FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

(a)Prepare the bank reconciliation statement for the month of December 2021.

(b)Prepare the necessary adjusting journal entries to update the accounting record.

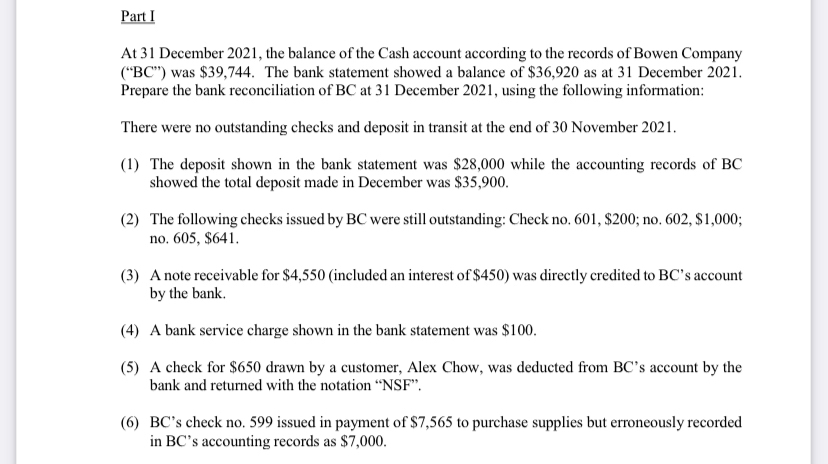

Transcribed Image Text:Part I

At 31 December 2021, the balance of the Cash account according to the records of Bowen Company

("BC") was $39,744. The bank statement showed a balance of $36,920 as at 31 December 2021.

Prepare the bank reconciliation of BC at 31 December 2021, using the following information:

There were no outstanding checks and deposit in transit at the end of 30 November 2021.

(1) The deposit shown in the bank statement was $28,000 while the accounting records of BC

showed the total deposit made in December was $35,900.

(2) The following checks issued by BC were still outstanding: Check no. 601, $200; no. 602, $1,000;

no. 605, $641.

(3) A note receivable for $4,550 (included an interest of $450) was directly credited to BC's account

by the bank.

(4) A bank service charge shown in the bank statement was $100.

(5) A check for $650 drawn by a customer, Alex Chow, was deducted from BC's account by the

bank and returned with the notation "NSF".

(6) BC's check no. 599 issued in payment of $7,565 to purchase supplies but erroneously recorded

in BC's accounting records as $7,000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The accountant of Universe Manufacturing collected the following information: The balance as per bank statement is $2,560.32 on 30 June 2020. On this date, the balance of the company’s book is $3,730.32. In addition, the accountant found the following items: a) Deposits in transit $1,460 b) Outstanding checks: $730 c) Bank statement shows a bank collection from bill receivables $1,000 d) Bank statement shows Interest received of $150 e) Bank service charge in the bank statement is $340 Required: prepare bank reconciliation statement at 30 June 2020.arrow_forwardPrepare any journal entries that should be made as a result of the bank reconciliation.arrow_forwardcomplete and correct help will be appreciate answer in text show computation for numbers with explanationarrow_forward

- Western Flyers received its bank statement for the month of July 2019 with an ending balance of $11,065.00 whereas the cash book balance for Western Flyers is $12875. Western Flyers determined that check #598 for $125.00 and check #601 for $375.00 were both outstanding. Also, a $7,500.00 deposit for July 30th was in transit as of the end of the month. Big Bucks Bank also collected an amount of $5,300 from a client of Western Flyer as payment of a note ($5,000) and interest ($300) earned on a note. Big Bucks Bank charged Flyers a $15.00 fee for the collection service and $20 for issuance of 10 check books. 5. A check for $75.00 from Colin Abraham, a client, was returned with the bank statement marked “NSF”.arrow_forwardA written order for a bank or other financialinstitution to pay a stated dollar amountto a specified business or person is called aa. check.b. deposit slip.c. notes receivable.d. receipt.e. debit memorandumarrow_forwardCoasters Co. issued a note receivable to a customer. The customer made payment directly to the Coaster’s bank. The payment appeared on the month-end bank statement. How would this payment be adjusted in the bank reconciliation? Add to company records (book side) Subtract from company records (book side) Subtract from bank statement (bank side) Add to bank statement (bank side)arrow_forward

