Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

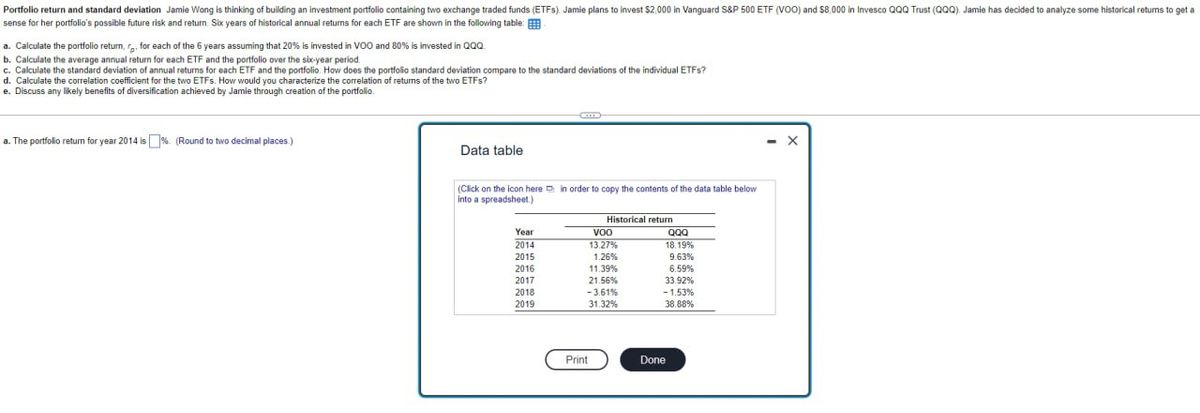

Transcribed Image Text:Portfolio return and standard deviation Jamie Wong is thinking of building an investment portfolio containing two exchange traded funds (ETFs) Jamie plans to invest $2,000 in Vanguard S&P 500 ETF (VOO) and $8,000 in Invesco QQQ Trust (QQQ). Jamie has decided to analyze some historical returns to get a

sense for her portfolio's possible future risk and return. Six years of historical annual returns for each ETF are shown in the following table:

a. Calculate the portfolio return, rp, for each of the 6 years assuming that 20% is invested in VOO and 80% is invested in QQQ

b. Calculate the average annual return for each ETF and the portfolio over the six-year period.

c. Calculate the standard deviation of annual returns for each ETF and the portfolio. How does the portfolio standard deviation compare to the standard deviations of the individual ETFs?

d. Calculate the correlation coefficient for the two ETFs. How would you characterize the correlation of returns of the two ETFs?

e. Discuss any likely benefits of diversification achieved by Jamie through creation of the portfolio.

a. The portfolio return for year 2014 is %. (Round to two decimal places.)

Data table

(Click on the icon herein order to copy the contents of the data table below

into a spreadsheet.)

Historical return

Year

2014

VOO

13.27%

QQQ

18.19%

2015

1.26%

9.63%

2016

11.39%

6.59%

2017

21.56%

33.92%

2018

-3.61%

-1.53%

2019

31.32%

38.88%

Print

Done

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Similar questions

- Manshukharrow_forwardBaghibenarrow_forwardGreta has risk aversion of A = 3 and a 1-year investment horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 9% per year, with a standard deviation of 23%. The hedge fund risk premium is estimated at 11% with a standard deviation of 38 %. The returns on both of these portfolios in any particular year are uncorrelated with its own returns in other years. They are also uncorrelated with the returns of the other portfolio in other years. The hedge fund claims the correlation coefficient between the annual return on the S&P 500 and the hedge fund return in the same year is zero, but Greta is not fully convinced by this claim. Required: a-1. Assuming the correlation between the annual returns on the two portfolios is indeed zero, what would be the optimal asset allocation? a-2. What is the expected risk premium on the portfolio? Req A1…arrow_forward

