FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

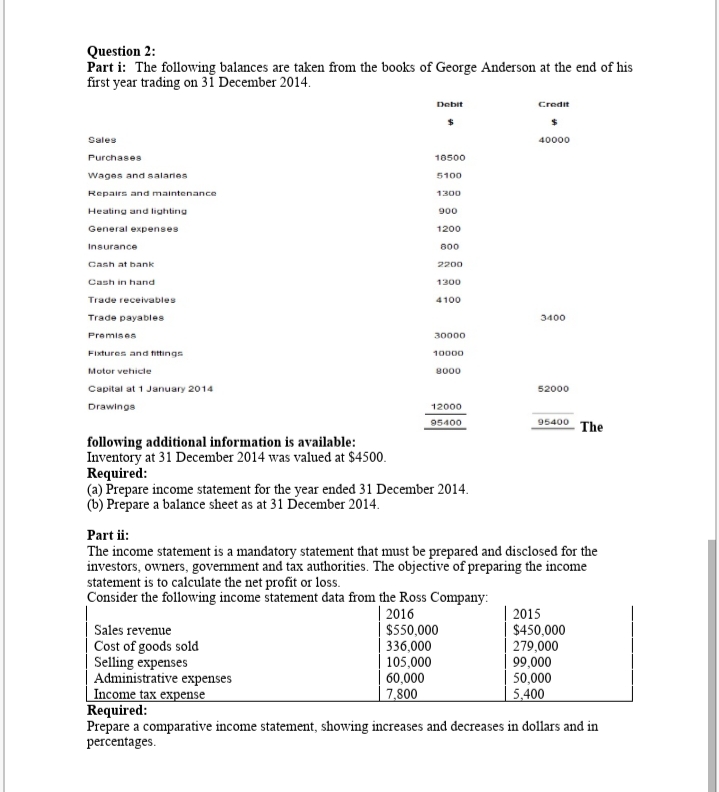

Transcribed Image Text:Question 2:

Part i: The following balances are taken from the books of George Anderson at the end of his

first year trading on 31 December 2014.

Debit

Credit

%24

Sales

40000

Purchases

18500

Wages and salaries

5100

Repairs and maintenance

1300

Heating and lighting

900

General expenses

1200

Insurance

800

Cash at bank

2200

Cash in hand

1300

Trade receivables

4100

Trade payables

3400

Premises

30000

Fixtures and fttings

10000

Motor vehicle

8000

Capital at 1 January 2014

52000

Drawings

12000

95400

95400 The

following additional information is available:

Inventory at 31 December 2014 was valued at $4500.

Required:

(a) Prepare income statement for the year ended 31 December 2014.

(b) Prepare a balance sheet as at 31 December 2014.

Part ii:

The income statement is a mandatory statement that must be prepared and disclosed for the

investors, owners, government and tax authorities. The objective of preparing the income

statement is to calculate the net profit or loss.

Consider the following income statement data from the Ross Company:

| 2016

| $550,000

336,000

105,000

60,000

2015

$450,000

279,000

99,000

50,000

5,400

Sales revenue

Cost of goods sold

Selling expenses

Administrative expenses

Income tax expense

Required:

Prepare a comparative income statement, showing increases and decreases in dollars and in

percentages.

7,800

Transcribed Image Text:Part iii:

Walter incorporation had the following transactions during the month of March 2018. Prepare an

income statement based on this information being careful to include only those items that should

appear in that financial statement.

1. Cash received from bank loans was $10,000

2. Revenues earned and received in cash were $8,500

3. The owner waters withdrew $4,000 in cash

4. The expenses incurred and paid were$ 5,000.

Part iv:

An inexperienced accountant for Fowler Company prepared the following income statement for

the month of august 2018

FOWLER COMPANY

Income Statement

For the Year Ended December 31, 2018

Revenues

Services provided to customers

investment by Q Fowler owner

$ 10,000.00

$ 5,000.00

loan from bank

1,400.00

Total Revenues:

$ 16,400.00

Expenses

payment to long term creditors

expenses required to provide services to customer

purchase of land

Total Expenses:

8000

7500

16000

Net Loss

31,500.00

$(15,100.00)

