ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

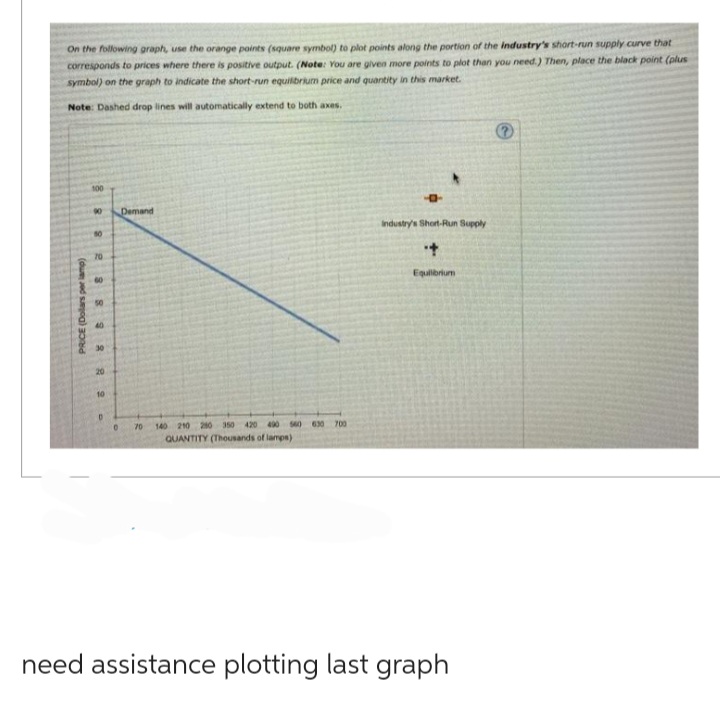

Transcribed Image Text:On the following graph, use the orange points (square symbol) to plot points along the portion of the industry's short-run supply curve that

corresponds to prices where there is positive output. (Note: You are given more points to plot than you need.) Then, place the black point (plus

symbol) on the graph to indicate the short-run equilibrium price and quantity in this market.

Note: Dashed drop lines will automatically extend to both axes.

8 8 8 8 8

100

PRICE (Dollars per lamp)

8 8 8

50

30

20

10

D

0

Demand

70 140 210 280 350 420 490 560

QUANTITY (Thousands of lamps)

