ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

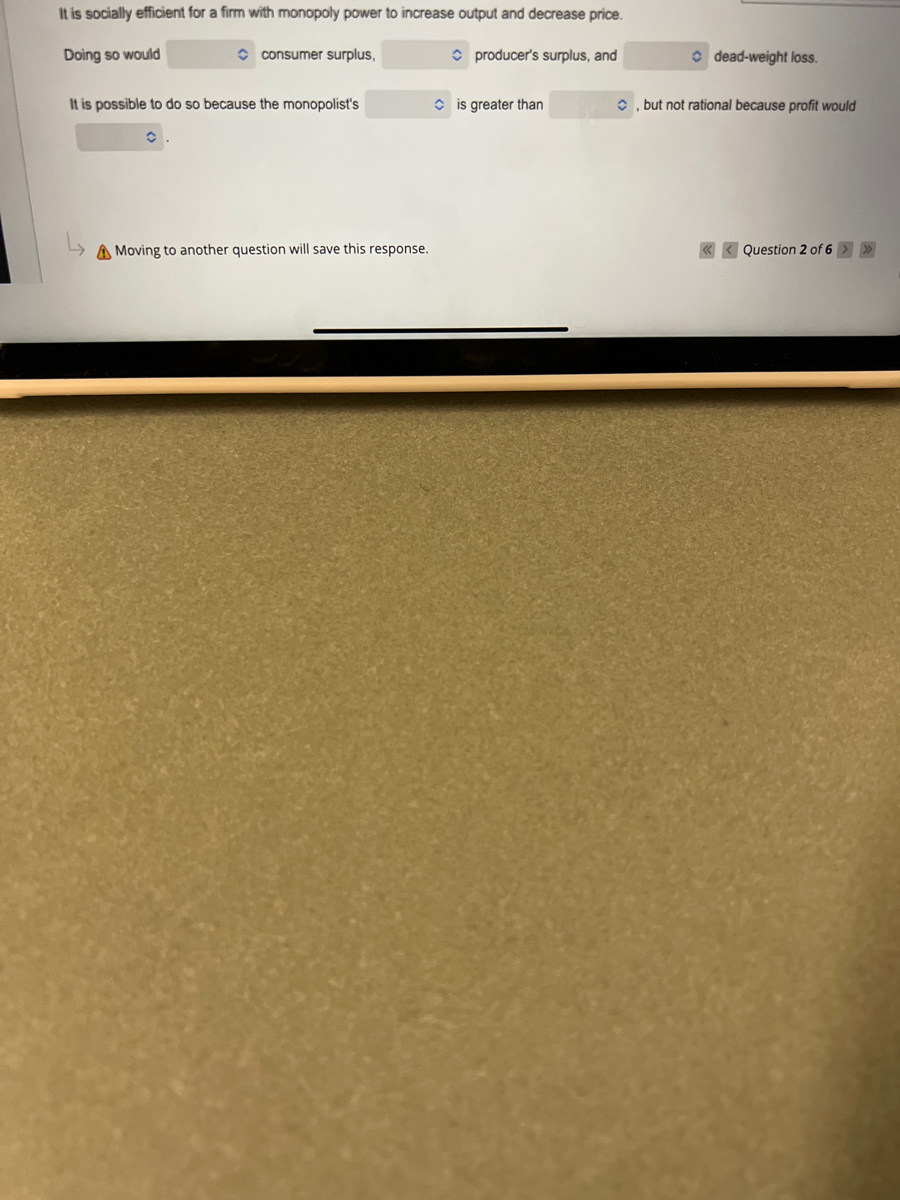

Transcribed Image Text:It is socially efficient for a firm with monopoly power to increase output and decrease price.

Doing so would

O consumer surplus,

O producer's surplus, and

O dead-weight loss.

It is possible to do so because the monopolist's

O is greater than

O, but not rational because profit would

A Moving to another question will save this response.

