FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

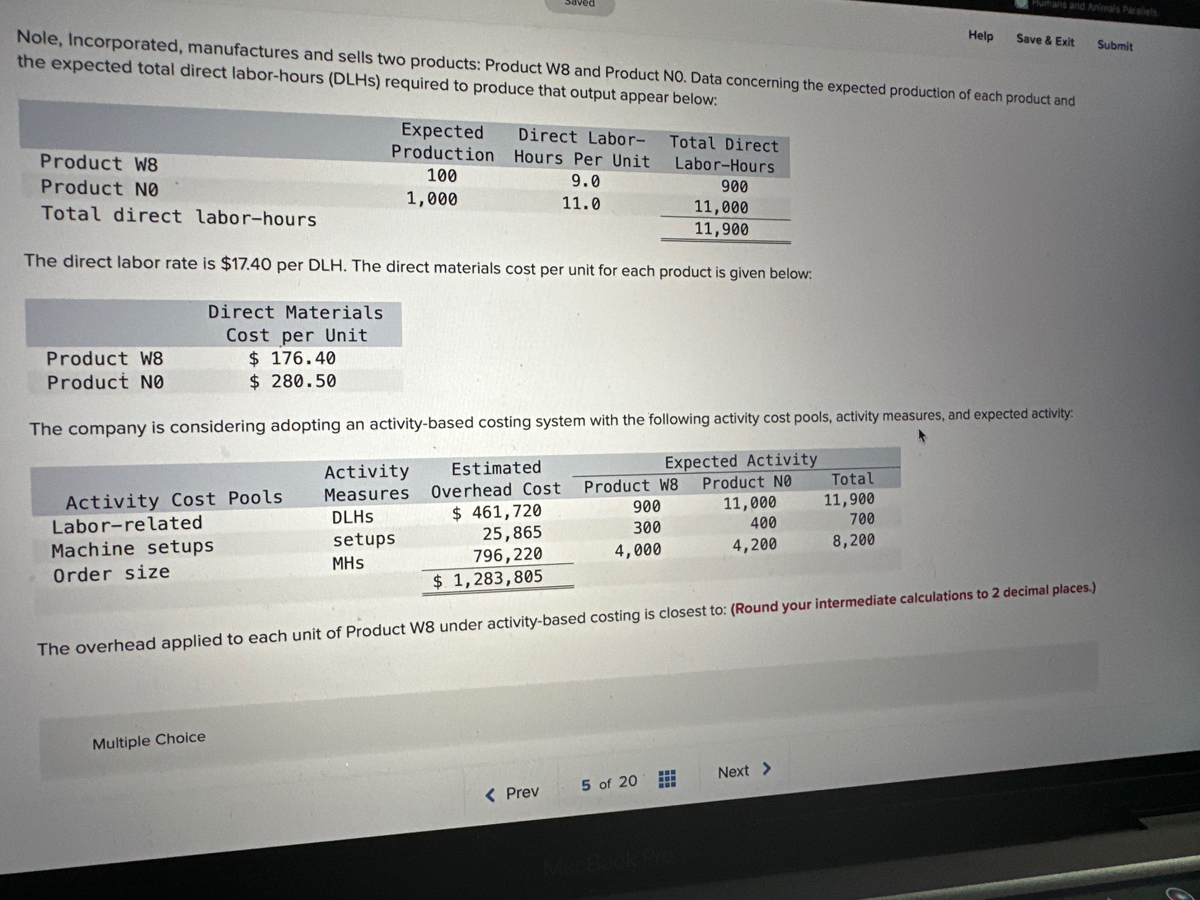

Transcribed Image Text:Nole, Incorporated, manufactures and sells two products: Product W8 and Product NO. Data concerning the expected production of each product and

the expected total direct labor-hours (DLHs) required to produce that output appear below:

Product W8

Product NO

Total direct labor-hours

Total Direct

Labor-Hours

900

11,000

11,900

The direct labor rate is $17.40 per DLH. The direct materials cost per unit for each product is given below:

Direct Materials

Cost per Unit

$ 176.40

$ 280.50

Product W8

Product NØ

Expected

Production

100

1,000

Activity Cost Pools

Labor-related

Machine setups

Order size

Direct Labor-

Hours Per Unit

9.0

11.0

The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity:

Expect

Activity

Product NO

11,000

400

4,200

Multiple Choice

Activity

Measures

DLHS

setups

MHS

Estimated

Overhead Cost

$461,720

25,865

796,220

$ 1,283,805

The overhead applied to each unit of Product W8 under activity-based costing is closest to: (Round your intermediate calculations to 2 decimal places.)

Product W8

900

300

4,000

< Prev

5 of 20

Hurhans and Animals Parallels

Save & Exit Submit

Help

Total

11,900

700

8,200

Next >

Transcribed Image Text:Multiple Choice

$1,167.10 per unit.

$970.92 per unit

The overhead applied to each unit of Product W8 under activity-based costing is closest to: (Round your intermediate calculations to 2 decimal places.)

