Essentials of Economics (MindTap Course List)

8th Edition

ISBN: 9781337091992

Author: N. Gregory Mankiw

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Related questions

Question

Not use ai please

Transcribed Image Text:Macmillan Learning

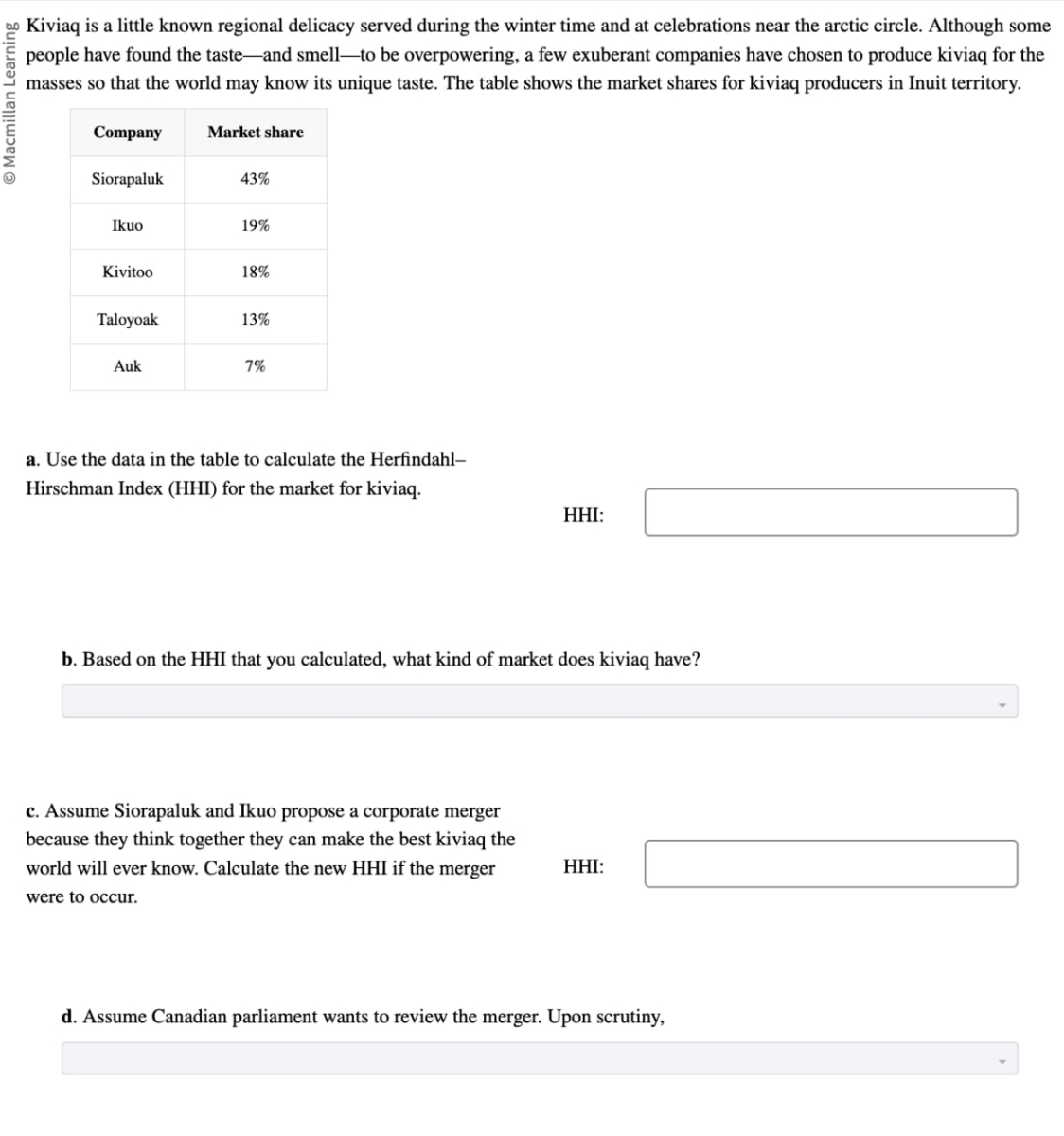

o Kiviaq is a little known regional delicacy served during the winter time and at celebrations near the arctic circle. Although some

people have found the taste-and smell—to be overpowering, a few exuberant companies have chosen to produce kiviaq for the

masses so that the world may know its unique taste. The table shows the market shares for kiviaq producers in Inuit territory.

Company

Market share

Siorapaluk

43%

Ikuo

19%

Kivitoo

18%

Taloyoak

13%

Auk

7%

a. Use the data in the table to calculate the Herfindahl-

Hirschman Index (HHI) for the market for kiviaq.

HHI:

b. Based on the HHI that you calculated, what kind of market does kiviaq have?

c. Assume Siorapaluk and Ikuo propose a corporate merger

because they think together they can make the best kiviaq the

world will ever know. Calculate the new HHI if the merger

were to occur.

