FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

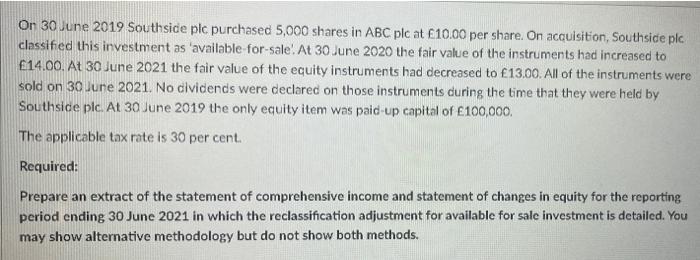

Transcribed Image Text:On 30 June 2019 Southside plc purchased 5,000 shares in ABC plc at £10.00 per share. On acquisition, Southside plc

classified this investment as 'available-for-sale!. At 30 June 2020 the fair value of the instruments had increased to

£14.00. At 30 June 2021 the fair value of the equity instruments had decreased to £13.00. All of the instruments were

sold on 30 June 2021. No dividends were declared on those instruments during the time that they were held by

Southside plc. At 30 June 2019 the only equity item was paid-up capital of £100,000.

The applicable tax rate is 30 per cent.

Required:

Prepare an extract of the statement of comprehensive income and statement of changes in equity for the reporting

period ending 30 June 2021 in which the reclassification adjustment for available for sale investment is detailed. You

may show alternative methodology but do not show both methods.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- What are the accounting ramifications of each of the three following situations involving the payment of contingent consideration in an acquisition? a. P Company issues 100,000 shares of its $50 fair value ($1 par) common stock as payment to buy S Company on January 1, 2015. P agrees to pay $100,000 cash two years later if S income exceeds an income target. The target is exceeded. b. P Company issues 100,000 shares of its $50 fair value ($1 par) common stock as payment to buy S Company on January 1, 2015. P agrees to issue 10,000 additional shares of its stock two years later if S income exceeds an income target. The target is exceeded. c. P Company issues 100,000 shares of its $50 fair value ($1 par) common stock as payment to buy S Company on January 1, 2015. P agrees to issue 5,000 additional shares two years later if the fair value of P shares falls below $50 per share. Two years later, the stock has a fair value below $50, and added shares are issued to S.arrow_forwardBrick Ltd acquired 80% of the shares in Mortar Ltd on 1 January 2019 for an initial consideration of £39,000,000 cash and a further £13,000,000 will be paid on 1 January 2021. On 1 January 2019, Mortar Ltd had retained earnings of £7,800,000 and the market price of its shares was £1.50 per share. The Statement of Financial Position of Brick Ltd and its subsidiary Mortar Ltd as at 31 December 2019 are as follows: Brick Ltd £000 Mortar Ltd £000 Non-current Assets: Property, plant and equipment at cost 65,000 52,000 Investment in Mortar Ltd 50,791 115,791 52,000 Current Assets: Inventories 3,900 10,400 Trade receivables: Brick Ltd 13,000 Other 20,800 9,100 Cash 2.600 27.300 32,500 84,500 Total Assets 143.091 Equity and Liabilities Еquity Ördinary Share Capital at £1 each 58,500 32,500 Revaluation Reserve 15,600 6,500 Retained earnings 33,210 107,310 36.400 75,400 Liabilities Non-Current Liabilities: Deferred consideration for Investment in Mortar Ltd. 12,381 Current Liabilities: 10,400…arrow_forwardOn 1 July 2019, Michelle Ltd acquired all the issued shares of Tracy Ltd, paying $250 000 cash. At that date, the financial statements of Tracy Ltd showed the following information. Share capital Retained earnings $100 000 100 000 All the assets and liabilities of Tracy Ltd were recorded at amounts equal to their fair values at the acquisition date, except some inventories recorded at $10 000 below their fair value. Also, Michelle Ltd identified at acquisition date a patent with a fair value of $40 000 that Tracy Ltd has not recorded in its own accounts. Required 1. Prepare the acquisition analysis at 1 July 2019. 2. Prepare the consolidation worksheet entries for Michelle Ltd's group at 1 July 2019. 3. Discuss how the answers for 1 and 2, above, would change if the Michelle Ltd paid only $200 000 cash for the shares in Tracy Ltd.arrow_forward

- Victoria Corp acquired 80 per cent of the share capital of Whitehorse Corp on 1 July 2019. As at the date of acquisition, Whitehorse’s retained earnings was $40,000. On this date, the fair value of the 20% non-controlling interest in Whitehorse was $25,000. Ignore the tax rate. The statements of the financial position of Victoria Corp and Whitehorse Corp as at 30 June 2020 are as follows: Victoria Corp ($) Whitehorse Corp ($) Current assets 320,000 168,000 Non-current assets: Property, plant and equipment 190,000 36,000 Investment (in Whitehorse) 100,000 - 290,000 36,000 610,000 204,000 Current liabilities 270,000 94,000 Shareholders’ equity: Share capital…arrow_forwardTrump Ltd acquired all the assets and liabilities of Bush Ltd on 30 June 2020. The purchase consideration was as follows: • $1,000,000 in cash paid on acquisition date • Two shares in Trump Ltd for every one share in Bush Ltd. Bush Ltd has 2,000,000 shares on issue at 30 June 2020. At 30 June 2013 Trump Ltd shares were quoted on the ASX at $2.50 per share. • A deferred payment of $500,000 to be paid on 30 June 2014.Trump Ltd’s cost of capital is 7% which represents a one period present value factor of 0.9346 • Should the price of Trump Ltd shares fall below $2.50 in the six months following the acquisition Trump Ltd is required to pay a cash contingent consideration. It is estimated that there is a 60% probability that the share price will fall to $2.45 in this period. Other information - Trump Ltd incurred legal and other costs associated with the acquisition of $10,000 - Trump Ltd incurred share issue costs of $4,000 The assets and liabilities acquired from Bush Ltd are as…arrow_forwardOn December 1, 2019, PT ABC exchanged 20.000 shares of its Rp10 par value ordinary shares held in treasury for a used machine. The treasury shares were acquired by ABC at a cost of Rp40 per share, and are accounted for under the cost method. On the date of the exchange, the ordinary shares had a fair value of Rp55 per share (the shares were originally issued at Rp30 per share). As a result of this exchange, ABC’s total equity will increase by:arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education