Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

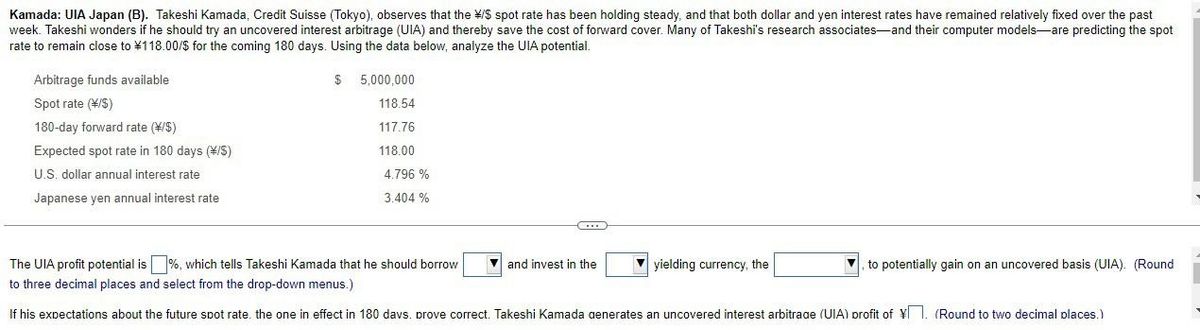

Transcribed Image Text:Kamada: UIA Japan (B). Takeshi Kamada, Credit Suisse (Tokyo), observes that the */$ spot rate has been holding steady, and that both dollar and yen interest rates have remained relatively fixed over the past

week. Takeshi wonders if he should try an uncovered interest arbitrage (UIA) and thereby save the cost of forward cover. Many of Takeshi's research associates and their computer models are predicting the spot

rate to remain close to ¥118.00/$ for the coming 180 days. Using the data below, analyze the UIA potential.

Arbitrage funds available

Spot rate (*/S)

180-day forward rate (\/$)

Expected spot rate in 180 days (\/S)

U.S. dollar annual interest rate

Japanese yen annual interest rate

$ 5,000,000

118.54

117.76

118.00

4.796 %

3.404 %

C

and invest in the

The UIA profit potential is %, which tells Takeshi Kamada that he should borrow

to three decimal places and select from the drop-down menus.)

If his expectations about the future spot rate, the one in effect in 180 days. prove correct. Takeshi Kamada generates an uncovered interest arbitrage (UIA) profit of ¥. (Round to two decimal places.)

yielding currency, the

to potentially gain on an uncovered basis (UIA). (Round

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardYou observe that the current interest rate on short-term U.S. Treasury bills is 4.86 percent. You also read in the newspaper that the GDP deflator, which is a common macroeconomic indicator used by market analysts to gauge the inflation rate, currently implies that inflation is 1.65 percent. What is the approximate real rate of interest on short-term Treasury bills? (Enter your answer as a percent rounded to 2 decimal places.)arrow_forwardYou were planning to purchase a house this month with a mortgage and just learned that the Fed is conducting open market purchase. Your situation is flexible in terms of the timing of the purchase; right now or later. It is assumed that everything else stays constant. What'd be the best strategy for your purchase? Explain using economic theory, not as a personal finance advisorarrow_forward

- In order to make CDs look more attractive than they really are, some banks advertise that their rates are higher than their competitors', but the fine print says that the rate is a simple interest rate. If a person deposits $15,000 at 7% per year simple interest, what compound interest rate would yield the same amount of money in 3 years? The compound interest rate that would yield the same amount of money in 3 years is 4.33 %.arrow_forwardHello, Just checking to see if this answer is correct. Please see below: Problem 1: The following two figures illustrate historical home price trend and interest rate for the 30-years fixed rate mortgage in the United States. Based on the information, please answer the following questions if today were in 2013. Assuming that history will repeat itself, what do you think of the U.S. housing market for the next 10 years? How about mortgage rate for the next 10 years? Based on your prediction, answer the two questions below: a)If you have money, should you invest in the housing market? b)If your answer in a) is “Yes”, and one lender allows you to borrow money, should you borrow money to buy the property? Why?arrow_forward(Related to Checkpoint 7.1) (Expected rate of return and risk) B. J. Gautney Enterprises is evaluating a security One-year Treasury bills are currently paying 3.1 percent. Calculate the investment's expected return and its standard deviation Should Gautney invest in this security? Probability 0.10 0.50 Return -6% 1% 5% 9% 0.30 0.10 (Click on the icon in order to copy its contents into a spreadsheet.) CID a. The investment's expected return is%. (Round to two decimal places)arrow_forward

- Step by step solutions pleasearrow_forwardConsider a CDS on Lehman Brothers default event. Given today’s market conditions you know that the present value of expected premium payments 6.0250*s, the present value of expected accrual payments is 0.0515*s and the present value of expected payoff is 0.1325. All measured per $1 of notional principal. You also know that Argo hedge fund bought this CDS on Lehman Brothers default from AIG one week ago with contractual rate of X basis points per year. Given this information the breakeven spread (i.e. the value of s) is _________ and today’s value of the CDS contract to AIG is positive if the value of s is _______ than X. a. 222 basis points;greater b. 218 basis points; smaller c. 218 basis points, greater d. 222 basis points; smaller e. 84 basis points; greater Please help and explainarrow_forwardThe amount of money (in billions of dollars) lent to customers with credit scores below 620 for subprime mortgages can be approximated by the function g(x) = 299.2e-0.15x, where x = 1 corresponds to the year 2001. (a) Find the value of subprime mortgage lending in 2011 for the described customer base. (b) If the trend continues, what is the first full year in which subprime lending falls below $4 billion? (a) Which of the following describes how to find the value of subprime mortgage lending in 2011 using the given information? Select the correct choice below and fill in the answer box to complete your choice. (Type an integer or a decimal.) A. To find the value of subprime mortgage lending in 2011, substitute g(x). for x and evaluate to find B. To find the value of subprime mortgage lending in 2011, find the intersection point of the graphs y=299.2e-0.15x and y=. The vahre of subprime mortgage lending in 2011 is represented by the y-coordinate. In 2011, the assets are about $ billion.…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education