ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

Transcribed Image Text:KE

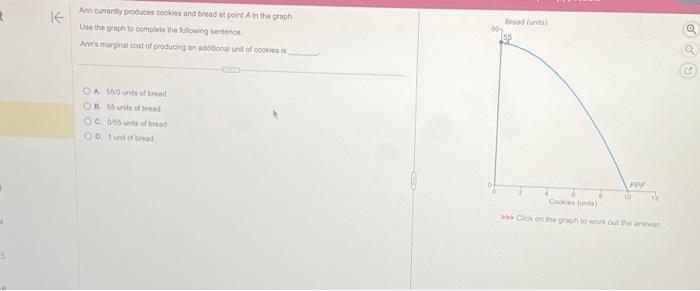

Ann currently produces cookies and bread at point A in the graph

Use the graph to complete the following sentence

Ann's marginal cost of producing an additional unit of cookies is

OA 550 units of bread

OB. 55 units of bread

OC 055 units of bread

OD 1 unt of bread

Bread (units)

PPE

Cookies (unit)

Click on the graph to work out the answer

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please explain how you decide what level of outputs you produce given a fixed level of an input. Show this on a graph.arrow_forwardnot use ai pleasearrow_forwardIII 123 Verdana 12 A A- Aa BIU abe X, x2 Styles 3. Complete the following table: See module 3 notes, chapter 13; there is a table that will show you how to work this. Total Average Average Average Marginal Variable Total cost Output Total Total Fixed Variable Cost Fixed Costs Cost 24 Cost Cost cost O$ 00で$ $50 $200 50.00 1. 45.00 000 06 2. 40.00 3. 4. 120 000 000 40.00 44.00 50.00 096 000 220 5. 6. 000 7. 8. 57.14 65.00 000 00 200 520 670 000 000 74.44 90.00 006 e 2 of 3 253 words E 00% Zoom Airarrow_forward

- what is efficient scale in economicsarrow_forwardPlease no written by hand solutionarrow_forwardWrite out an example Cobb-Douglas production function. Derive the signsfor the relationship between labor and output and for marginal product oflabor and labor, holding other inputs fixed. Explain with economic intuition.arrow_forward

- 5.3 A column on barrons.com discussing General Motors (GM) made the following observation: "Even the seemingly variable' costs of hourly workers were made burdensome by union agreements whereby 95% of hourly workers' salaries were paid when they were laid off, turning variable labor compensation into a fixed cost." a. Aren't workers' salaries always a variable cost and not a fixed cost? Briefly explain the author's reasoning. b. Suppose that GM reduces its production of cars. Compare what happens to GM's average total cost production in a situation where (i) the company doesn't have this union agreement, and (ii) the company does have this agreement. Use a graph to illustrate your answer.arrow_forward4. A decision at the margin Raphael is a hard-working college senior. One Saturday, he decides to work nonstop until he has answered 100 practice problems for his math course. He starts work at 8:00 AM and uses a table to keep track of his progress throughout the day. He notices that as he gets tired, it takes him longer to solve each problem. Time Total Problems Answered 8:00 AM 9:00 AM 40 10:00 AM 70 11:00 AM 90 Noon 100 Use the table to answer the following questions. The marginal, or additional, gain from Raphael's first hour of work, from 8:00 AM to 9:00 AM, is problems. The marginal gain from Raphael's third hour of work, from 10:00 AM to 11:00 AM, is problems. Later, the teaching assistant in Raphael's math course gives him some advice. "Based on past experience," the teaching assistant says, "working on 15 problems raises a student's exam score by about the same amount as reading the textbook for 1 hour." For simplicity, assume students always cover the same number of pages…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education