FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

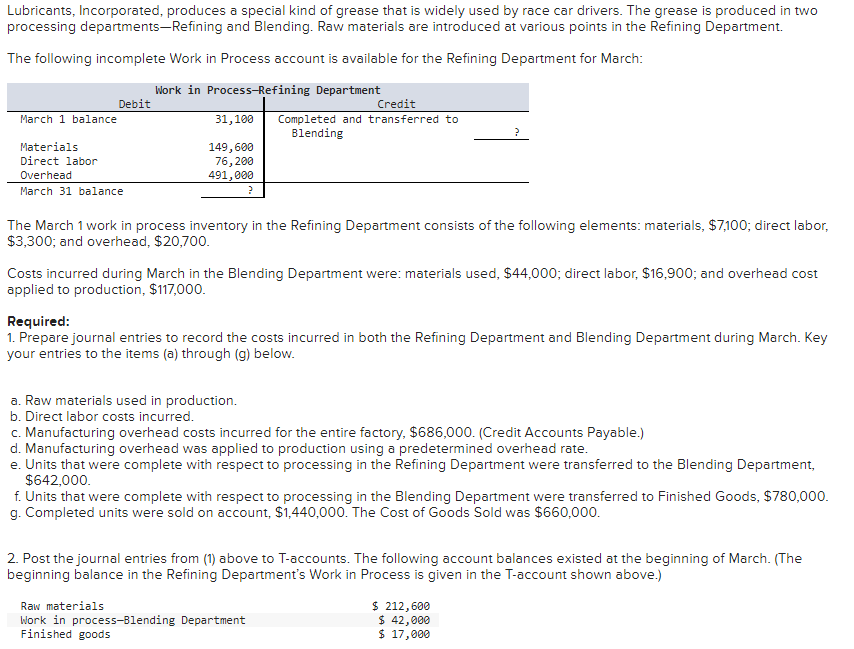

Transcribed Image Text:Lubricants, Incorporated, produces a special kind of grease that is widely used by race car drivers. The grease is produced in two

processing departments-Refining and Blending. Raw materials are introduced at various points in the Refining Department.

The following incomplete Work in Process account is available for the Refining Department for March:

March 1 balance

Debit

Materials

Direct labor

Overhead

March 31 balance

Work in Process-Refining Department

31,100

149,600

76,200

491,000

?

Credit

Completed and transferred to

Blending

The March 1 work in process inventory in the Refining Department consists of the following elements: materials, $7,100; direct labor,

$3,300; and overhead, $20,700.

Costs incurred during March in the Blending Department were: materials used, $44,000; direct labor, $16,900; and overhead cost

applied to production, $117,000.

Required:

1. Prepare journal entries to record the costs incurred in both the Refining Department and Blending Department during March. Key

your entries to the items (a) through (g) below.

a. Raw materials used in production.

b. Direct labor costs incurred.

c. Manufacturing overhead costs incurred for the entire factory, $686,000. (Credit Accounts Payable.)

d. Manufacturing overhead was applied to production using a predetermined overhead rate.

e. Units that were complete with respect to processing in the Refining Department were transferred to the Blending Department,

$642,000.

f. Units that were complete with respect to processing in the Blending Department were transferred to Finished Goods, $780,000.

g. Completed units were sold on account, $1,440,000. The Cost of Goods Sold was $660,000.

2. Post the journal entries from (1) above to T-accounts. The following account balances existed at the beginning of March. (The

beginning balance in the Refining Department's Work in Process is given in the T-account shown above.)