630 700

P

industry's Short-Run Supply

+

Equilibrium

need assistance plotting last graph

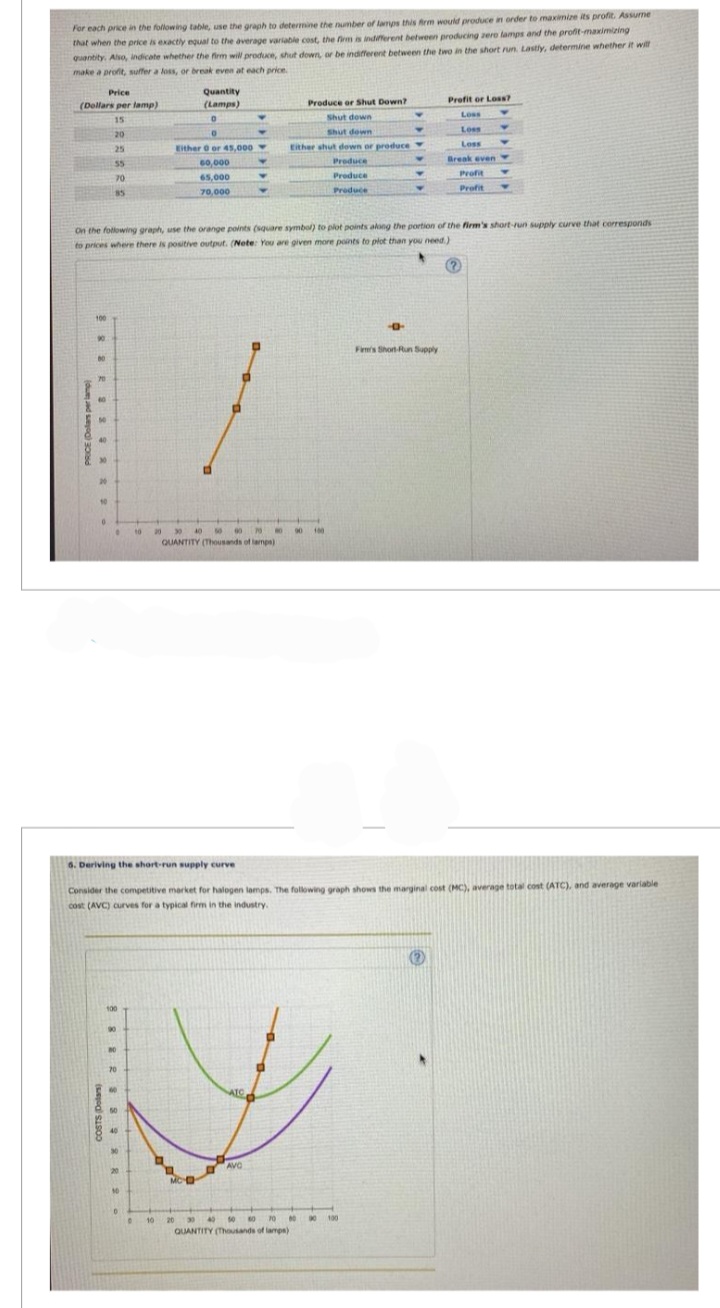

Transcribed Image Text:For each price in the following table, use the graph to determine the number of lamps this firm would produce in order to maximize its profit. Assume

that when the price is exactly equal to the average variable cost, the firm is indifferent between producing zero lamps and the profit-maximizing

quantity. Also, indicate whether the firm will produce, shut down, or be indifferent between the two in the short run. Lastly, determine whether it will

make a profit, suffer a loss, or break even at each price.

Price

(Dollars per lamp)

15

20

PRICE (Dollars per lamp

80

RS232

70

26

25

55

70

85

10

588 288 8

COSTS (Dolars)

20

On the following graph, use the orange points (square symbol) to plot points along the portion of the firm's short-run supply curve that corresponds

to prices where there is positive output. (Note: You are given more points to plot than you need.)

(?

10

0

10

D

Quantity

(Lamps)

0

0

Either 0 or 45,000

10

60,000

65,000

70,000

MC-D

20

D

20 30 40 50 60 75 NO

QUANTITY (Thousands of lamps)

Y

D

Y

6. Deriving the short-run supply curve

Consider the competitive market for halogen lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable

cost (AVC) curves for a typical firm in the industry.

ATC

♥

AVC

Produce or Shut Down?

Shut down

Shut down

Either shut down or produce

Produce

Produce

Produce

90 100

Y

50 60

70

00

30 40

QUANTITY (Thousands of lamps)

Y

00100

Profit or Loss?

Loss

Loss

Loss

--0-

Firm's Short-Run Supply

Y

Break even Y

Profit

Profit

Y

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Homework (Ch 09) 1. The supply curve in the very short run The following graph shows the annual demand for tortilla chip consumption, which is initially in long-run equilibrium at point D. Suppose that tortilla chips are sold in a perfectly competitive market, and tastes shift away from tortilla chips so that demand shifts leftward from D₁ to D₂. Use the purple line (diamond symbol) to illustrate the supply curve in the very short run. Make sure the line passes through two of the starred points on the graph. PRICE (Dollars per bag) 10 9 0 1 2 C D A B D₂ 3 4 5 6 7 8 QUANTITY (Millions of bags per year) 9 D. 10 Short-Run Supply Curve ?arrow_forwardPlease correct answer and don't use hend raitingarrow_forwardExplain how the following events may affect the profit rate for a U.S. firm and industry (be sure to define your measure(s) of the profit rate) :Consider both the immediate impact and the possible long run implications: (1) across firms within an industry; (2) across industries and (3) across nations please long and mindful answers that covers all three categories. j) Removal of all subsidies to the U.S. agriculture sector k) Reduction in the federal tax rate on profit incomearrow_forward

