Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

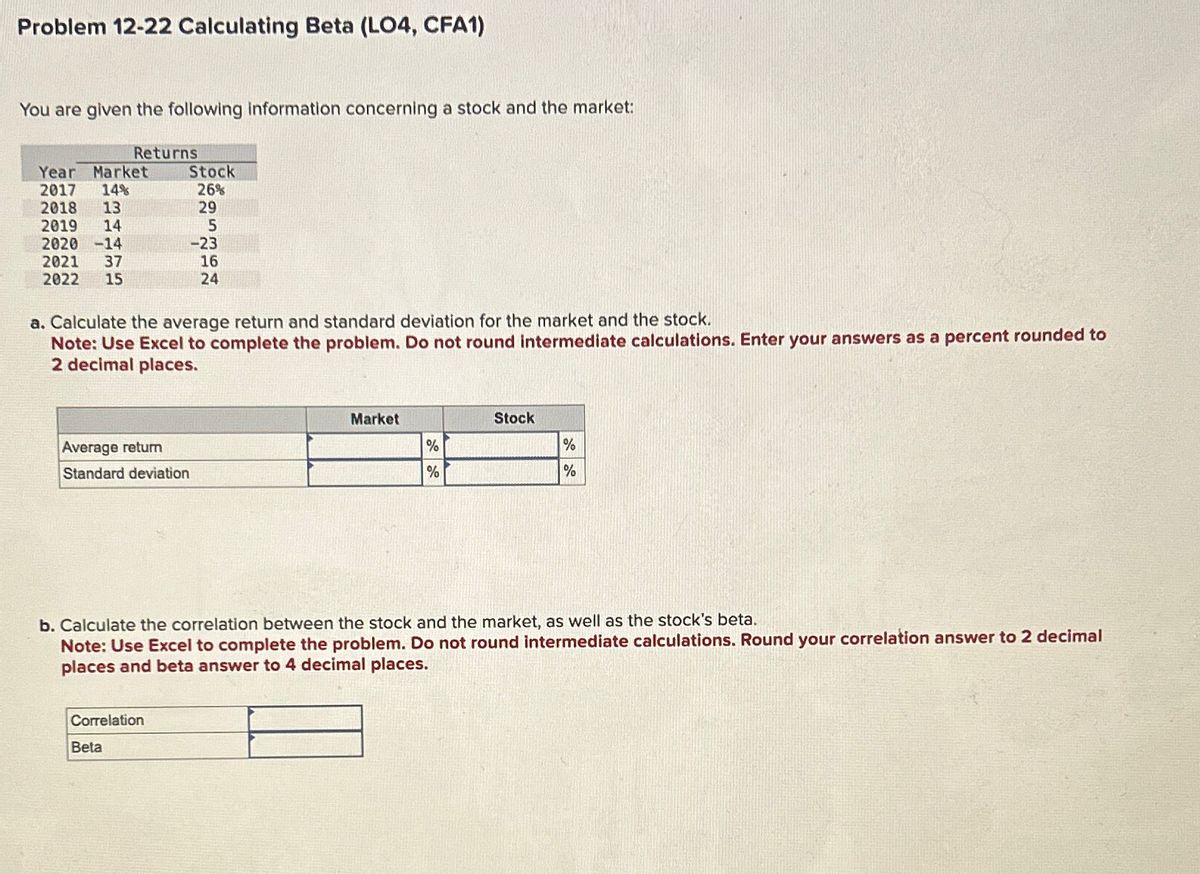

Transcribed Image Text:Problem 12-22 Calculating Beta (LO4, CFA1)

You are given the following information concerning a stock and the market:

Year Market

2017 14%

2018 13

2019 14

2020 -14

2021 37

2022 15

Returns

a. Calculate the average return and standard deviation for the market and the stock.

Note: Use Excel to complete the problem. Do not round intermediate calculations. Enter your answers as a percent rounded to

2 decimal places.

Stock

26%

29

5

-23

16

24

Average return

Standard deviation

Correlation

Beta

Market

%

%

Stock

b. Calculate the correlation between the stock and the market, as well as the stock's beta.