- You work as an economic analyst for an investment firm. You believe there are four possible states for the economy over the next year: Boom, Good, Poor, Bust. Your colleague Tosha has estimated the returns for three stocks based on those four scenarios. One of your clients has a portfolio that is 20.00% invested in Stock A and 30.00% invested in Stock C. The rest of your client's portfolio is invested in Stock B. Use the information below to calculate the expected return, variance, and standard deviation on your client's portfolio. 1. First fill in the missing probability and portfolio weight (cells D19 and F22). 2. Calculate the actual return for the portfolio in each state. 3. Use those portfolio returns and the probabilities to calulcate the portfolio's expected return using the SUMPRODUCT function. 4. Calculate the squared deviation from the mean for each state of the economy. 5. Use the SUMPRODUCT function to get the variance (the probability weighted average of the squared…arrow_forwardGreta has risk aversion of A = 4 and a 1-year investment horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 7% per year, with a standard deviation of 18%. The hedge fund risk premium is estimated at 12% with a standard deviation of 33%. The returns on both of these portfolios in any particular year are uncorrelated with its own returns in other years. They are also uncorrelated with the returns of the other portfolio in other years. The hedge fund claims the correlation coefficient between the annual return on the S&P 500 and the hedge fund return in the same year is zero, but Greta is not fully convinced by this claim. Required: a-1. Assuming the correlation between the annual returns on the two portfolios is indeed zero, what would be the optimal asset allocation? a-2. What is the expected risk premium on the portfolio? Complete…arrow_forwardUse the data below to answer the following question. If you have a risk-aversion factor of 2.5 and the risk-free rate is 2%, you would invest _______% of your money in the risky portfolio. Year Return 2014 -15% 2015 -5% 2016 30% 2017 -10% 2018 35%arrow_forward

- Greta has risk aversion of A = 4 and a 1-year investment horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 4-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 6% per year, with a standard deviation of 18%. The hedge fund risk premium is estimated at 10% with a standard deviation of 33%. The returns on both of these portfolios in any particular year are uncorrelated with its own returns in other years. They are also uncorrelated with the returns of the other portfolio in other years. The hedge fund claims the correlation coefficient between the annual return on the S&P 500 and the hedge fund return in the same year is zero, but Greta is not fully convinced by this claim. Compute the estimated annual risk premiums, standard deviations, and Sharpe ratios for the two portfolios. Note: Do not round your intermediate calculations. Round "Sharpe ratios" to 4 decimal places and other…arrow_forwardState the return rate (in %) for your optimal portfolio.arrow_forwardAn investment advisor has recommended a R50,000 portfolio containing assets R, J, and K; R25,000 will be invested in asset R, with an expected annual return of 12 percent; R10,000 will be invested in asset J, with an expected annual return of 18 percent; and R15,000 will be invested in asset K, with an expected annual return of 8 percent. What is the expected annual return of this portfolio? What is the correct answer? A. 12.01% B. 12.00% C. 11.98% D. 12.93%arrow_forward

- Alternative 1 2 WN 3 Investment 100% of asset F 50% of asset F and 50% of asset G 50% of asset F and 50% of asset H Year 2019 2020 2021 2022 Asset F 10% 11% 12% 13% Historical Return Asset G 11% 10% 9% 8% Asset H 8% 9% 10% 11%arrow_forwardThe following information applies to Problems 22 through 27: Greta has risk aversion of A = 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continu- ously compounded.) The S&P 500 risk premium is estimated at 5% per year, with a standard devia- tion of 20%. The hedge fund risk premium is estimated at 10% with a standard deviation of 35%. The returns on both of these portfolios in any particular year are uncorrelated with its own returns in other years. They are also uncorrelated with the returns of the other portfolio in other years. The hedge fund claims the correlation coefficient between the annual return on the S&P 500 and the hedge fund return in the same year is zero, but Greta is not fully convinced by this claim. 22. Compute the estimated annual risk premiums, standard deviations, and Sharpe ratios for the two portfolios. 23. Assuming…arrow_forwardYour client, Sandra is considering three assets: a bond mutual fund, a cryptocurrency ETF, and US Treasury bills. The annualized T-bill rate is 2%. The information below refers to the two risky assets. Expected return Standard deviation Bond mutual fund Cryptocurrency ETF 3% 10% Correlation coefficient 0 14% 20% (a) What are the proportions of each asset, in Sandra's optimal risky portfolio? (b) Suppose the return for each risky asset follows a normal distribution. What is the 1% value-at-risk for Sandra's optimal risky portfolio? Hint: P(Z<-2.326) = 0.01 where Z~N(0, 1).arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education