FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

Please provide answer as same format in question. Thanks.

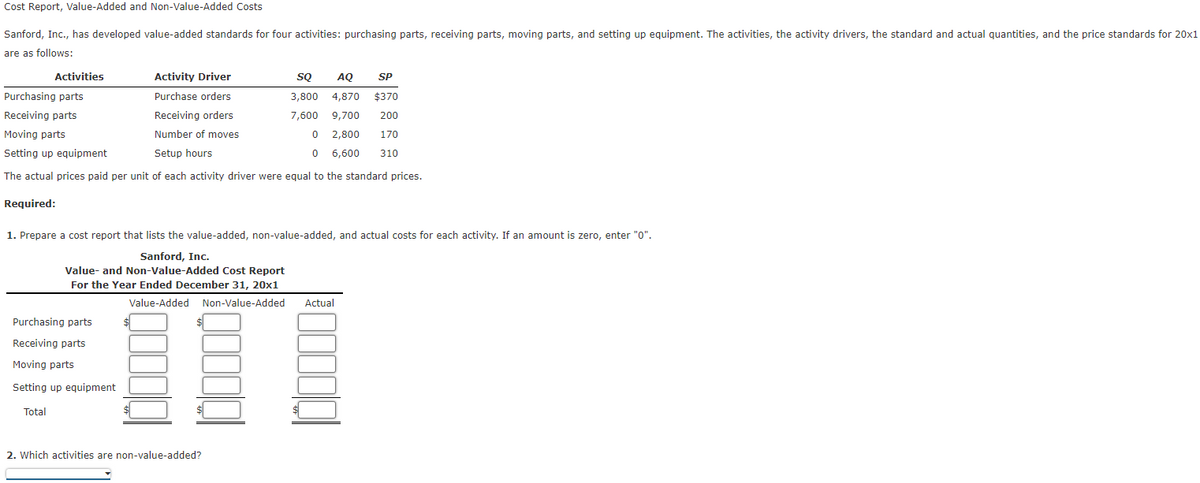

Transcribed Image Text:**Cost Report, Value-Added and Non-Value-Added Costs**

Sanford, Inc. has developed value-added standards for four activities: purchasing parts, receiving parts, moving parts, and setting up equipment. The activities, the activity drivers, the standard and actual quantities, and the price standards for 20x1 are as follows:

| **Activities** | **Activity Driver** | **SQ** | **AQ** | **SP** |

|-------------------------|---------------------|--------|--------|--------|

| Purchasing parts | Purchase orders | 3,800 | 4,870 | $370 |

| Receiving parts | Receiving orders | 7,600 | 9,700 | $200 |

| Moving parts | Number of moves | 0 | 2,800 | $170 |

| Setting up equipment | Setup hours | 0 | 6,600 | $310 |

The actual prices paid per unit of each activity driver were equal to the standard prices.

**Required:**

1. Prepare a cost report that lists the value-added, non-value-added, and actual costs for each activity. If an amount is zero, enter "0".

**Sanford, Inc.**

**Value- and Non-Value-Added Cost Report**

**For the Year Ended December 31, 20x1**

| **Activities** | **Value-Added** | **Non-Value-Added** | **Actual** |

|-------------------------|-----------------|---------------------|------------|

| Purchasing parts | | | |

| Receiving parts | | | |

| Moving parts | | | |

| Setting up equipment | | | |

| **Total** | | | |

2. Which activities are non-value-added?

**Explanation:**

- **Graphs/Diagrams**: The table in the image represents various activities related to inventory and setup processes at Sanford, Inc. It details the standard quantity (SQ), actual quantity (AQ), and standard price (SP) for each activity. The cost report form is meant to assess which activities add value or incur unnecessary costs (non-value-added).

- **Activities and Drivers**: Four key activities are analyzed here:

- **Purchasing parts** requires purchase orders.

- **Receiving parts** involves handling

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education