ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

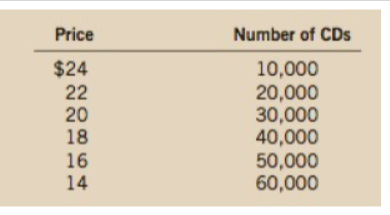

Johnny Rockabilly has just finished recording his latest CD. His record company’s

marketing department determines that the demand for the CD is as follows:

The company can produce the CD with no fixed cost and a variable cost of $5 per CD.

a. Find total revenue for quantity equal to 10,000,20,000, and so on. What is the

marginal revenue for each 10,000 increase in the quantity sold?

b. What quantity of CDs would maximize profit? What would the

the profit be?

c. If you were Johnny's agent, what recording fee would you advise johnny to demand

from the record company? Why?

Transcribed Image Text:Price

Number of CDs

$24

22

20

18

10,000

20,000

30,000

40,000

50,000

60,000

16

14

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the following passage from the article. According to studies cited by the American Cancer Society, the most surefire way to get people to quit, especially youths, is to raise prices. A 10 percent increase, for example, is followed by a 6.5 percent reduction in the number of cigarette-smoking youths and a 2 percent reduction of the habit in adults. According to the article: demand for cigarettes is elastic for both youths and adults demand for cigarettes is less elastic among youths than adults. demand for cigarettes is more elastic among youths than adults. demand for cigarettes is inelastic for both youths and adultsarrow_forwardWhich of the following is most likely to have a low price elasticity of demand? A good that is very expensive. A good with no close substitutes. A good that most people consider a luxury. All are equally likely to have a low price elasticity of demand.arrow_forwardOnly type answer and give answer fastarrow_forward

- Two drivers—Kenji and Lucia—each drive up to a gas station. Before looking at the price, each places an order. Kenji says, “I'd like 10 gallons of gas.” Lucia says, “I'd like $10 worth of gas.” Why does Lucia's demand has an unit elasticity instead of an elasticity equal to infinity?arrow_forwardMelanie really enjoys using her old-school charcoal grill to cook steaks, but she has found that due to environmental regulations, charcoal prices have gone up 50%. What is her price elasticity of demand for the rest of this month going to be compared to what it will be in the spring? Please explain why.arrow_forwardDINKS are households with "double income, no kids", and such households are invading your neighbourhood. You decide to take advantage of this influx by starting a gourmet take-away food store. Assume that these DINKS in your neighbourhood are your only potential customers. You know that the price elasticity of demand for your food from DINKS is 0.5, and their income elasticity of demand is 1.5. From the standpoint of the quantity that you sell, explain which of the following changes would concern you most. First, the number of DINKS in your neighbourhood falls by 10 percent. Second, the average income of DINKS falls by 5 percent.arrow_forward

- 10. Comics The demand curve for original Iguanawoman comics is given by (400 – p)² (0arrow_forwardImagine you've started a new pizza restaurant. It costs you about $6 to produce a pizza. Last week you sold 500 pizzas for $12 each. This week you raised your price and sold 375 pizzas for $14 each. What price should you be charging? (round to the nearest penny) Using Inverse elasticity pricingarrow_forwardCalculate the Elasticity Coefficient for the following scenario. Patty bakes pies, she sells them for $10 each and sells about 55 pies per week. But the price of her ingredients increased so she' s contemplating a price increase. She will raise the price to $12 and she estimates her demand will fall to 50 pies per week. Calculate the elasticity coefficient for Patty's Pies. Are Patty's Pies elastic or inelastic? Should she raise her prices? Or keep them the same? You should be able to show your work.arrow_forward

- Is the demand for a particular brand of car, like a Chevrolet, likely to be more or less price-elastic than the demand for all cars? It's likely to be more/less price-elastic because of the availability of substitues/complementsarrow_forwardJose owns a donut business in Los Angeles, and he wants to increase his total revenue. He knows that, when donuts are $1, he sells 200 an hour, and when he lowers the price to $0.75, he sells 280 an hour. A) Using the midpoint method, compute the price elasticity of demand for Jose’s donuts. Please show the formula used for understanding. B) Based on (A) is demand for Jose’s donuts elastic or inelastic? How do you know? Explain C) Should he raise or lower the price to generate more revenue.arrow_forwardTwo drivers-Kevin and Maria-each drive up to a gas station. Before looking at the price, each places an order. Kevin says, "I'd like 10 gallons of gas." Maria says, "I'd like $10 worth of gas." Who's statement is elastic?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education