Related questions

Concept explainers

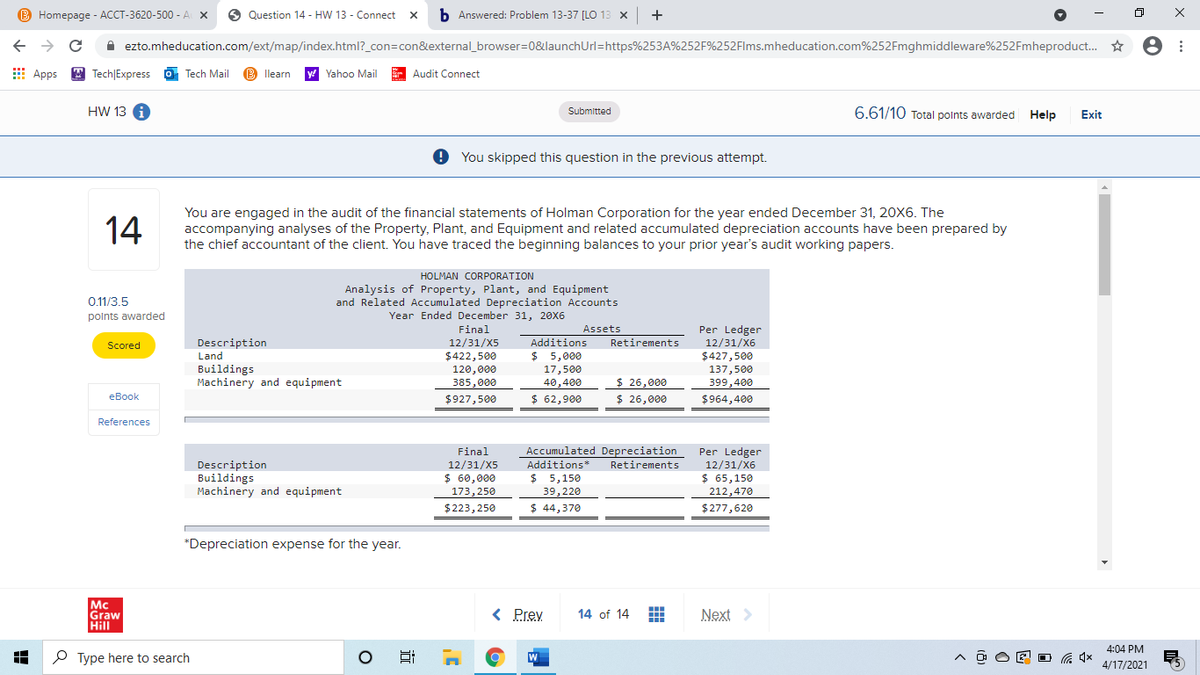

You are engaged in the audit of the financial statements of Holman Corporation for the year ended December 31, 20X6. The accompanying analyses of the Property, Plant, and Equipment and related

All plant assets are

Your audit revealed the following information:

- The company completed the construction of a wing on the plant building on June 30. The service life of the building was not extended by this addition. The lowest construction bid received was $17,500, the amount recorded in the Buildings account. Company personnel constructed the addition at a cost of $16,000 (materials, $7,500; labor, $5,500; and

overhead , $3,000). - On August 18, $5,000 was paid for paving and fencing a portion of land owned by the company and used as a parking lot for employees. The expenditure was charged to the Land account.

- The amount shown in the machinery and equipment asset retirement column represents cash received on September 5 upon disposal of a machine purchased in July 20X2 for $48,000. The chief accountant recorded depreciation expense of $3,500 on this machine in 20X6.

- Harbor City donated land and a building appraised at $100,000 and $400,000, respectively, to Holman Corporation for a plant. On September 1, the company began operating the plant. Since no costs were involved, the chief accountant made no entry for the above transaction.

Required:

Prepare the

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

- Consider the following independent situations relating to the audit of five different audit clients for year ended 30 June 20X8. Assume that all the situations are material. For each of the above cases, state the appropriate audit opinion that the auditor would require. Give reasons 1. new client has changed its valuation method of property, plant and equipment. It has adopted the Fair Value Revaluation Model to replace the Historic cost measurement method. Whilst the auditor does not object to the change in the valuation model, the new method has a material effect on the financial statements and has not been disclosed. A special meeting was held between the CFO and the Finance Team and the Lead Partner from the Audit team, but nothing was resolved 2. (ii) A new start-up company specialising in air-drone mail/package delivery has grown strongly in the past year. Over the past three years the company has made consistent losses, borrowed heavily, experienced staff turnover and dealt with…arrow_forwardDiscuss whether the changes described in each of the cases below require recognition in the CPA’s audit report as to consistency. (Assume that the amounts are material.) a. The company changed its inventory method to FIFO from weighted-average, which had been used in prior years. b. The company disposed of one of the two subsidiaries that had been included in its consolidated statements for prior years. c. The estimated remaining useful life of plant property was reduced because of obsolescence.arrow_forwardAnalyse and explain how the following situation would affect the audit report for the financial year ended on 31 December 2020. The client company, Explorer Ltd, has included $4 million mineral leases in the financial statement, which are valued by the client using fair value methodologies. However, to be able to realise the value of the mineral lease balance, additional funding is required to successfully commercialise the mineral leases. It’s uncertain that the client is able to obtain this additional funding. The auditors believe that the information is adequately disclosed by the client in the footnote of the financial report. The carrying value of the mining lease represents 6% of reported net profit for the 2020 financial year, whereas the client’s materiality is 5% of reported net profit.arrow_forward

- As the engagement partner, you have reviewed the audit working papers of Royal Height Limited. The audit team has highlighted the following matters in the working papers: Thirty percent of the companys recorded turnover (revenue) comprises of cash sales. Proper records of cash sales have not been maintained. Consequently, the audit team was unable to design audit procedures to verify the cash sales. During the current year, the company changed the method of charging depreciation on its fixed assets from the straight line to the diminishing balance method. However, all the required disclosures have been included in the notes to the financial statements. Required: Discuss the impact of each of the above matters on your audit report.arrow_forwardYou are a partner incharge of the audit for Bargin Ltd, a private company. The finishing of the audit report is pending for the income year 2018 and you have recorded some situations where possible action is required They are listed below: Bargin Ltd, carries its property, plant, and equipment accounts at current market values. Current market values exceed historical cost by a highly material amount, and the effects are pervasive throughout the financial statements. Management of Bargin Ltd, refuses to allow you to observe, or make, any counts of inventory. The recorded book value of inventory is highly material. You were unable to confirm accounts receivable with Bargin Ltd, customers. However, because of detailed sales and cash receipts records, you were able to perform reliable alternative audit procedures. One week before the end of fieldwork, you discover that the audit manager on the Bargin Ltd, engagement owns a material amount of Bargin Ltd, common stock. You relied…arrow_forwardYou a partner incharge of the audit for Bargin Ltd, a private company. The completion of the audit report is pending for the income year 2018 and you have recorded some situations where possible action is required They are listed below: Bargin Ltd, carries its property, plant, and equipment accounts at current market values. Current market values exceed historical cost by a highly material amount, and the effects are pervasive throughout the financial statements. Management of Bargin Ltd, refuses to allow you to observe, or make, any counts of inventory. The recorded book value of inventory is highly material. You were unable to confirm accounts receivable with Bargin Ltd, customers. However, because of detailed sales and cash receipts records, you were able to perform reliable alternative audit procedures. One week before the end of fieldwork, you discover that the audit manager on the Bargin Ltd, engagement owns a material amount of Bargin Ltd, common stock. You relied…arrow_forward

- please answer with reasonarrow_forwardFor the following independent situations, assume that you are the audit partner on the engagement: 1. In reviewing of subsequent events, you learned of heavy damage to the client's warehouse due to a fire occurred after year-end. The loss will partly be reimbursed by insurance. The newspaper described the event in detail. The client made adjustment to related inventories and buildings to reflect the loss. 2. All facts are the same as situation 1, but the client did not make adjustment to year end figure of inventory. 3. During the course of examination on your audit client, you suspect that a material amount of assets has been misappropriated through fraud. Management refuses to allow you to investigate further to confirm the suspicions. 4. The client's financing arrangements expired and the amount outstanding was past due. The client cannot renegotiate or obtain refinancing and is considering filing bankruptcy. Financial statements were prepared using the going concern basis and this…arrow_forwardIn reviewing of subsequent events, you learned of heavy damage to the client’s warehouse due to a fire occurred after year-end. The loss will partly be reimbursed by insurance. The newspaper described the event in detail. The client made adjustment to related inventories and buildings to reflect the loss. All facts are the same as situation 1, but the client did not make adjustment to year end figure of inventory. During the course of examination on your audit client, you suspect that a material amount of assets has been misappropriated through fraud. Management refuses to allow you to investigate further to confirm the suspicions. The client’s financing arrangements expired and the amount outstanding was past due. The client cannot renegotiate or obtain refinancing and is considering filing bankruptcy. Financial statements were prepared using the going concern basis and this fact is not disclosed. An equipment which was used by the client for more than 5 years is considered to…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education