Raw materials

Work in process-Blending Department

Finished goods

$ 212,600

$ 42,000

$ 17,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Sharma Company has three process departments: Mixing, Encapsulating, and Bottling. At the beginning of the year, there were no work-in-process or finished goods inventories. The following data are available for the month of July: Department ManufacturingCosts Added* Ending Work inProcess Mixing $88,700 $20,200 Encapsulating 77,140 17,570 Bottling 72,450 3,380 *Includes only the direct materials, direct labor, and the overhead used to process the partially finished goods received from the prior department. The transferred-in cost is not included. Required: Question Content Area 1. Prepare journal entries that show the transfer of costs (a) from Mixing to Encapsulating, (b) from Encapsulating to Bottling, and (c) from Bottling to finished goods inventory. a. - Select - - Select - b. - Select - - Select - c. - Select - - Select - Question Content Area 2. Post the entries made in…arrow_forward! Required information [The following information applies to the questions displayed below.] Clopack Company manufactures one product that goes through one processing department called Mixing. All raw materials are introduced at the start of work in the Mixing Department. The company uses the weighted-average method of process costing. Its Work in Process T-account for the Mixing Department for June follows (all forthcoming questions pertain to June): June 1 balance Materials Direct labor Overhead June 30 balance Debit Work in Process-Mixing Department 27,000 151, 100 95,500 113,000 Equivalent units of production for materials 4. Compute the equivalent units of production for materials. ? The June 1 work in process inventory consisted of 4,400 units with $14,100 in materials cost and $12,900 in conversion cost. The June 1 work in process inventory was 100% complete with respect to materials and 60% complete with respect to conversion. During June, 36,900 units were started into…arrow_forwardWhite Diamond Flour Company manufactures flour by a series of three processes, beginning with wheat grain being introduced in the Milling Department. From the Milling Department, the materials pass through the Sifting and Packaging departments, emerging as packaged refined flour. The balance in the account Work in Process—Sifting Department was as follows on July 1:Work in Process—Sifting Department (900 units, 3/5 completed) on July 1Cost Source Dollar AmountDirect Materials (900 x $3.15) $2,835Conversion (900 x 3/5 x $0.30) 162Total Materials and Conversion 2,997The following costs were charged to Work in Process—Sifting Department during July:Work in Process—Sifting DepartmentCost Source Dollar AmountDirect materials transferred from Milling Department: 15,700 units at $2.30 a unit $36,110Direct Labor 5,420Factory Overhead 2,384During July, 15,500 units of flour were completed. Work in Process—Sifting Department on July 31 was 1,100 units, 4/5 completed.Instructionsa. Prepare a cost…arrow_forward

- Lubricants, Incorporated, produces a special kind of grease that is widely used by race car drivers. The grease is produced in two processing departments-Refining and Blending. Raw materials are introduced at various points in the Refining Department. The following incomplete Work in Process account is available for the Refining Department for March: Work in Process-Refining Department Debit March 1 balance Materials Direct labor Overhead 34,800 Credit Completed and transferred to Blending ? 138,600 82,200 490,000 March 31 balance ? The March 1 work in process inventory in the Refining Department consists of the following elements: materials, $8,500; direct labor, $4,700; and overhead, $21,600. Costs incurred during March in the Blending Department were: materials used, $45,000; direct labor, $17,000; and overhead cost applied to production, $113,000. Required: 1. Prepare journal entries to record the costs incurred in both the Refining Department and Blending Department during March.…arrow_forward! Required information [The following information applies to the questions displayed below.] Clopack Company manufactures one product that goes through one processing department called Mixing. All raw materials are introduced at the start of work in the Mixing Department. The company uses the weighted-average method of process costing. Its Work in Process T-account for the Mixing Department for June follows (all forthcoming questions pertain to June): June 1 balance Materials Direct labor Overhead June 30 balance Debit Work in Process-Mixing Department Credit 27,000 Completed and transferred to Finished Goods 151, 100 95,500 113,000 ? The June 1 work in process inventory consisted of 4,400 units with $14,100 in materials cost and $12,900 in conversion cost. The June 1 work in process inventory was 100% complete with respect to materials and 60% complete with respect to conversion. During June, 36,900 units were started into production. The June 30 work in process inventory consisted of…arrow_forwardHearty Soup Co. uses a process cost system to record the costs of processing soup, which requires the cooking and filling processes. Materials are entered from the cooking process at the beginning of the filling process. The inventory of Work in Process—Filling on April 1 and debits to the account during April were as follows:Bal., 800 units, 30% completed:Direct materials (800 × $4.30) $ 3,440Conversion (800 × 30% × $1.75) 420 $ 3,860From Cooking Department, 7,800 units $34,320Direct labor 8,562Factory overhead 6,387During April, 800 units in process on April 1 were completed, and of the 7,800 units entering the department, all were completed except 550 units that were 90% completed.Charges to Work in Process—Filling for May were as follows:From…arrow_forward