- Please prepare the bank reconciliation statement on 31 May 2021 in your activity book from information . Please do it in the attached format. All information needed has been attachedarrow_forwardThe following information is available for the FRAN Company for the month of December 2019 1. On December 31, 2019 the balance in the company's Cash account has a balance of $ 15,862 . 2. The company's bank statement shows a balance December 31, 2019 of $ 19,454 . 3. Outstanding checks at December 31, 2019 total $ 2,967 . 4. A deposit placed in the bank's night depository on December 31, 2019 totaling $ 1,351 did not appear on the bank statement. 5. Included with the bank statement was a debit memorandum in the amount of $ 26 for bank service charges. It has not been recorded on the company's books. 6. Included with the bank statement was a credit memorandum for collection of a notes receivable for $ 1,243 . It has not been recorded on the company’s books. 7. A cash sales on December 15, 2019 that totaled $ 916 was incorrectly journaled and posted as $ 961 . 8. A cash sales on December 27, 2019 that totaled $ 461 was incorrectly journaled and posted as $ 416 . 9. Check #145 was written…arrow_forwardCan you please show your work on how you came up with the balance per bank and the balance per book on the reconciliation statement? Branson Co. received its bank statement for the month ending May 31, 2019, and reconciled the statement balance to the May 31, 2019, balance in the Cash account. The reconciled balance was determined to be $36,400. The reconciliation recognized the following items: A deposit made on May 31 for $22,700 was included in the Cash account balance but not in the bank statement balance. Checks issued but not returned with the bank statement were No. 673 for $4,550 and No. 687 for $9,700. Bank service charges shown as a deduction on the bank statement were $110. Interest credited to Branson Co.'s account but not recorded on the company's books amounted to $88. Returned with the bank statement was a "debit memo" stating that a customer's check for $3,240 that had been deposited on May 23 had been returned because the customer's account was overdrawn. During a…arrow_forward

- The following data represents information necessary to assist in preparing the July 31, 2019 bank reconciliation for Domore Company. On July 31, the bank balance was $5,353. The bank statement indicated a deduction of $20 for all bank service charges. A customer deposited $1,210 directly into the bank account to settle an outstanding accounts receivable bill. Cheque #566 for $800 and cheque #573 for $560 have been recorded in the company ledger but did not appear on the bank statement. A customer paid an amount of $4,570 to Domore Company on July 31 but the deposit did not appear on the bank statement. The accounting clerk made an error and recorded a $150 cheque as $1,500. The cheque was written to pay an outstanding accounts payable account. Cheque #8603 for $170 was deducted from Domore Company's account by the bank. This cheque was not written by Domore Company and needs to be reversed by the bank. The bank included an NSF cheque in the amount of $490 relating to a…arrow_forwardWinson Company reported the following information related to its 31 August 2019 bank statement: i) The bank statement's balance is $3267. ii) The cash account balance is $3193. iii) The outstanding checks total $612. iv) The deposits in transit amount to $1415. v)The bank service charge is $27. vi) Winson's accountant issued a check for $153 (inpayment on an account payable) that was erroneously recorded in the ledger as $135. vii)Bank debit memorandum for$138 NSF (not sufficient funds)check from one of its customers. viii) The bank collected an account receivable in the amount of $1060 on. behalf if Winson Company. Required; Prepare Winson Company's bank reconciliation on 31 August 2019.arrow_forwardMatch each description to the appropriate term. Clear All Measures how frequently during the year accounts Net realizable value receivable are being turned into cash Amounts owed by customers Receivables documented by a formal written instrument of credit All money claims against Notes receivable other entities The difference between Accounts receivable accounts receivable and turnover allowance for doubtful accountsarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education