ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

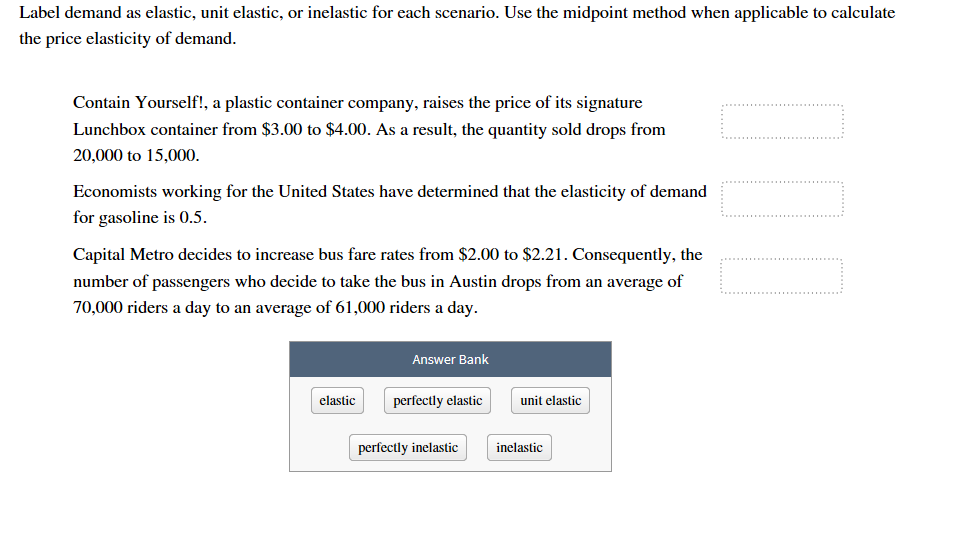

Transcribed Image Text:Label demand as elastic, unit elastic, or inelastic for each scenario. Use the midpoint method when applicable to calculate

the price elasticity of demand

Contain Yourself!, a plastic container company, raises the price of its signature

Lunchbox container from $3.00 to $4.00. As a result, the quantity sold drops from

20,000 to 15,000.

Economists working for the United States have determined that the elasticity of demand

for gasoline is 0.5

Capital Metro decides to increase bus fare rates from $2.00 to $2.21. Consequently, the

number of passengers who decide to take the bus in Austin drops from an average of

70,000 riders a day to an average of 61,000 riders a day.

Answer Bank

perfectly elastic

elastic

unit elastic

inelastic

perfectly inelastic

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 4 images

Knowledge Booster

Similar questions

- The table below gives part of the supply schedule for personal computers in the United States. Price Quantity Supplied before tech change $1,100 12,000 $900 8,000 a) Calculate the price elasticity of supply when price rises from $900 to $1,100 using the arc elasticity formula (the midpoint method). b) Now suppose that technology changes such that at every price, 1000 more computers are supplied. Now, as prices rise from $900 to $1,100, is the elasticity of supply smaller than, larger than, or equal to the elasticity in part a)? Price Quantity Supplied after tech change $1,100 13,000 $900 9,000 c) Does the change in b) change the slope of the supply curve? Are slope and elasticity the same thing? Explain.arrow_forwardWhich good would you expect to have a greater price elasticity of demand: a gallon of brand name ice cream sold at a grocery chain store in Phoenix or a gallon of ice cream sold at a specialty ice cream pallor in Phoenix. Why?arrow_forwardWhat is the formula for measuring the price elasticity of supply? Es = (Click to select)percentage change in quantity supplied / percentage change in pricepercentage change in quantity demanded / percentage change in incomepercentage change in quantity demanded / percentage change in price Suppose the price of apples goes up from $20 to $23 a box. In direct response, Goldsboro Farms supplies 1300 boxes of apples instead of 1200 boxes. Compute the coefficient of price elasticity (midpoints approach) for Goldsboro’s supply. Instructions: Round your answer to two decimal places. Es = Is its supply elastic, or is it inelastic? Supply is (Click to select)elasticinelastic.arrow_forward

- If the price elasticity of demand is equal to 0.5, is demand elastic, inelastic, or unitary elastic?arrow_forwardReview Question 1.2, If a 13 percent increase in the price of Cap'n Crunch cereal causes a 22 percent reduction in the number of boxes of cereal demanded, what is the absolute value of the price elasticity of demand calculation for Cap'n Crunch cereal? Epl= (Enter a numeric response using a real number rounded to two decimal places.) The demand for Cap'n Crunch isarrow_forwardTo calculate an elasticity coefficient of demand, we need to Divide the percentage change in the price by the percentage change in the quantity demanded Multiply the percentage change in the quantity demanded by the percentage change in the price Know the slope of the demand curve Multiply the percentage change in the price by the percentage change in the quantity demandedarrow_forward

- According to data from the U.S. Department of Energy, sales of the fuel-efficient Toyota Prius hybrid fell from 194,108 vehicles sold in 2014 to 180,603 in 2015. Over the same period, according to data from the U.S. Energy Information Administration, the average price of regular gasoline fell from $3.36 to $2.43 per gallon. Using the midpoint method, calculate the cross-price elasticity of demand between Toyota Priuses and regular gasoline. According to your estimate of the cross-price elasticity, are the two goods complements or substitutes? Does your answer make sense?arrow_forwardThe figure to the right illustrates the demand for taxi rides in a large city. Suppose the price per ride is initially $35 but then falls to $25 due to a recession. What is the price elasticity of demand for taxi rides? Using the midpoint formula, the price elasticity of demand is. (Enter your response rounded to two decimal places.) Demand is unit-elastic inelastic elastic C Price (dollars per taxi ride) 60- 55- 50- 45- 40- 35- 30- 25- 20- 15- 10- 5- 0+ 0 A B D 40,000 80,000 120,000 160,000 200,000 240, Quantity (taxi rides per day)arrow_forwardIf the price of product X increases from $10 to$12, the quantity demanded for gasoline (X) will fall from 100 to 82 and the quantity demanded for product Y also fall from 90 to 63 but the quantitydemanded for product Z will increases from 50 to76. a.What is price elasticity of demand for X?b.What is cross-price elasticity of demand for Ywith respect to price X? What are X and Y?c.What is cross-price elasticity of demand for Zwith respect to price X? What are X and Z?arrow_forward

- If Congress prohibited the sale of Japanese luxury cars like Lexus, Acura, and Infiniti, how would this affect the price elasticity of demand for Mercedes, BMWs, and Jaguars in the U.S.?arrow_forwardIn a study of the demand for automobiles in Canada, economists Blomqvist and Hassel distinguished between large and small cars and estimated the price and cross- price elasticities as well as the effects of the price of gasoline on the demands for small and large cars. Their results were as follows: a. C. New large cars New small cars d. Own price elasticity 1.26 2.30 Cross price elasticity 0.86 1.73 Elasticity with respect to gasoline price Note: The cross-price elasticities show that the demand for new small cars is more responsive to changes in the price of new large cars than the demand for new large cars is to changes in the price of new small cars. Do the cross-price elasticities have the expected sign? Briefly explain. b. If the price of new small cars went up by, say, 5 percent, by what percentage would new small car purchases change? {Note: In your answer to this and all of the remaining parts of this question, please indicate whether the change is an increase or a decrease.}…arrow_forwardAm. 112.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education