ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

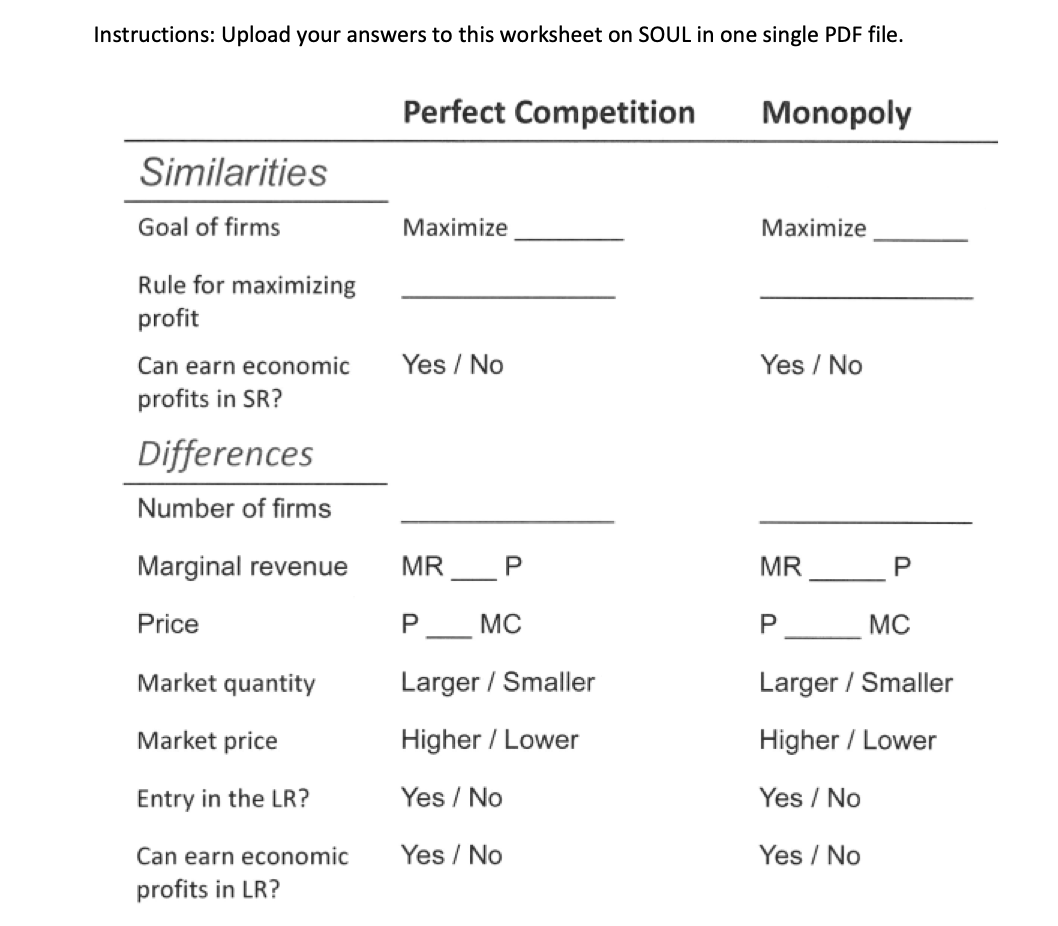

Transcribed Image Text:Instructions: Upload your answers to this worksheet on SOUL in one single PDF file.

Perfect Competition

Monopoly

Similarities

Goal of firms

Maximize

Maximize

Rule for maximizing

profit

Can earn economic

Yes / No

Yes / No

profits in SR?

Differences

Number of firms

Marginal revenue

MR__P

MR

P

Price

MC

MC

-

Market quantity

Larger / Smaller

Larger / Smaller

Market price

Higher / Lower

Higher / Lower

Entry in the LR?

Yes / No

Yes / No

Yes / No

Yes / No

Can earn economic

profits in LR?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The size of a firm is more important than market share in determining market power for an industry or product. A. True B. Falsearrow_forwardTable 8.1 Q 0 1 2 3456 3 4 6 7 8 9 10 MC $30 20 30 40 50 60 70 80 90 100 ATC $230 125.00 93.33 80.00 74.00 71.67 71.43 72.50 74.44 77.00 AVC Produce an output of 5 and earn a negative economic profit Shutdown and produce nothing Produce an output of 5 and earn a positive economic profit Produce an output of 6 and earn a positive economic profit -11 $130 75.00 60.00 55.00 54.00 55.00 57.14 60.00 63.33 67.00 Refer to table 8.1. If the competitive market price for kale is $51, what will the firm do in the short-run?arrow_forwardUsing the table for a firm (NOTE: You should use the rule of profit maximization), Price (S) Q (Demand) TR 26 1 22 2 18 3 14 10 6 4 5 6 TC 26 34 44 56 70 86 MR ΝΑ MC ΝΑ 15. Complete the table. 16. Using the table, draw the demand curve, MR curve, and MC curve in one diagram. 17. Determine the output and price of the profit-maximizing firm. (NOTE: you should explicitly use MR, MC for profit-max condition.) 18. Why can the firm not charge higher than the price you choose in #17? 19. Determine the profit of the proft-maximizing firm. 20. Determine the profit of the proft-maximizing firm in the long run.arrow_forward

- Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 10 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 15 firms. Finally, use the green points (triangle symbol) to plot the short-run industry supply curve when there are 20 firms. PRICE (Dollars per pound) 100 90 80 70 80 50 40 30 20 10 0 0 125 250 375 500 825 750 875 1000 1125 1250 QUANTITY (Thousands of pounds) Demand Because you know that competitive firms earn Supply (10 firms) True Supply (15 firms) If there were 10 firms in this market, the short-run equilibrium price of rhodium would be $ would . Therefore, in the long run, firms would False Supply (20 firms) per pound. From the graph, you can see that this means there will be ? per pound. At that price,…arrow_forwardplease answer in text form and in proper format answer with must explanation , calculation for each part and steps clearlyarrow_forwardQuestion 17 Compared to perfect competition, in a monopoly market structure price is and quantity is higher, lower higher, higher lower, higher lower, lower O Oarrow_forward

- Questioned uploaded in the attached jpg file.arrow_forwardList and explain three reasons for strong barriers to entry that make it difficult for new firms to enter the market where existing firms are earning economic profits.arrow_forward20 Fill in the blank with the correct answer by typing in the box. The most significant barrier to entry for coffee house firms that want to compete with Starbucks isarrow_forward

- How can I describe the equilibrium situation of the firm operating in the perfectly competitive market and the firm operating in the monopoly market by drawing graphics, and at the same time, how can I explain the cost, revenue and demand structures with graphics? b210801021@subu.edu.tr You can send a reply to this address. If it can be in Turkish, I would be happy, but if it is not, it is not a problem.arrow_forward4arrow_forwardSuppose a perfectly competitive industry can produce a product with total cost TC = 30 and the market demand for the product is given by Q = 120- Suppose that the same market can be served by a monopolist operates with the same cost and demand functions. How does the consumer surplus change due to monopoly relative to perfect competition? O It falls by 3600 It does not change OIt falls by 6000 It falls by 4800arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education