ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

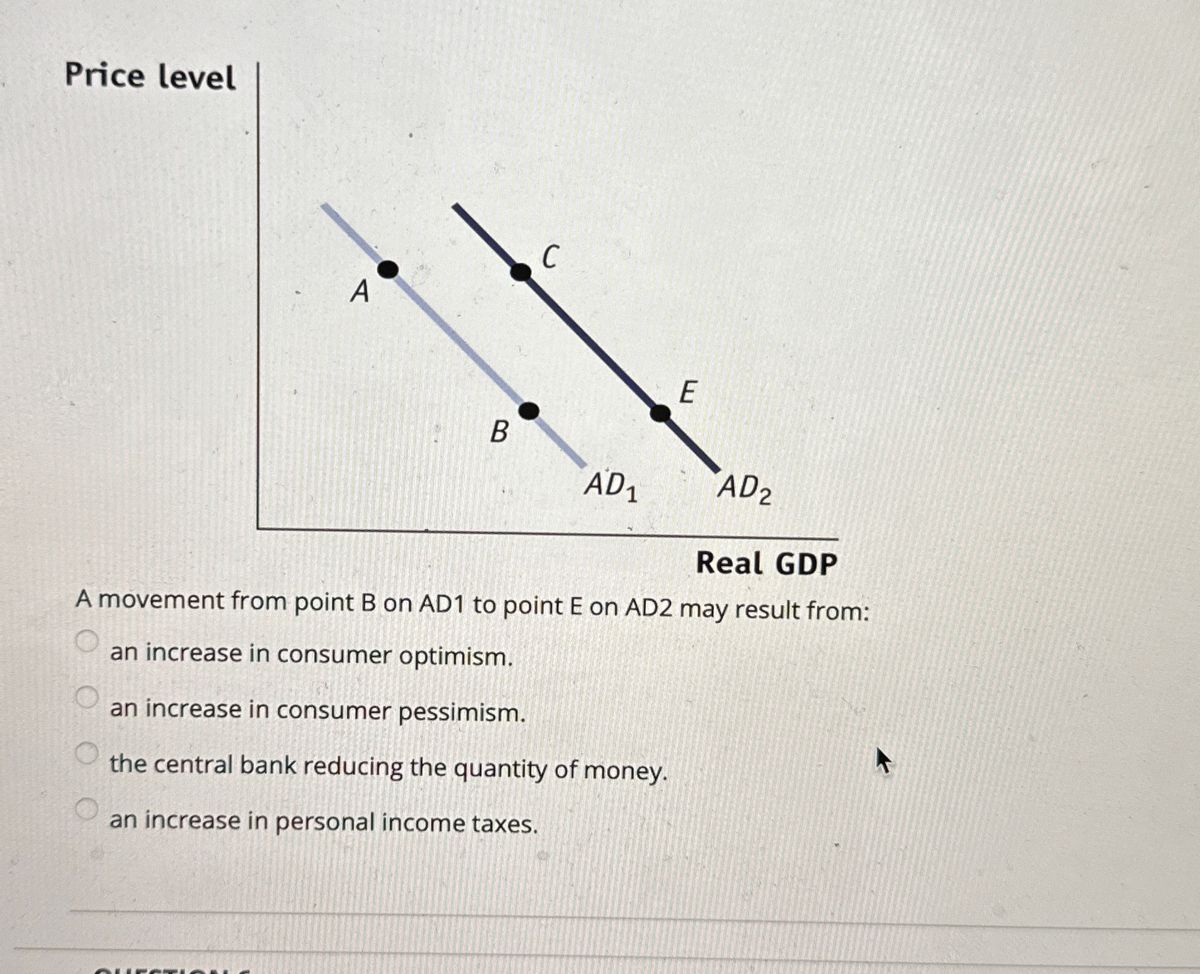

Transcribed Image Text:Price level

A

QUESTIO

B

C

AD₁

E

AD₂

Real GDP

A movement from point B on AD1 to point E on AD2 may result from:

an increase in consumer optimism.

an increase in consumer pessimism.

the central bank reducing the quantity of money.

an increase in personal income taxes.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The percentage change in the overall level of prices in an economy is called a. contraction.arrow_forwardChanges in real values can only be caused by quantity changes. Select one: True Falsearrow_forwardWhich of the following statements is false? a) Trend GDP shows what the path of potential GDP would be if it grew steadily. b) A trough occurs at the end of a period of contraction. c) Trend GDP may be below potential GDP in some quarters and above in others. d) Trend GDP may be below actual GDP in some quarters and above in others.arrow_forward

- Explain how real GDP is determined when the price level is fixed.arrow_forwardWhich of the below is one of the reasons that the Aggregate Demand curve is downward sloping? The income effect of a price change, aggregated across many markets The substitution effect of a price change, aggregated across many markets Higher inflation means nominal incomes are higher so households can afford to spend more Higher domestic price levels cause exports to fall and imports to risearrow_forwardAD AD AD, Real GDP Refer to the above diagram. An expansionary fiscal policy can best be represented by a: Multiple Choice shift in the aggregate demand curve from AD2 to AD1. shift in the aggregate demand curve from AD3 to AD2. Prex Price Levelarrow_forward

- According to Keynes’ Law... A) The total demand for products determine the level of gross domestic product and may not equal the supply capacity of the economy in the short run. B) The total demand always equals the total supply capacity in the short run. C) The total demand tends to rise above the total supply capacity in the short run which leads to recessions D) The total supply of products determines the level of gross domestic product and the level of demand in the economy in the long run.arrow_forwardWhich of the following is likely to occur if an increase in legal immigrants significantly reduces the wages of workers, ceteris paribus? A. Aggregate supply will decrease (shift left). B. Aggregate supply will increase (shift right). C. Aggregate demand will increase (shift right). D. Aggregate demand will decrease (shift left).arrow_forwardWhich of the following statement is true? A) Economic fluctuations are irregular and unpredictible B) Most macroeconomic quantities fluctuate together C) As output falls, unemployment rises D) All of the abovearrow_forward

- Price Level AD1 AD₂ AD2 Real Domestic Output, GDP Refer to the accompanying graph. What combination would most likely cause a shift from AD1 to AD2? Multiple Choice О an increase in taxes and no change in government spending О a decrease in taxes and a decrease in government spending О a decrease in taxes and an increase in government spendingarrow_forwardDeflation is particularly bad for an economy in recession for all of the following reasons EXCEPT a-with deflation people spend less expecting prices to be lower in the future b- the rising prices makes goods more expensive c- with deflation the value of assets declines while the value of loans does not - this lowers wealth and further depresses spendingarrow_forwardOther things the same, continued technological progress and continued increases in the money supply would unambiguously lead to rising prices only. rising real GDP only. rising prices and rising real GDP. neither rising prices nor rising real GDP.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education