ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

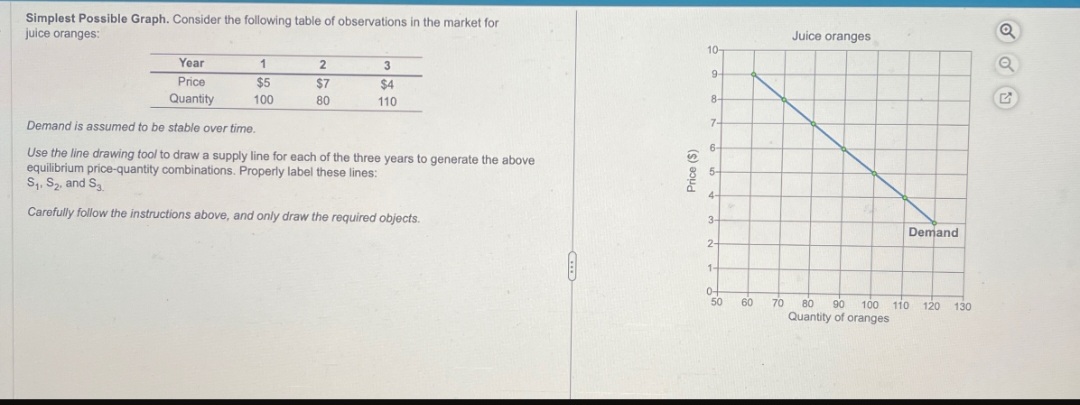

Transcribed Image Text:Simplest Possible Graph. Consider the following table of observations in the market for

juice oranges:

Year

1

2

3

Price

Quantity

$5

$7

$4

100

80

110

Demand is assumed to be stable over time.

Use the line drawing tool to draw a supply line for each of the three years to generate the above

equilibrium price-quantity combinations. Properly label these lines:

S₁, S2, and S3.

Carefully follow the instructions above, and only draw the required objects.

Price ($)

10-

9-

8-

7-

6-

4-

3-

Juice oranges

Demand

2-

1-

o+

50 60

70 80 90 100 110

120

130

Quantity of oranges

G

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 2. Assume that a firm has the following production function; q = L0.5K0.5. Its capital is fixed at K = 1. It faces a rental rate of r = $90 and a wage rate of W = $10. d. Determine the average, average variable, and average fixed cost functions. e. Determine the marginal cost function. f. Calculate the lowest cost, and associated quantity, that the firm can produce this good for in the short run.arrow_forwardSuppose that you are the vice president of operations of a manufacturing firm that sells an industrial lubricant. Further suppose that your economist gives you the following supply and demand equations: Supply equation: QS = 0.5P-20 Demand equation: P = 100 a ) Calculate the equilibrium price and quantity that characterizes this good b) Graphically show the market equilibrium price and quantity you found in part a). Please label this point "A". c) Suppose that the local government imposes a $4 per-unit sales tax on consumers. Calculate the new equilibrium price and quantity that characterizes this good under this new scenario. d) Graphically show the new market equilibrium on the graph you drew in part b). Please label this point "B".arrow_forwardPlease assistarrow_forward

- I need some help Consider the equations and graphs for the demand and supply functions given below. Then answer the following questions. P=5Q^2+72Q P=-Q^2-3Q+20.23 State the domain for these curves for the analysis to be valid. (Answer to 2 decimal places)arrow_forwardYou are a financial analyst with a specialization in the motion pictureIndustry. You have been hired to analyze the prices of movie theater tickets. The following two events are occurring simultaneously in the Ghana:A new national chain opens new multi-screen movie theaters in most cities in Ghana.Movie theaters cut the price of popcorn and soft drinks in half.Draw a demand-and-supply graph showing equilibrium in the market for movie tickets hefore the above two events took place. Label the axes and curves. Label the initial equilibrium — before events (i) and (ii) - as P,and Q, on your graph.b.Now show on your graph how event (i) affects the demand or supply curves for tone teres, Brelly explain which of the demand or supply variables caused the eftect you are showing on your graph.Now slow on your graph how event (il) affects the demand or supply curves for ovis Lesets. Brielly explain which of the demand or supply variables caused the effe you are showing on your graph.Based on your…arrow_forward= D(x) = 23 Espacio en Blanco 1: Espacio en Blanco 2: Espacio en Blanco 3: P = 1 X 20 and the price-supply equation = S(x) P = Given the price-demand equation (A) Find the equilibrium price. Answer: The equilibrium price is $ (use 2 decimal places) (B) The total gain to producers who are willing to supply units at a lower price is $ (C) The total savings to consumers who are willing to pay a higher price for the product is $ = 8+ 1 8000 (round to 2 decimal places) (use 2 decimal places)arrow_forward

- QUESTION 25 Assume that there is a rise in common cold and cough in the winter months. On the other hand there is a low production of over the counter cold/cough medications How this combined situation will affect the price and quantity of such medications. Note: Make sure to explain all the steps of your analysisarrow_forwardNonearrow_forwardEstimate the equilibrium price. $ per pan. Round to the nearest dollar. Use the graph attached below to help answer the question i appreciate it thanks!!!!arrow_forward

- Your analysis of data indicates that the demand curve for product x is estimated to be linear and given by equation Qd = 150-3p and the supply curve for product x appears to be linear as well and is estimated Qs=P-10. Graphically draw these two curves labeling all relevant points such as intercepts for each line inn the horizonal and vertical axes. Now, given the demand is Qd=150-3P and supply is Qs=P-10 the next assignment is to compute the equillirbium price and quantity in the market for product X, indicate on a graph. changes in consumer demographics cause the demand curve to change Qd=90-3p. If the supply curve remains the same Qs = P - 10 graphically draw these two curves labeling all the relevant points in the horizontal and vertical axes. Now, given the demand is Qd = 90-3P and supply is Qs = P-10, the next task is to compute the new equilibrium price and quantity in the market for product x. Indicate on a graph.arrow_forwardKk135.arrow_forwardqs=-5+3p qd=9-2p2 Draw the market diagram for this product with price shown on the vertical axis. Find the economically meaningful solution for the equilibrium price and quantity.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education