ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

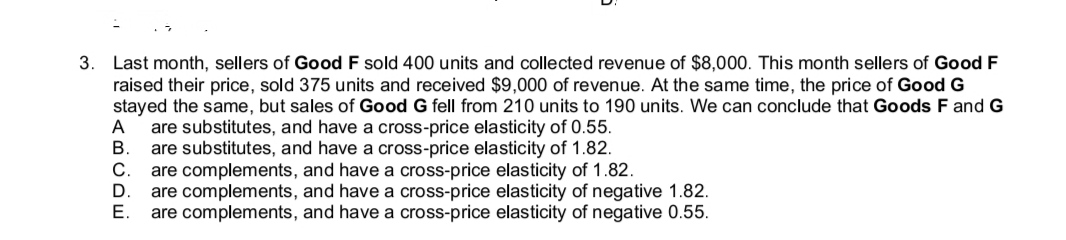

Transcribed Image Text:3. Last month, sellers of Good F sold 400 units and collected revenue of $8,000. This month sellers of Good F

raised their price, sold 375 units and received $9,000 of revenue. At the same time, the price of Good G

stayed the same, but sales of Good G fell from 210 units to 190 units. We can conclude that Goods F and G

are substitutes, and have a cross-price elasticity of 0.55.

are substitutes, and have a cross-price elasticity of 1.82.

are complements, and have a cross-price elasticity of 1.82.

are complements, and have a cross-price elasticity of negative 1.82.

are complements, and have a cross-price elasticity of negative 0.55.

A

BCDE

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- At $5 per cup, customers will buy 8 cups of coffee per week. At a price of $3, consumers are willing to buy 12 cups per week. The elasticity of the market demand curve for coffee between P = $5 and P = $3 (dropping all minus signs) isarrow_forwardRequired information You are the manager of a firm that receives revenues of $20,000 per year from product X and $80,000 per year from product Y. The own price elasticity of demand for product X is −3 and the cross-price elasticity of demand between products Y and X is −1.6. Suppose you increase the price of good X by 2 percent. Assume that the information about product X and product Y from the problem changed to the following: Revenues per year from product X $ 15,000 Revenues per year from product Y $ 80,000 Own price elasticity of demand for product X −3 Cross-price elasticity of demand between products X and Y −1.4 Price increase of product X (percent) 3 Instruction: Update the data in your spreadsheet to the values above and enter the recomputed answer for the original question. Required: How much will your firm’s total revenues (revenues from both products) change? Change in revenues: ____________________arrow_forwardWhen the price of good Y increases from $2 to $3, the quantity demanded for good X decreases from 20 units to 10 units. Using the Midpoint Method for Elasticity, what is the cross-price elasticity of demand between goods X and Y. (Round all decimal calculations to the closest ten-thousandths so your percentages are rounded to the closest hundredths; round your final answer to the closest hundredths.) Are goods X and Y complements or substitutes?arrow_forward

- The cross-price elasticity between the good sold in this market (call it X) and another good (Y) is εXY = –0.80. The cross-price elasticity between the good X and good Z, on the other hand, is εXZ = 1.50. Are X and Y substitutes, complements, or unrelated? How about X and Z? Explain.arrow_forwardWhen the price of good Y increases from $2 to $3, the quantity demanded for good X decreases from 20 units to 10 units. Calculate the cross-price elasticity of demand between goods X and Y. (Round all decimal calculations to the closest ten- thousandths so your percentages are rounded to the closest hundredths; round your final answer to the closest hundredths.) Are goods X and Y complements or substitutes?arrow_forwardYear 1 2 Income $10,000 $10,000 Price of Good X $5 $10 Using the above table and the Midpoint Method for Elasticity, suppose now that the income in year 1 increases from $10,000 to $20,000, and as a result, the quantity demanded for good y in year 1 changes from 20 units to 30 units. What is the income elasticity of demand for good Y in year 1? Is Y a normal or inferior good? Explain how you know whether it is a normal or inferior good. Blank 1 Income Elasticity of Demand: Blank 1 (Round your answer to TWO-decimal places; you MUST enter the decimal value even if it is a '0' - ie: 1.20 NOT 1.2.) Blank 2 Good Y is a Blank 2 (normal / inferior) good. Blank 3 Good Y is a normal/inferior good, because Blank 3. QD of Good X 10 units 8 units QD of Good Y 20 units 30 units Add your answer Add your answer Add your answerarrow_forward

- Suppose that a 10 percent increase in the price of normal good Y causes a 5 percent decrease in the quantity demanded of normal good X. The coefficient of cross elasticity of demand is Multiple Choice negative, and therefore these goods are substitutes. positive, and therefore these goods are substitutes. negative, and therefore these goods are complements. positive, and therefore these goods are complements..arrow_forwardDoes this imply that ice cream and frozen yogurt are complements or substitutes and does that answer match your intuition for whether or not ice cream and frozen yogurt are complements or substitutes? If not, how can you account for the value of the cross price elasticity implied by the data?arrow_forwardConsider the following demand function Qd=1000-4P2+6P*+5Y which describes how the demand Qd for a good depends on its price, P, the price P*of another good and income Y. Calculate the own-price elasticity, the cross price elasticity and income elasticity when P=10, P*=20 and Y=1000. Is demand elastic or inelastic? Are the goods complements or substitutes? Is demand normal?arrow_forward

- Assume the market demand for tuna cans may be written as Qtc = 45 - 2 x Ptc + Psc+ 0.3y (where Ptc = price of tuna cans and Psc = price of sardine cans, and y = income). Further assume that both tuna cans and sardine cans sell for $1 and income is $25. Calculate cross - price elasticity for tuna cans and identify whether the goods are substitutes or complements.arrow_forward3) When is demand said to be inelastic? a) when the quantity demanded changes proportionately more than price b) when the quantity demanded changes proportionately more than income c) when the quantity demanded changes proportionately less than price d) when the quantity demanded changes proportionately less than income 4) Suppose there is a 3 percent increase in the price of good X and a resulting 6 percent decrease in the quantity of X demanded. What is the price elasticity of demand for X? a) 0 b) 2 c) 6 d) infinitearrow_forwardI am stuck with this one?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education