (5 years)

Power and maintenance (5 years)

Taxes, insurance, etc. (5 years)

Selling and admin. expenses (5 years)

Profit (loss)

Present Proposed

Operations Operations

$167,100 $167,100

$56,900 $56,900

39,500

3,700

19,500

1,300

4,400

39,500

39,500

$140,900 $120,300

-

$

Continue with Replace Old Machine Differential Effects

(Alternative 2)

Old Machine

(Alternative 2)

(Alternative 1)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- can i please get a correct answer for that questionarrow_forwardI need to know how to solve this exercise and what equation I should use Thank you!arrow_forwardMoving to another question will save this response. Question 2 A conceptual framework is like a A Moving to another question will save this responsearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education