HHI:

d. Assume Canadian parliament wants to review the merger. Upon scrutiny,

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 4 images

Knowledge Booster

Similar questions

- You own Athleticon, which manufactures athletic wear. Your new contract with Atlanta United, a professional soccer team, allows Athleticon to be the sole suppler of athletic wear with the “Atlanta United” logo. No one lese can manufacture athletic wear with the “Atlanta United” logo. What do you think will be Athleticon’s level of profitability on the sale of “Atlanta United” athletic wear? Explain why. Your contract with Atlanta United only lasts 3 years. It was not renewed. Other firms can now manufacture athletic wear with the “Atlanta United” logo It is now 5 years after your contract with Atlanta United was terminated. Any manufacturer that wants to can manufacture and sell athletic wear with the “Atlanta United” logo. What do you think will be the level of profitability and rate of return on manufacturing athletic wear with the “Atlanta United” logo? Explain why.arrow_forward(c) A discriminating monopolist is faced with the following price elasticities: e1-0.75 and What pricing policy should the monopolist adopt in the two markets? In which market will it be profitable for the monopolist to operate? Assume now that er ez 0.50, will it be advisable for the monopolist to discriminate or operate a single market? run. Briefly explain why the monopolist has no unique supply curve in the short Unlike the competitive firm, the monopoly firm can make supernormal profit in the long run. Explain why. e-1.50 i. ii. iii. iv. V.arrow_forwardA large share of the world supply of diamondscomes from Russia and South Africa. Suppose thatthe marginal cost of mining diamonds is constant at$1,000 per diamond and the demand for diamonds isdescribed by the following schedule:Price Quantity$8,000 5,000 diamonds7,000 6,0006,000 7,0005,000 8,0004,000 9,0003,000 10,0002,000 11,0001,000 12,000a. If there were many suppliers of diamonds, whatwould be the price and quantity?b. If there were only one supplier of diamonds, whatwould be the price and quantity?c. If Russia and South Africa formed a cartel, whatwould be the price and quantity? If the countriessplit the market evenly, what would be SouthAfrica’s production and profit? What wouldhappen to South Africa’s profit if it increased itsproduction by 1,000 while Russia stuck to thecartel agreement?d. Use your answers to part (c) to explain why cartelagreements are often not successful.arrow_forward

- Assuming you are the managing director of a firm that produces three goods: A, Band C. The price elasticity of demand for A is 1.2, for B it is 1.00 and for C it is 0.75.It is known that he firm is experiencing serious cash flow problems and you have toincrease total revenue as soon as possible. If you were in a position to set the pricesfor these goods, what would be your pricing strategy for each productarrow_forwardTyped plz and asap thanks I want quality solution pleasearrow_forward105 100 95 90+ 8282 85- 75 70- 382999282822" 65- 55 50 45 40 35 SH 5 10 15 MC ATC MR 60 65 Demand ++++ 90 95 100105110115120 Q What price will the monopolistically competitive firm charge in this market? O $70 $80 $75 $60arrow_forward

- follow. Table 13.1 Price (S) Quantity 4.00 2000 3.50 2400 3.00 2800 2.50 3200 2.00 3600 1.50 4000 1.00 4400 Refer to Table 13.1. If a monopoly faces the demand schedule given in the table, what is its marginal revenue from the 2400th unit it sells? A) $3.75 B) $1 C) $3.50 OD) $400arrow_forwardP1arrow_forwardGraph shows the cost and revenue information for Shitotsu the monopolist. What are the levels of price, output, total (sales) revenue. and total profits if the monopolist were to produce at the positions (a) through (d) indicated in table below? Costs and revenues 30 27 24 21 18 15 9 6 3 0 3 6 9 12 15 Quantity per period 18 21 MR D=AR MC ACarrow_forward

- PRICE (Dollars per engine) 100 90 80 70 60 40 30 & 2 20 10 MO D 0 10 ATC MR Demand 20 30 40 50 60 70 DO 90 QUANTITY (Thousands of engines) 100 Mon Comp Outcome Min Unit Cost Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that optimal quantity. Furthermore, a monopolistically competitive firm's average total cost in long-run equilibrium is average total cost. at the the minimumarrow_forward2. The market for dark chocolate us characterized by Cournot duopolists - Honeydukes and Wonka industries. The market demand for dark chocolate is:P = 8 - 0.005Qdwhere P is the price per bar in dollars and Qd is dark chocolate's daily quantity demanded in bars (use qh to represent the quantity of dark chocolate sold by Honeydukes and qw to represent the quantity of dark chocolate sold by Wonka Industries). Honeydukes has a constant marginal cost of $2.50 per bar, while Wonka Industries has a constant marginal cost of $3.00 per bar. The firms move simultaneously in choosing their profit-maximizing quantity of output.a. Given the firms move simultaneously, what is the equation for Honeydukes' reaction function with qh expressed as a function of qw?b. Given the firms move simultaneously, what is the equation for Wonka's reaction function with qw expressed as a function of qh?c. What quantity of dark chocolate will each firm produce in equilibrium and what price will be established for a…arrow_forwardWhat is a company based in Nova Scotia that you think shoud begin selling its products in a country outside of North America? who are some current competitors in that country and their marketing efforts.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning  Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc

Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:9781337091992

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax

Managerial Economics: Applications, Strategies an...

Economics

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:Cengage Learning

Exploring Economics

Economics

ISBN:9781544336329

Author:Robert L. Sexton

Publisher:SAGE Publications, Inc

Principles of Microeconomics

Economics

ISBN:9781305156050

Author:N. Gregory Mankiw

Publisher:Cengage Learning