- Assume that the cost data in the following table are for a purely competitive producer: Average Average Average Total Variable Marginal Cost Total Fixed Product Cost Cost Cost 1 $60.00 $45.00 $105.00 $ 45.00 30.00 42.50 72.50 40.00 3 20.00 40.00 60.00 35.00 4 15.00 37.50 52.50 30.00 12.00 37.00 49.00 35.00 6. 10.00 37.50 47.50 40.00 7 8.57 38.57 47.14 45.00 7.50 40.63 48.13 55.00 9. 6.67 43.33 50.00 65.00 10 6.00 46.50 52.50 75.00 Instructions: If you are entering any negative numbers be sure to include a negative sign (-) in front of those numbers. Select "Not applicable" and enter a value of "0" for output if the firm does not produce. a. At a product price of $57.00 (i) Will this firm produce in the short run? (Click to select) V (ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output? |(Click to select V output = units per firm (iii) What economic profit or loss will the firm realize per unit of output? |(Click to select v per unit = $ b.…arrow_forwardQ27arrow_forwardThe following graph shows the market for annual tortilla chip consumption, which is initially in long-run equilibrium at point D. After the change in tastes and the rightward shift in demand, the market moves to point in the short run and then to point in the long run. On the following graph, use the purple line (diamond symbol) to plot the long-run market supply curve for tortilla chips, making sure that it goes through two of the points A, B, C, or D. PRICE (Dollars per bag 10 9 8 2 1 D 0 1 True B D₁ O False 23 C S 10²4 NO 2 3 4 5 7 8 QUANTITY (Milions of bags per year) According to the graph, the tortilla chip market is an example of 10 Long-Run Supply True or False: The average cost at the cost-minimizing level of output is lower for the new marginal firm than it was for the marginal firm before the change in demand. industry.arrow_forward

- Illustrate to the right, a graph showing a company being profitable in a competitive market in the Long Run selling its product at Market Price (MP*) based on its Average Variable Cost (AVC) and Average Total Cost (ATC) and Marginal Cost (MC). Identify each key point on the graph. Observe the Short - Run Loss information illustrated in the graph to the right. With respect to Price (P*"), Average Variable Cost (AVC), Average Total Cost (ATC), Marginal Revenue (MR), and Marginal Cost (MC), what assumption would you make if the firm was selling its product at P What would happen if this were to continue in the long run? Is there a Shut Down point? ** ? Notice that MR = Parrow_forwardThis problem continues from the previous one. On the graph the supply in the Rest of the World has shifted from Sstart to S2 and the market in the Rest of the World has moved to a new short run equilibrium at B. The price of Good A is P1 in the U.S. and P2 in the Rest of the World. Which answer choices are correct from the image bellow?arrow_forwardConsider the perfectly competitive spice market. At the equilibrium price, the elasticity of market supply is 2.65 and the elasticity of demand is 0.40. Spice is a normal good. An increase in incomes cause the market PRICE of spices to rise by 3%. What is the percentage change in market QUANTITY? Notes: Enter a number only, do not include the % sign. If it decreases, include a negative sign before your number. For example, if it is a 15.675% decrease, enter -15.68 not -0.15. If quantity decreases include a negative sign.arrow_forward

- Operation managementarrow_forwardFarmer Johnson producers Eggs in a perfectly competitive egg market. The short run cost curves are displayed below. $4.00 MC $3.50 ATC AVC $3.00 $2.50 $2.00 $1.50 $1.00 $0.50 $0 20 40 60 80 100 120 140 160 Dozens of Eggs Price of Eggsarrow_forwardqD = 100 – 0.5p, qS = 2p – 20 What is the price elasticity of supply? Is the situation modeled here more likely to be reflecting a short- or long-run equilibrium? Why?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education