ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

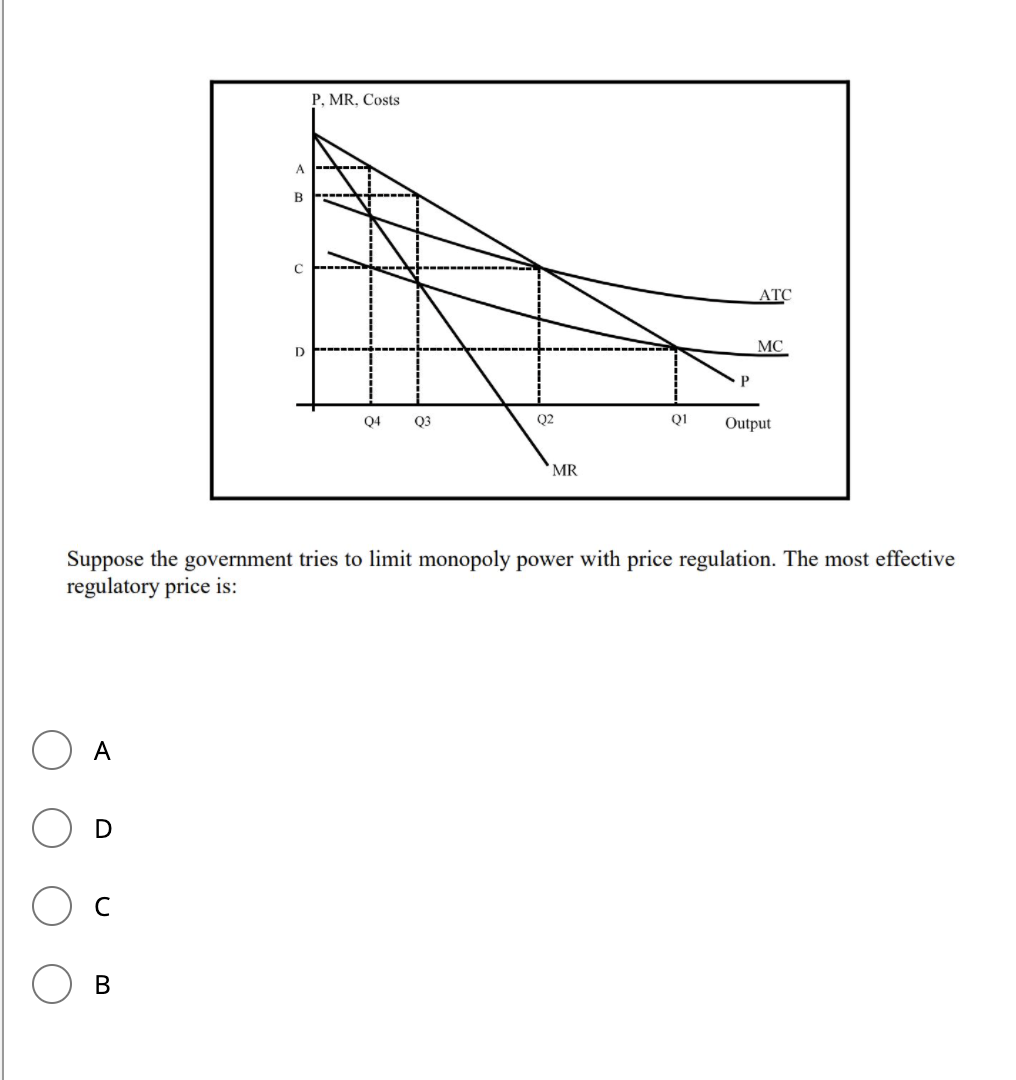

Transcribed Image Text:P, MR, Costs

A

B

ATC

MC

Q4

Q3

Q2

QI

Output

MR

Suppose the government tries to limit monopoly power with price regulation. The most effective

regulatory price is:

A

D

В

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- ASAP Suppose the market for kiwis has a demand curve of the form: Qd = 200-2Pd And that the costs of the monopoly producer of kiwis are determined by Total Cost (Q) = Variable Cost (Q) + Fixed Cost. C (Q) = Q² + 100. That is, its marginal cost will be: MgC (Qs) = 2Qs = Ps A. If the Government regulates this monopoly so that it does not generate welfare losses, how much should the maximum price to impose be? B. If the Government decides to grant a subsidy to reach the amount of the social optimum, would it stop having a loss of welfare? C. Bonus How much the subsidy should be for each unit so that the amount is reached in the social optimum.arrow_forward20. A natural monopoly occurs when one firm can supply the entire market more cheaply than can a number of firms. b. results from decreasing returns to scale. o. is a monopoly in the production of raw materials. d. is one result of a patent. a. 100G Oarrow_forwardDon't use chatgpt otherwise we will give dounvotearrow_forward

- A monopoly can sell 20 units of output for $18 per unit. Alternatively it can sell 21 units of output for $16 per unit. The marginal revenue of the 21st unit of output is...arrow_forward3. Assume inverse demand function for game console in an imaginary country is P=1200-4Q and the total cost function is TC=400+4Q². Government put $120 of specific tax on production. a. If the market is competitive what is the incidence of tax on consumer? b. If the market is monopolist what is the incidence of tax on consumer?arrow_forwardAssume inverse demand function for game console in an imaginary country is P=1200-4Q and the total cost function is TC=400+4Q². Government put $120 of specific tax on production. a. If the market is competitive what is the incidence of tax on consumer? b. If the market is monopolist what is the incidence of tax on consumer?arrow_forward

- a d MC = ATC MR D h Quantity (units) Refer to the figure above. Using the labels provided in the graph, identify the area of deadweight loss that would exist if this were a monopoly market. def acf bcde efgh abd $/unitarrow_forwardWhile firms in perfect competition maximize profit by producing at a quantity where the marginal cost of producing another unit of a good is equal the the marginal revenue from producing another unit, monopoly firms will maximize profit by producing at a quantity where marginal cost of producing another unit is equal to the marginal revenue (the same as perfect competition) the marginal profit the average total cost O the price of the good 10:04 P Bi 63°F Cloudy 5/20/202 e here to search Oarrow_forwardWhen will a monopoly be economically efficient? a if it produces where the marginal cost equals the average cost b if it produces where the marginal cost is greater than the average cost c if it produces where the marginal cost is less than the average cost d if it produces where the marginal cost equals the pricearrow_forward

- You are an analyst for De Boers, the monopoly producer of diamonds. You are given the following market information: P = -4QD + 76 P = 8Qs + 10 TC = 40 + 15Q? MC = 30Qarrow_forwardIf a monopoly car[ sell 120 units of output for $11 each or 110 units of output for $12 each, we can safely conclude that for this monopoly, the profit-maximizing level of output is: a. greater than 120 units. b. less than 120 units. c. less than 110 units.. d. greater than 110 units.arrow_forwardPM P Monopoly O A. Green O B. Yellow O C. Pink O D. Blue QM MC MR ATC D Which region represents deadweight loss?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education