FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

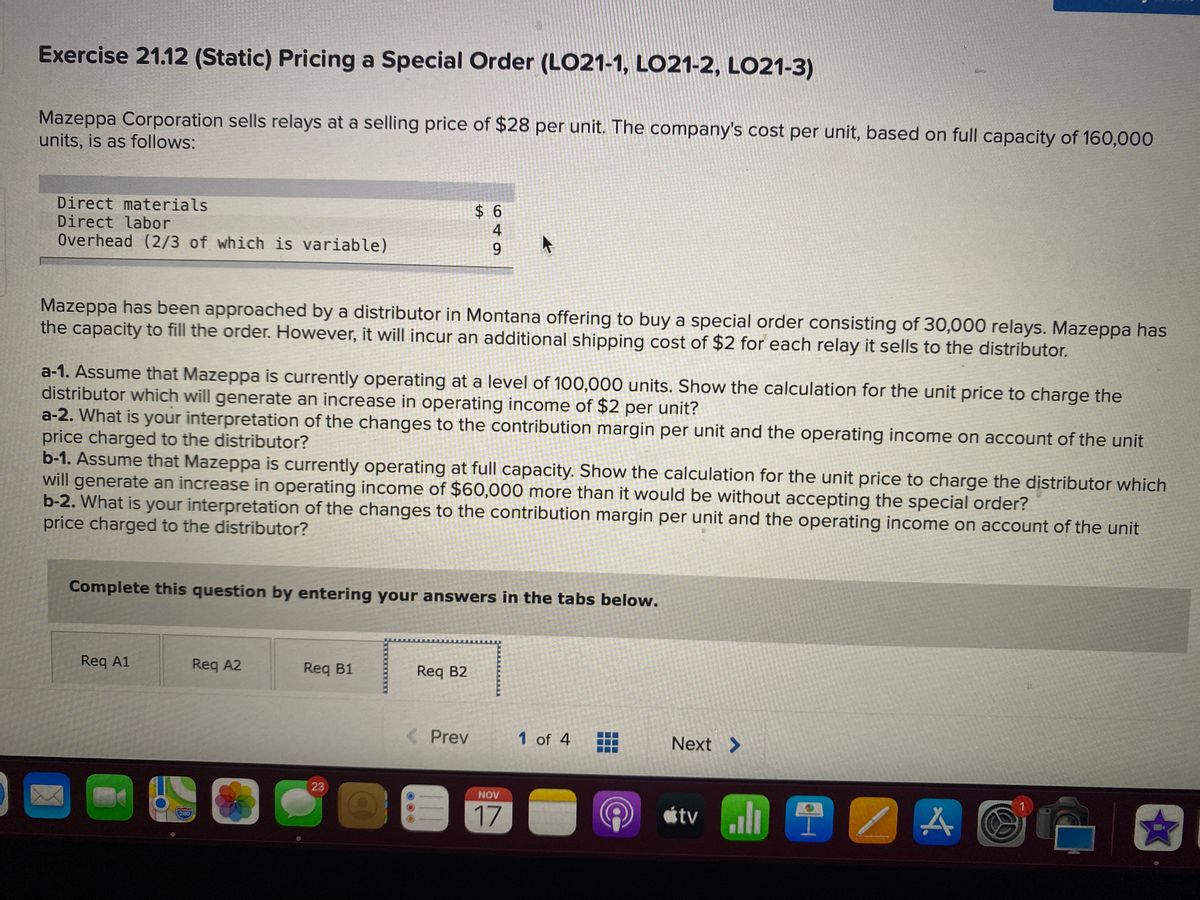

Transcribed Image Text:Exercise 21.12 (Static) Pricing a Special Order (LO21-1, LO21-2, LO21-3)

Mazeppa Corporation sells relays at a selling price of $28 per unit. The company's cost per unit, based on full capacity of 160,000

units, is as follows:

Direct materials

Direct labor

Overhead (2/3 of which is variable)

Mazeppa has been approached by a distributor in Montana offering to buy a special order consisting of 30,000 relays. Mazeppa has

the capacity to fill the order. However, it will incur an additional shipping cost of $2 for each relay it sells to the distributor.

a-1. Assume that Mazeppa is currently operating at a level of 100,000 units. Show the calculation for the unit price to charge the

distributor which will generate an increase in operating income of $2 per unit?

a-2. What is your interpretation of the changes to the contribution margin per unit and the operating income on account of the unit

price charged to the distributor?

b-1. Assume that Mazeppa is currently operating at full capacity. Show the calculation for the unit price to charge the distributor which

will generate an increase in operating income of $60,000 more than it would be without accepting the special order?

b-2. What is your interpretation of the changes to the contribution margin per unit and the operating income on account of the unit

price charged to the distributor?

Complete this question by entering your answers in the tabs below.

Req A1

Req A2

Reg B1

Req B2

Prev

1 of 4

Next >

23

NOV

al T2 A

17

tv

280

649

%24

![bričé chárged to the distributor?

Complete this question by entering your answers in the tabs below.

Req A1

Req A2

Req B1

Req B2

What is your interpretation of the changes to the contribution nargin per unit and the operating income on account of the unit price charged to

the distributor? (Do not round intermediate calculations.)

In order for the company to increase its operating income $60,000 above what it would be without the order,

the contribution margin per unit included with the special order must be $2 per unit more ($2 × 30,000 units =

$60,000) than the normal contribution margin. The normal contribution margin is the sales price, $28, less

all variable costs [

+ (2/3 x

], or $12. Thus, the selling price of the

special order must cover the additional shipping costs, and still result in a contribution margin of

normal + $2 additional requirement). Therefore, a selling price of

is required.

< Req B1

Req B2>

Prev

1 of 4

Next >

23

國 2囚

NOV

17

étv

280

MacBook Air](https://content.bartleby.com/qna-images/question/bed57b3f-4985-4c44-a1d3-1432756d6b0e/8329eb68-ab40-4af0-8f28-b204e7c910fd/9p07d_processed.jpeg)

Transcribed Image Text:bričé chárged to the distributor?

Complete this question by entering your answers in the tabs below.

Req A1

Req A2

Req B1

Req B2

What is your interpretation of the changes to the contribution nargin per unit and the operating income on account of the unit price charged to

the distributor? (Do not round intermediate calculations.)

In order for the company to increase its operating income $60,000 above what it would be without the order,

the contribution margin per unit included with the special order must be $2 per unit more ($2 × 30,000 units =

$60,000) than the normal contribution margin. The normal contribution margin is the sales price, $28, less

all variable costs [

+ (2/3 x

], or $12. Thus, the selling price of the

special order must cover the additional shipping costs, and still result in a contribution margin of

normal + $2 additional requirement). Therefore, a selling price of

is required.

< Req B1

Req B2>

Prev

1 of 4

Next >

23

國 2囚

NOV

17

étv

280

MacBook Air

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education