« < Question 2 of 6> »

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A natural monopoly exists when O producing a large output has significantly lower marginal cost than producing a small output. the good produced by a monopoly is classified as a natural product. exploitative business tactics are used to force other companies out of the market illegally. O the monopoly-level of market power develops naturally due to the company's high product quality.arrow_forwardHow is a legal monopoly different from a natural monopoly? In a legal monopoly, barriers to entry are created by the government. O In a legal monopoly, the monopolist has purchased the necessary certificate from the local government that allows the formation of a monopoly. A legal monopoly applies to government-run institutions, whereas a natural monopoly applies to all other resources O In a legal monopoly, the Federal Trade Commission has paid a firm to be the only producer of a product in a given area. JAN 12 MENU MacBook Air tv N Aarrow_forwardenter roctor "se urce n When negative externalities are present in a market 3 O private costs will be greater than social costs. O social costs will be greater than private costs. O only government regulation will solve the problem. O the market will not be able to reach any equilibrium. Question 3 In a monopolistically competitive industry, firms set price O equal to marginal cost since each firm is a price taker. O below marginal cost since each firm is a price taker. O above marginal cost since each firm is a price setter. O always a fraction of marginal cost since each firm is a price setter. C $ O 4 % BABAA 5 M Oll 6 & O 7 8 O 9 2 pts ✓ 0arrow_forward

- ASAP Suppose the market for kiwis has a demand curve of the form: Qd = 200-2Pd And that the costs of the monopoly producer of kiwis are determined by Total Cost (Q) = Variable Cost (Q) + Fixed Cost. C (Q) = Q² + 100. That is, its marginal cost will be: MgC (Qs) = 2Qs = Ps A. If the Government regulates this monopoly so that it does not generate welfare losses, how much should the maximum price to impose be? B. If the Government decides to grant a subsidy to reach the amount of the social optimum, would it stop having a loss of welfare? C. Bonus How much the subsidy should be for each unit so that the amount is reached in the social optimum.arrow_forwardABO 0 E O 75% Q Multiple Choice O Refer to the graph for a monopolist in short-run equilibrium. The monopolist will charge a price equal to the distance: OA O О ос MC g AVC MR ATC not labeled on the grapharrow_forwardMany schemes for price discrimination involvesome cost. For example, discount coupons take upthe time and resources of both the buyer and theseller. This question considers the implications ofcostly price discrimination. To keep things simple,let’s assume that our monopolist’s production costsare simply proportional to output so that averagetotal cost and marginal cost are constant and equalto each other.a. Draw the cost, demand, and marginal-revenuecurves for the monopolist. Show the pricethe monopolist would charge without pricediscrimination.b. In your diagram, mark the area equal to themonopolist’s profit and call it X. Mark thearea equal to consumer surplus and call it Y.Mark the area equal to the deadweight loss andcall it Z.c. Now suppose that the monopolist can perfectlyprice discriminate. What is the monopolist’sprofit? (Give your answer in terms of X, Y,and Z.)d. What is the change in the monopolist’s profit fromprice discrimination? What is the change in totalsurplus from…arrow_forward

- Question 9 Because a monopolist has market power, which of the following is NOT a characteristic of a monopolist? O It faces a horizontal demand curve O It faces a downward-sloping demand curve O When it produces an extra unit of output, it must lower its price for on all units sold O Its marginal revenue curve is below its demand curvearrow_forwardAssuming that the price is greater than the average variable cost, a monopolist maximizes profits at the output for which (picture a graph): O price is equal to marginal revenue in the downward part of the marginal cost curve O marginal cost is equal to marginal revenue in the upward sloping part of the marginal cost curve O average variable cost and average total cost are in the downward part of their curves and price is equal to marginal cost O average total cost is at the lowest pointarrow_forwardPlease helparrow_forward

- A single-price monopolist is currently producing at an output level where marginal revenue is $14, marginal cost is $16, AVC=$13, and ATC= $15. It is assumed that the monopolist, as usual, chooses its price on the demand curve. To maximize profit or minimize losses in the short run, this monopolist should O A. decrease the price and increase the level of output. O B. increase the price and the level of output. O C. leave the market. O D. decrease the price and the level of output. O E. increase the price and decrease the level of output.arrow_forwardThe quantity sold by a monopolist using first degree price discrimination is higher than the quantity sold by a monopolist who cannot price discriminate. O True O Falsearrow_forwardA monopolist faces the following demand curve: Price $10 $9 $8 $7 $6 $5 $4 $3 Quantity 5 Select one: O a. 31 units O b. 7 units O c. 16 units O d. 23 units 10 16 23 31 45 52 60 The monopolist has total fixed costs of $40 and a constant marginal cost of $5. What is the profit-maximizing level of output?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education