Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

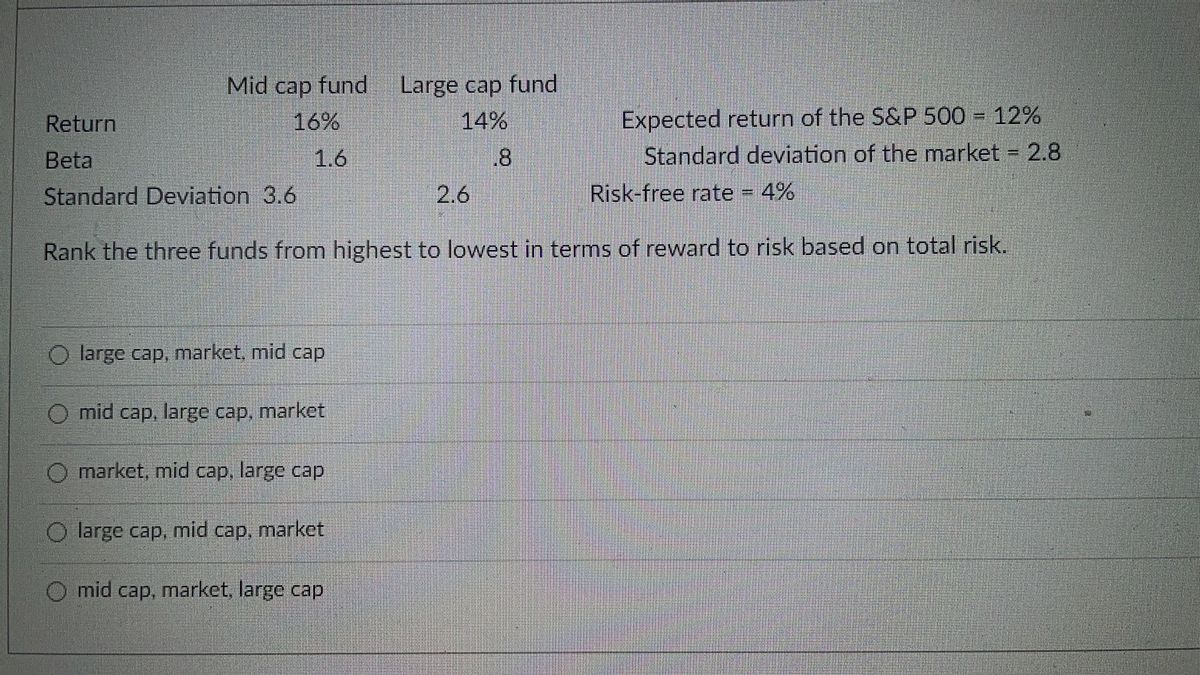

Transcribed Image Text:### Risk and Return Analysis

The table below provides data for two types of investment funds, mid cap and large cap, along with market-related information.

| | Mid Cap Fund | Large Cap Fund |

|----------------------------|--------------|----------------|

| **Return** | 16% | 14% |

| **Beta** | 1.6 | 0.8 |

| **Standard Deviation** | 3.6 | 2.6 |

Additional Market Information:

- **Expected Return of the S&P 500**: 12%

- **Standard Deviation of the Market**: 2.8

- **Risk-free Rate**: 4%

### Problem Statement

Rank the three options (including the market) from highest to lowest in terms of reward to risk based on total risk.

