FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

Note:-

- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism.

- Answer completely.

- You will get up vote for sure.

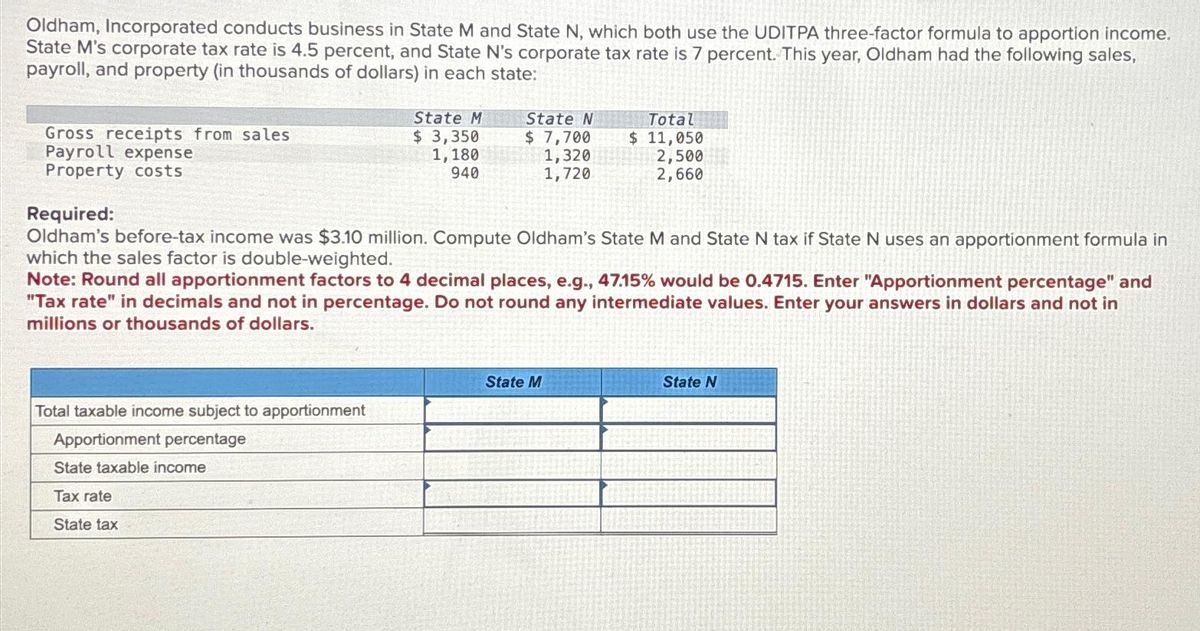

Transcribed Image Text:Oldham, Incorporated conducts business in State M and State N, which both use the UDITPA three-factor formula to apportion income.

State M's corporate tax rate is 4.5 percent, and State N's corporate tax rate is 7 percent. This year, Oldham had the following sales,

payroll, and property (in thousands of dollars) in each state:

Gross receipts from sales

Payroll expense

Property costs

State M

$ 3,350

1,180

940

Total taxable income subject to apportionment

Apportionment percentage

State taxable income

Tax rate

State tax

State N

$ 7,700

1,320

1,720

Required:

Oldham's before-tax income was $3.10 million. Compute Oldham's State M and State N tax if State N uses an apportionment formula in

which the sales factor is double-weighted.

Note: Round all apportionment factors to 4 decimal places, e.g., 47.15% would be 0.4715. Enter "Apportionment percentage" and

"Tax rate" in decimals and not in percentage. Do not round any intermediate values. Enter your answers in dollars and not in

millions or thousands of dollars.

Total

$ 11,050

2,500

2,660

State M

State N

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Please dont give plagiarised answers thnkuarrow_forwardTacit or implicit knowledge, is personal, experiential, context-specific, and hard to formalize and communicate. True Falsearrow_forwardThe legal environment has little impact on human resource management decision making. Question 22 options: True Falsearrow_forward

- discuss how critical thinking skills will make you less likely to be influenced by arguments that are based on fallacies and faulty reasoning.arrow_forwardProvide best Answer As per posible fastarrow_forwardCritically evaluate how the breach of ethics by auditors could contribute to expand the audit expectation gap. Your report should include/address the following concerns: 1. Introduce/analyze ethical aspect of auditors and audit expectation gap. 2. Critically examine how different threats to ethics enlarge the audit expectation gap. 3. Propose ways to minimize the threats to ethics and thus the expectation gap of audits. 4. Determine the current developments and future direction of ethical aspects of auditors, and explain how such developments contribute to safeguard the audit profession as a concluding remarks. Include a cover page, an executive summary, a table of contents and references. You may include an appendix if necessary.arrow_forward

- Karen finds that many claim forms were rejected because important information was omitted. How might Karen suggest corrections for these omissions?arrow_forwardWhat is risk of incorrect acceptance? A. The risk that the auditor concludes that a material misstatement exists when it does not exist. B. The risk that the auditor concludes that a material misstatement does not exist when it actually does not. C. The risk that the auditor concludes that a material misstatement does not exist when it does exist. D. The risk that the auditor concludes that a material misstatement exists when it actually does.arrow_forwardUrgent Please answer a soon as possible. Answer must be plagirism free What is the role of auditors and explain the importance of the role.arrow_forward

- 1. Choose the ethical considerations that Amahle Khumalo should recognize in deciding how to proceed. Note: You may select more than one answer. Single click the box with the question mark to produce a check mark for a correct answer and double click the box with the question mark to empty the box for a wrong answer. Any boxes left with a question mark will be automatically graded as incorrect. Check my work is not available. Khumalo should exercise initiative and good judgment in providing management with information having a potentially adverse economic impact Khumalo should determine whether the controller's request violates her professional or personal standards or the company's code of ethics. ? Khumalo should protect proprietary information and should not violate the chain of command by discussing this matter with the controller's superiors ?Khumalo should not try to convince the controller regarding the probable failure of reworks.arrow_forwardQuite often, people may face situations that put them in an ethical conflict. The best way to cope with this is ________. Question 22 options: A) to develop a personal code of ethical conduct about what is right and wrong B) to use the "golden rule" C) to do what makes the largest number of people happy in the situation D) to do nothing and ignore the situation E) to act the same way you have seen others act in similar situationsarrow_forwardSearch Google images for bad data visualizations. Post a link to the image.Describe what is inaccurate or misleading about the visualization. Replace the inaccurate and misleading information with what you think makes the image a good visualization.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education