$3,884.00 per unit

796,220

$1,283,805

$4,344.05 per unit

4,000

< Prev

5 of 20

400

4,200

MacBook Pro

700

8,200

Next >

G

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Chhom, Inc., manufactures and sells two products: Product F9 and Product U4. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Product F9 500 4 2,000 Product U4 1,000 2 2,000 Total direct labor-hours 4,000 The direct labor rate is $25.50 per DLH. The direct materials cost per unit is $274 for Product F9 and $222 for Product U4. The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Expected Activity Activity Cost Pools Activity Measures Overhead Cost Product F9 Product U4 Total Labor-related DLHs $ 31,900 2,000 2,000 4,000 Production orders orders 50,640 600 1,000 1,600 Order size MHs 103,200 3,300 2,600 5,900 $ 185,740 If the company allocates all of its overhead based on direct labor-hours using its…arrow_forwardShip Co. produces storage crates that require 1.2 meters of material at $.85 per meter and 0.1 direct labor hours at $15.00 per hour. Overhead is applied at the rate of $9 per direct labor hour. What is the total standard cost for one unit of product that would appear on a standard cost card?arrow_forwardDengerarrow_forward

- (The following information applies to the questions displayed below.) Martinez Company's relevant range of production is 7,500 units to 12,500 units. When it produces and sells 10,000 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Average Cost Per Unit $ 5.30 $ 2.80 $ 1.40 $4.00 $ 2.30 $2.20 $ 1.20 $ 0.45 2. For financial accounting purposes, what is the total amount of period costs igcurred to sell 10,000 units? (Do not round intermediate calculations.) Total period costarrow_forwardTesh, Inc., manufactures and sells two products: Product P9 and Product I9. Data concerning the expected production of each product and the expected total direct labour-hours (DLHs) required to produce that output appear below: Expected Production Direct Labour-Hours Per Unit Total Direct Labour-Hours Product P9 200 7.0 1,400 Product I9 400 6.0 2,400 Total direct labour-hours 3,800 The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Expected Activity Activity Cost Pools Activity Measures Overhead Cost Product P9 Product I9 Labour-related DLHs $71,136 1,400 2,400 Machine setups setups 42,880 300 200 General factory MHs 406,620 4,200 3,900 $520,636 The activity rate for the Machine setups activity cost pool under activity-based costing is closest to: a. $1,041.27 per setup b. $85.76 per setup c. $214.40 per setup d.…arrow_forwardSheddon Industries produces two products. The products' identified costs are as follows: Direct materials. Direct labor Multiple Choice The company's overhead costs of $55,000 are allocated based on direct labor cost. Assume 5,000 units of product A and 6,000 units of product B are produced. What is the cost per unit for product B? Note: Do not round intermediate calculations. $12.56 $14.56 Product A $ 21,000 15,000 $14.19 Product B $ 16,000 25,000arrow_forward

- Cane Company manufactures two products called Alpha and Beta that sell for $125 and $85, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 101,000 units of each product. Its average cost per unit for each product at this level of activity are given below: Direct materials Direct labor Variable manufacturing overhead Traceable fixed manufacturing overhead Variable selling expenses Common fixed expenses Total cost per unit Alpha $ 30 21 8 Traceable fixed manufacturing overhead 17 13 16 $ 105 Alpha Beta The company considers its traceable fixed manufacturing overhead to be avoidable, whereas its common fixed expenses are unavoidable and have been allocated to products based on sales dollars. $12 20 Required: 1. What is the total amount of traceable fixed manufacturing overhead for each of the two products? Beta 19 9 11 $ 77arrow_forwardDhapaarrow_forwardELU Company makes two products in a single facility. These products have the following unit product costs: Product A Product B Direct materials $10.90 $15.80 Direct labour 12.50 12.60 Variable manufacturing overhead 2.40 1.20 Fixed manufacturing overhead 11.60 7.20 Unit product cost $37.40 $36.80 Additional data concerning these products are listed below. Product A Product B Mixing minutes per unit 2.00 1.00 Selling price per unit $55.80 $54.60 Variable selling cost per unit $2.10 $1.40 Monthly demand in units 2,000 1,000 The mixing machines are potentially a constraint in the production facility. A total of 4,000 minutes are available per month on these machines. Direct labour is a variable cost in this company. Required: How many minutes of mixing machine time would be required to satisfy demand for both products? How many of each product should be produced, rounded to the nearest…arrow_forward

- Dinesh Bhaiarrow_forwardSalvatori, Inc., manufactures and sells two products: Product A4 and Product Q5. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Expected Production Direct Labor-Hours Per Unit Total Direct Labor-Hours Product A4 690 7.9 5,451 Product Q5 990 4.9 4,851 Total direct labor-hours 10,302 The company has an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Expected Activity Activity Cost Pools Activity Measures Overhead Cost Product A4 Product Q5 Total Labor-related DLHs $ 167,558 5,451 4,851 10,302 Machine setups setups 15,050 1,250 1,150 2,400 Order size MHs 504,027 5,100 5,400 10,500 $ 686,635 The overhead applied to each unit of Product A4 under activity-based costing is closest to: (Round your intermediate calculations to 2 decimal places.)arrow_forwardYour Company makes three products in a single facility. These products have the following unit product costs: Product A Product B Product C Direct material $26.00 $26.00 $27.00 Direct labor 15.00 17.00 16.00 Variable manufacturing overhead 4.00 5.00 6.00 Fixed manufacturing overhead 21.00 28.00 23.00 Unit cost $66.00 $76.00 $72.00 Additional data concerning these products are listed below: Product A Product B Product C Mixing minutes per unit 3 2 2.5 Selling price per unit $76.00 $90.00 $84.00 Variable selling cost per unit $4.00 $3.00 $5.00 Monthly demand in units 1,500 3,000 4,000 The mixing machines are potentially the constraint in the production facility. A total of 18,000 minutes is available per month on these machines. Direct labor is a variable cost in this company. Required: How many minutes of mixing machine time would be required to satisfy demand for all three products?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education