- Required information [The following information applies to the questions displayed below.] Clopack Company manufactures one product that goes through one processing department called Mixing. All raw materials are introduced at the start of work in the Mixing Department. The company uses the weighted-average method of process costing. Its Work in Process T-account for the Mixing Department for June follows (all forthcoming questions pertain to June): June 1 balance Materials Direct labor Overhead June 30 balance Debit Work in Process-Mixing Department Credit 27,000 Completed and transferred to Finished Goods 151, 100 95,500 113,000 ? Conversion cost transferred to finished goods The June 1 work in process inventory consisted of 4,400 units with $14,100 in materials cost and $12,900 in conversion cost. The June 1 work in process inventory was 100% complete with respect to materials and 60% complete with respect to conversion. During June, 36,900 units were started into production. The…arrow_forwardRequired information [The following information applies to the questions displayed below.] Clopack Company manufactures one product that goes through one processing department called Mixing. All raw materials are introduced at the start of work in the Mixing Department. The company uses the weighted-average method of process costing. Its Work in Process T-account for the Mixing Department for June follows (all forthcoming questions pertain to June): June 1 balance Materials Direct labor Overhead June 30 balance Debit Work in Process-Mixing Department Total cost of conversion Credit 28,000 Completed and transferred to Finished Goods 147,630 93,500 111,000 ? The June 1 work in process inventory consisted of 4,600 units with $15,000 in materials cost and $13,000 in conversion cost. The June 1 work in process inventory was 100% complete with respect to materials and 60% complete with respect to conversion. During June, 37,100 units were started into production. The June 30 work in process…arrow_forwardMunabhaiarrow_forward

- Clopack Company manufactures one product that goes through one processing department called Mixing. All raw materials are introduced at the start of work in the Mixing Department. The company uses the weighted-average method of process costing. Its Work in Process T-account for the Mixing Department for June follows (all forthcoming questions pertain to June): June 1 balance Materials Direct labor Overhead June 30 balance Debit Foundational 4-14 (Algo) Work in Process-Mixing Department 27,000 154,205 98,500 116,000 ? Credit Completed and transferred to Finished Goods The June 1 work in process inventory includes 4,100 units with $14,700 in materials cost and $12,300 in conversion cost. The June 1 work in process inventory was 100% complete with respect to materials and 60% complete with respect to conversion. During June, 36,600 units were started into production. The June 30 work in process inventory consisted of 9,400 units 100% complete with respect to materials and 50% complete…arrow_forwardAlchemy Manufacturing produces a pesticide chemical and uses process costing. There are three processing departments Mixing, Refining, and Packaging. On January 1, the first department-Mixing-had no beginning inventory. During January, 52,000 fl. oz. of chemicals were started in production. Of these, 36,000 fl. oz. were completed and 16,000 fl. oz. remained in process. In the Mixing Department, all direct materials are added at the beginning of the production process, and conversion costs are applied evenly throughout the process. The weighted average method is used. At the end of the month, Alchemy calculated equivalent units of production. The ending inventory in the Mixing Department was 70% complete with respect to conversion costs. With respect to direct materials, what is the number of equivalent units of production in the ending inventory? OA. 16,000 equivalent units B. 36,000 equivalent units OC. 52,000 equivalent units OD. 11,200 equivalent units ***arrow_forwardLui Coffee Company roasts and packs coffee beans. The process begins by placing coffee beans into the Roasting Department. From the Roasting Department, coffee beans are then transferred to the Packing Department. The following is a partial work in process account of the Roasting Department at March 31: ACCOUNT Work in Process-Roasting Department ACCOUNT NO. Balance Balance Date Item Debit Credit Debit Credit March 1 Bal., 25,000 units, 10% completed 21,250 31 Direct materials, 600,000 units 31 Direct labor 450,000 471,250 31 Factory overhead 244,600 415,820 715,850 1,131,670 31 Goods transferred, 605,000 units 31 Bal., ? units, 45% completed ? Required: 1. Prepare a cost of production report, and identify the missing amounts for Work in Process-Roasting Department. If an amount is zero, enter "0". When computing cost per equivalent units, round to the nearest cent. Lui Coffee Company Cost of Production Report-Roasting Department Units Units charged to production: For the Month Ended…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education