### Options

1. **large cap, market, mid cap**

2. **mid cap, large cap, market**

3. **market, mid cap, large cap**

4. **large cap, mid cap, market**

5. **mid cap, market, large cap**

When considering investments, understanding the balance between return and risk is crucial. Utilize this data to guide investment decisions by evaluating the reward-to-risk ratio.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- 6. Fund A Fund B Expected Ret. E(r) 13.4 % . 10.8% Standard Deviation - 13 %. 15.8% The table above contains expected annual returns for funds A and B. Assuming that the risk free rate is 2.55% and that the correlation of returns between funds A and B is -0.18, calculate the weight of Fund A in the minimum - variance two - risky asset portfolio comprised of funds A and B.arrow_forwardD4)arrow_forwardThe following performance data about the Big Gain Fund & the S&P 500 appears below Big Gain S&P 500 Return 40% 22% Standard Deviation 32 % 20% Beta Value 1.26 1.00 The risk free rate is 5% Required i. Calculate the sharpe ratio ii. The Treynor measure iii. And Jensen's iv. Comment on the results obtainedarrow_forward

- O B *Book Problem Walk Through Suppose you are the money manager of a $4.24 mbon investment fund the fund consists of four stocks with the following investments and beta Stock Beta 1.50 (0.00) 1.25 8.75 W Investment $320,000 500,000 1.320,000 1,000,000 C D the market's required rate of retums 11% and the risk free rate is what is the fund's requered rate of retum De not found intermedate caldabone Round your answer to two decimal placearrow_forwardIn the above $110K allocation problem, you decided to allocate 30% weight in A, 50% weight in B, 20% weight in C, and you want to find its AVG return. Which of the following is the appropriate method to find the mean (AVG) return on the $100K fund invested? a. Weighted Average (WAVG ) b. Simple Average c. Geometric Average d. Arithmetic Averagearrow_forwardINV 1 6d You have decided to invest in three mutual funds: one in equities, one in long corporate and government bonds, and a money market fund invested in T-bills yielding 5%. Your estimate of the relevant parameters for the equities and bond funds are as follows: Expected Return Standard Deviation Equities .15 .30 Bonds .06 .09 The correlation between the fund returns is 0.12. Without the money market fund, what would be the weights of a portfolio on the best feasible CAL, composed of the equities and bond funds which would be expected to return 10%, and what would be its standard deviation?arrow_forward

- Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 4%. The characteristics of the risky funds are as follows: Stock fund (S) Bond fund (B) Expected Return 23% 14 Standard Deviation The correlation between the fund returns is 0.12. Sharpe ratio 29% 17 What is the Sharpe ratio of the best feasible CAL? (Do not round intermediate calculations. Enter your answer as a decimal rounded to 4 places.) Check my workarrow_forwardINV 1 6f You have decided to invest in three mutual funds: one in equities, one in long corporate and government bonds, and a money market fund invested in T-bills yielding 5%. Your estimate of the relevant parameters for the equities and bond funds are as follows: Expected Return Standard Deviation Equities .15 .30 Bonds .06 .09 The correlation between the fund returns is 0.12. Compare the portfolios in #4 and #5. Is this consistent with what you would expect when adding the T-bill money market fund as essentially the risk-free asset?arrow_forwardProblem 6-6 (Algo) Consider the following table: Scenario Probability Stock Fund Rate of Return Bond Fund Rate of Return Severe recession 0.10 -44% -11% Mild recession 0.20 -24% 17% Normal growth 0.40 29% 10% Boom 0.30 34% -7% Required: a. Calculate the values of mean return and variance for the stock fund. (Do not round intermediate calculations. Round "Mean return" value to 1 decimal place and "Variance" to 2 decimal places.) b. Calculate the value of the covariance between the stock and bond funds. (Negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 2 decimal places.)arrow_forward

- 23. What return should be expected from investing in the market portfolio that is expected to yield 18% if the investment includes all of the investor's funds plus 30% additional funds borrowed at the risk-free rate of 6%? A. 18.6% B. 19.6% C. 21.6% D. 24.0%arrow_forward3. Problem 8.07 (Portfolio Required Return) BA eBook Problem Walk-Through Suppose you are the money manager of a $5.02 million investment fund. The fund consists of four stocks with the following investments and betas: Investment $ 260,000 600,000 1,560,000 2,600,000 с D If the market's required rate of return is 12% and the risk-free rate is 5%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. % Stock A B Beta 1.50 (0.50) 1.25 0.75arrow_forwardNonearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education