ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Please answer the blank spaces below:

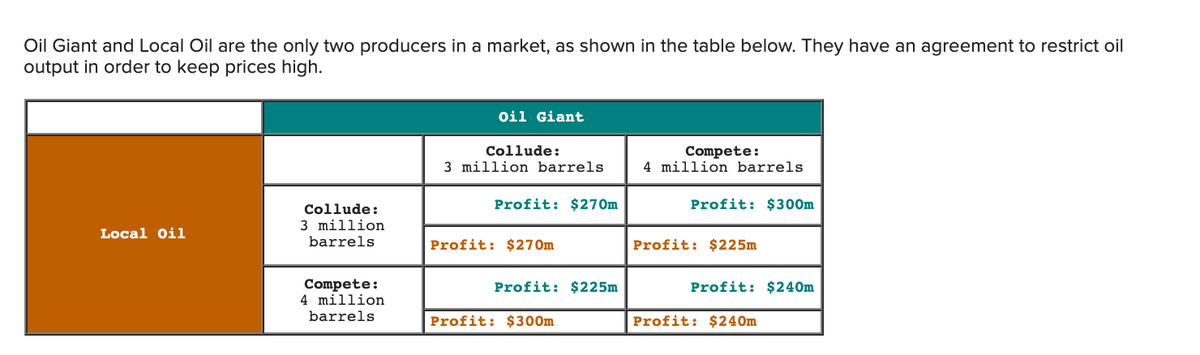

1. At the Nash equilibrium, Local Oil earns a profit of $______ m, and Oil Giant earns a profit of $_______ m. [enter the numbers only]

Transcribed Image Text:Oil Giant and Local Oil are the only two producers in a market, as shown in the table below. They have an agreement to restrict oil

output in order to keep prices high.

Oil Giant

Compete:

4 million barrels

Collude:

3 million barrels

Profit: $270m

Profit: $300m

Collude:

3 million

Local Oil

barrels

Profit: $270m

Profit: $225m

Compete:

4 million

barrels

Profit: $225m

Profit: $240m

Profit: $300m

Profit: $240m

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Give typing answer with explanation and conclusionarrow_forwardConsider an economy with 2 goods, H consumers and m firms. Each consumer, h, has an endowment of 2 units of good 1 and none of good 2, preferences described by a. Calculate a firm’s profit-maximizing choices, a consumer’s demands and the competitive equilibrium of the economy. b. What happens to as (i) m increases; (ii) H increases? Why? c. Suppose that each consumer’s endowment of good 1 increases to 2 + 2δ. Explain the change in relative prices. d. What is the effect of changing: i. The distribution of endowments among consumers; ii. The consumers’ preferences toarrow_forward1arrow_forward

- 4 The Competitive Equilibrium Model—Deriving Supply] Negar owns a trendy and sustainable shoe factory. The total cost of producing a given number of pairs of shoes is displayed in the table below. Assume Negar can only produce the integer quantities of pairs of shoes specified in the table. Number of pairs Total Cost 0 400 10 410 20 430 30 460 40 500 50 580 60 680 70 800 b. Draw the supply curve for Negar’s shoe factory. c. Suppose the wholesale market for shoes that sell to retail stores is competitive, with a market price of $10 per pair (i.e., $100 per 10 pairs). If Negar’s goal is to maximize profits, how many pairs will she choose to sell? d. What are Negar’s profits when she sells the number of pairs from (c) at the market price of $10? e. Calculate Negar’s producer surplus given the price and quantity from part (c). How does this compare to the profit calculated in part (d)?arrow_forwardHomework (Ch 06) Back to Assignment Attempts Do No Harm / 1 3. Effects of rent control Rent controls force landlords to price apartments below the equilibrium price level. An immediate effect is a shortage (excess demand) of apartments, because the quantity of apartments demanded is greater than the quantity supplied at the regulated price. When cities prevent landlords from charging market rents, which of the following are common long-run outcomes? Check all that apply. O Landlords earn lower profits from renting housing units, but the rent charged has no effect on either the quantity or quality of rental units. O The future supply of rental housing units increases. O Black markets develop. O The quality of rental housing units falls.arrow_forwardPrice and cost (dollars per ride) The graph shows the market for the two zipline firms that operate in a resort city. If the firms decide to compete, then together they will produce rides at a price of per ride. 60 O A. 400: $30 MC O B. 400; $50 50 O C. between 200 and 400: between $30 and $50 40 O D. 200: $30 O E. 200; $50 30 20 'D 10 MR 100 200 300 400 500 Quantity (number of rides)arrow_forward

- 1. Characteristics of competitive markets The model of competitive markets relies on these three core assumptions: 1. There must be many buyers and sellers-a few players can't dominate the market. 2. Firms must produce an identical product-buyers must regard all sellers' products as equivalent. 3. Firms and resources must be fully mobile, allowing free entry into and exit from the industry. The first two conditions imply that all consumers and firms are price takers. While the third is not necessary for price-taking behavior, assume for this problem that a market cannot maintain competition in the long run without free entry. Identify whether or not each of the following scenarios describes a competitive market, along with the correct explanation of why or why not. Scenario There are hundreds of colleges that serve millions of students each year. The colleges vary by location, size, and educational quality, which enables students with diverse preferences to find schools that match…arrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward2. Suppose that the market for wind chimes is a competitive market. The following graph shows the daily cost curves of a particular firm operating in this PRICE (Dollars per wind chime) 40 b) 36 32 28 24 20 16 2 8 4 0 MC 0 2 4 + 10 12 14 16 18 20 QUANTITY (Thousands of wind chimes per day) 8 market: a) In short run, at a market price of $26 per wind chime how much will firm ATC AVC 6 the market price is $26 in th quantity you obtained in question (a), indicate the area that represents firm's profit or loss in short run on the graph. c) What is this firm's shutdown price, that is the price below which it is optimal for the firm to shut down in short run? d) In the long run, all firms can enter and exit the market, and all entrants have the same costs as above. As this market makes the transition to its long-run equilibrium, will the price rise or fall? Will the quantity demanded rise or fall? Will the quantity supplied by each firm rise or fall? Explain your answers. e) Graph the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education