Note: Use Excel to complete the problem. Do not round intermediate calculations. Round your correlation answer to 2 decimal

places and beta answer to 4 decimal places.

%

%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Answer final 2arrow_forwardBholaarrow_forward3 pts Assume that you run a regression on the raw returns of the stock of Company J against the raw returns of the market and find an intercept of 1.324 percent and a beta of 1.50. If the risk-free rate is 2.64 percent, and using the concept of Jensen's Alpha, then determine by how much this stock beat the market. Answer in decimal format, to 4 decimal places. For example, if you answer is 3.33%, enter "0.0333".arrow_forward

- Consider the following information on two stocks: P(State) Stock A Stock B Boom 20% 30% 20% Normal 50% 12% -5% Slow 15% 4% 8% Recession 15% -10% 10% Calculate the covariance(A,B). (Enter percentages as decimals and round to 4 decimals)arrow_forwardReview the following market information: Current Stock Market Return 11.25% Current T-Bill Price $979.43 Historic T-Bill Average Return 2.80% Historic Stock Market Average Return 8.10% Stock Beta 1.23 What is the required return (rounded to two places)?arrow_forwardthe following information is provided for the stock market: Expected Beta Return Alphabet 12.5% 1.5 Meta 9% 1 Yahoo ? 1.35 (a) (10 points) In the context of CAPM, calculate the expected return of Yahooarrow_forward

- Historical Returns: Expected and Required Rates of Return You have observed the following returns over time: Assume that the risk-free rate is 5% and the market risk premium is 4%. a. What are the betas of Stocks X and Y? Do not round intermediate calculations. Round your answers to two decimal places. % Year 2017 2018 2019 2020 2021 % Stock X 12% 17 -13 2 22 % Stock Y 15% 7 -4 3 12 Stock X: Stock Y: b. What are the required rates of return on Stocks X and Y? Do not round intermediate calculations. Round your answers to two decimal places. Stock X: Stock Y: c. What is the required rate of return on a portfolio consisting of 80% of Stock X and 20% of Stock Y? Do not round intermediate calculations. Round your answer to two decimal places. Market 13% 12 -10 2 15arrow_forwardQ15arrow_forwardThe figure in the popup window, a. The expected return. b. The standard deviation of the return. Note: Make sure to round all intermediate calculations to at least five decimal places. Graph/chart Probability (%) 35- 30- 25- 20 15- 10- 5 9 -25% shows the one-year return distribution for RCS stock. Calculate -10% 0% Return 10% 25% - Q Q 2 Xarrow_forward

- Consider the rate of return of stocks ABC and XYZ. Year 1 2 3 4 ABC XYZ ABC 22% 9 19 1 O ABC Ⓒ XYZ ABC XYZ Required: a. Calculate the arithmetic average return on these stocks over the sample period. (Do not round Intermediate calculations. Round your answers to 2 decimal places.) XYZ 38% 11 19 -11 Arithmetic Average b. Which stock has greater dispersion around the mean return? c. Calculate the geometric average returns of each stock. (Do not round Intermediate calculations. Round your answers to 2 decimal places.) Expected rate of return 11.40 % 11.40 % Geometric Average Expected rate of return d. If you were equally likely to earn a return of 22%, 9%, 19%, 6%, or 1%, in each year (these are the five annual returns for stock ABC), what would be your expected rate of return? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) e. What if the five possible outcomes were those of stock XYZ? (Do not round Intermediate calculations. Round your answers to 2…arrow_forwardColonel Motors (C) Separated Edison (S) Expected Return 10% 8% Standard Deviation 6% 3% Please represent graphically all potential combinations of stocks C and S, if the correlation coefficient between the returns of stocks C and S is: A) 1 B) 0 C) -1 Please report these investment opportunity sets in the corresponding Excel sheets.arrow_forward4 Skipped Use the following data for Questions 3-5: Value 12500 17500 20000 Stock A B C Exp. Return 8.5% 9.2% 10.6% Beta 0.8 1.2 1.4 Question 4: What is the portfolio's Beta? ENTER YOUR ANSWER ROUNDED TO 2 DECIMAL PLACESarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education