Required:

Prepare a revise income statement in accordance with generally accepted accounting principles.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 7 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- At the beginning of Year 3 Omega Company had a $75,000 balance in its accounts receivable account and a $10,400 balance in allowance for doubtful accounts. During Year 3 Omega experienced the following events. (1) Earned $256,000 of revenue on account. (2) Collected $248,000 cash from accounts receivable. (3) Wrote off $8,500 of accounts receivable as uncollectible. Omega estimates uncollectible accounts to be 4% of receivables. The December 31, Year 3 ending balance in the allowance for doubtful accounts account (balance after expense recognition) is: Multiple Choice $2,980. $8,500. $2,660. $3,300.arrow_forwardb) Sofea Enterprise runs a retail business. All cash and cheque receipt and payment are recorded in the Cash Book. The following transactions occurred during the month of September 2021 and are yet to be recorded in the Cash Book: The debit balance in the Cash and Bank accounts are $2,000 and $17,000 respectively. 3/9 Transfer cash $1,000 into the bank account. 4/9 Purchased goods worth $3,600 by cheque. 5/9 Paid Jamilah & Co. $5,000 by cheque for purchase of goods. 6/9 The owner took $500 cash for his own use. 8/9 Paid the shop rental $3,000 by cheque. 10/9 Received a cheque from Ms. Angie amounting to $3,600 after deducting cash discount $400. 15/9 Cash sales of $3,200. 18/9 Issued $2,850 cheque to Seri Enterprise after deducting cash discount of 5%. 20/9 Received $5,000 cheque from Faiz Enterprise. 23/9 Cash sales banked the same day, $2,600. 28/9 Paid wages to shop assistant by cheque, $1,200. REQUIRED: Prepare a Three-column Cash Book, balancing it at 30 September 2021. Bring down…arrow_forwardPart 1 Prepare journal entries to the following. (Do not round intermediate calculations. Round the final answers to the nearest whole dollar.) a. Issuance of the bonds on June 1, 2023 b. Payment of interest on December 1, 2023 c. Adjusting entry to accrue bond interest and discount amortization on January 31, 2024 d. Payment of interest on June 1, 2024 Assume JetCom Inventors Inc. has a January 31 year-end. View transaction list Journal entry worksheet 1 2 3 4 Record issued bond at discount. Note: Enter debits before credits. Date June 01, 2023 General Journal Debit Credit >arrow_forward

- On December 31, 2018, Lance Company prepared an income statement and balance sheet. Total: Revenues, Expenses, Net Income, Assets, Liabilities, and Stockholders' Equity had the following balances, respectively: Net Revenues Expenses Total Assets $40,000 $100,000 $30,000 Total Liabilities Stockholders' Equity $70,000 Income 120,000 80,000 During audit, the auditor detected that the following transaction was not recorded: Sold $30,000 merchandise in cash. Sales taxes was 6% which was not included in the price. Merchandise sold had cost company 18,000 to purchase. What would be the total amount of Revenues, Expenses, Net Income, Assets, Liabilities, and Stockholders' Equity, after recording the above transaction. Net Revenues Experkses Income Total Assets Total Liabilities Stockholders' Equity Balance: Before 120,000 80,000 $40,000 $100,000 $30,000 $70,000 trans. After transarrow_forward"Marquis Smith started IT Consulting Services Incorporated on January 1, Year 1. The company experienced the following events during its first year of operation 1 On June 1 Year 1, the company borrowed $21.600 cash from the bank. The note had a one-year term and 6% annual interest rate 2. On December 31. Year 1, the company adjusted the accounting records to recognize accrued interest expense on the bank note Required: Use a horizontal financial statements model to show how each event affects the balance sheet, income statement, and statement of cash flows More specifically, record the amounts of the events into the model. Also, in the Statement of Cash Flows column, classify the cash flows as operating activities (OA), investing activities (IA), or financing activities (FA) Note: Enter any decreases to account balances and cash outflows with a minus sign. Leave cells blank if no input is needed. Event Number Assets Cash 21 600 2 Total CNet change in cash 01 21.600 Notes Payable 21,600…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education