ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

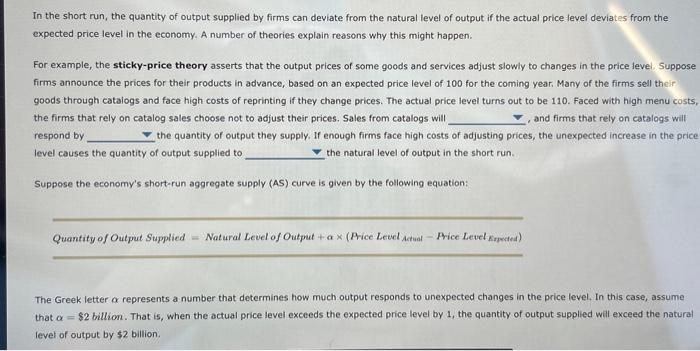

Transcribed Image Text:In the short run, the quantity of output supplied by firms can deviate from the natural level of output if the actual price level deviates from the

expected price level in the economy. A number of theories explain reasons why this might happen.

For example, the sticky-price theory asserts that the output prices of some goods and services adjust slowly to changes in the price level. Suppose

firms announce the prices for their products in advance, based on an expected price level of 100 for the coming year. Many of the firms sell their

goods through catalogs and face high costs of reprinting if they change prices. The actual price level turns out to be 110. Faced with high menu costs,

the firms that rely on catalog sales choose not to adjust their prices. Sales from catalogs will

and firms that rely on catalogs will

respond by

the quantity of output they supply. If enough firms face high costs of adjusting prices, the unexpected increase in the price

level causes the quantity of output supplied to

the natural level of output in the short run..

Suppose the economy's short-run aggregate supply (AS) curve is given by the following equation:

Quantity of Output Supplied Natural Level of Output + ax (Price Level Actual-Price Level Expected)

The Greek letter a represents a number that determines how much output responds to unexpected changes in the price level. In this case, assume

that a $2 billion. That is, when the actual price level exceeds the expected price level by 1, the quantity of output supplied will exceed the natural

level of output by $2 billion.

Transcribed Image Text:Suppose the natural level of output is $60 billion of real GDP and that people expect a price level of 110.

On the following graph, use the purple line (diamond symbol) to plot this economy's long-run aggregate supply (LRAS) curve. Then use the orange

line segments (square symbol) to plot the economy's short-run aggregate supply (AS) curve at each of the following price levels: 100, 105, 110, 115,

and 120.

PRICE LEVEL

125

120

115

110

105

100

95

90

85

80

A

75

0 10

20

40 50 60 70

30

OUTPUT (Billions of dollars)

60 90

100

AS

LRAS

?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- December, 2006, was a difficult month for Colorado’s beef industry. Multiple heavy snow storms caused thousands of beef cattle to be stranded in nose-high snow drifts. They could not get food or water for themselves. In spite of valiant attempts by the National Guard to drop hay, many died. Beef market prices in the spring were predicted to rise. The series of unfortunate events continued: after the spring thaw, Colorado cattlemen experienced a couple of cases of mad-cow disease. Beef market prices fell (contrary to the earlier prediction). Diagram in (a) the initial impact of the bad winter on the price and quantity. Then, on the same grid, incorporate the impact on price and quantity of the mad-cow cases. Be sure that your final diagram indicates a market price decrease. Using economic terminology, write a statement in (b) explaining the results of your graphical analysis in (a). a) GRAPHICAL ANALYSIS b) WRITTENarrow_forwardGiven a linear supply function of the form QXs = 3,000 + 3PX - 2Pr - Pw, and assuming Pr = $1,000, Pw = $100, and PX=50, the PS is: (use commas: 30,000 instead of 30000)arrow_forwardTwo software companies sell competing products. These products are substitutes so that the number of units that either company sells is a decreasing function of its own price and an increasing function of the other product’s price. Let P1 and X1 be the price and quantity sold of product 1, and P2 and X2 the price and quantity sold of product 2. We have that and . Each company has incurred a fixed cost for designing their software and writing programmes, but the cost of selling to an extra user is zero. As the firms compete in prices, each company will choose a price that maximises its profits. Explain why the price that maximises each company’s profits is the same as the price that maximises its total revenue. Write an expression for the total revenue of each company as a function of it its price and the other company’s price. Company’s 1 best response function BR1(P2) is the price of product 1 that maximises its profits given the price of product 2 is P2. Similarly,…arrow_forward

- Consider an economy consisting of some firms with flexible prices and some with rigid prices. Let pf denote the price set by a representative flexible-price firm and p' the price set by a representative rigid-price firm. Flexible-price firms set their prices after m is known; rigid-price firms set their prices before m is known. Thus flexible-price firms set pf = p = (1-)p+ om, and rigid-price firms set p' = Ep = (1-6)Ep + Em, where E denotes the expectation of a variable as of when the rigid-price firms set their prices. Assume that fraction q of firms have rigid prices, so that p =qp² + (1 − q)pf. (a) Find pf in terms of p',m, and the parameters of the model (o and q). (b) Find p' in terms of Em and the parameters of the model. (c) (i) Do anticipated changes in m (that is, changes that are expected as of when rigid-price firms set their prices) affect y? Why or why not? (ii) Do unanticipated changes in m affect y? Why or why not?arrow_forwardThe market for coffee is characterized by Qdc=210-Pc and Qsc=2Pc-0.5Pt where QC is the quantity of coffee in hundreds of pounds, PC is the price per hundred pounds of coffee, and PT is the price per hundred pounds of tea. The market for tea is characterized by Qdt=210-Pt and Qst= 2Pt-0.5Pc, where QT is the quantity of tea in hundreds of pounds. Suppose a new medical study touts the benefits of drinking coffee, leading to an increase of 30 pounds of coffee at every price. The new equilibrium price of tea is ____. The new equilibrium price of coffee is _____.arrow_forwardWhat variables cause the simple sticky price AS curve to shift? What variables cause the partial sticky price AS curve to shift?arrow_forward

- For demand function Qd = a - bP and supply function Qs = dP - c , using Cramer’s rule determine equilibrium price and equilibriumarrow_forwardQuestion For each sentence below describing changes in the tangerine market, discuss whether the statement is true, false, or uncertain. Justify your answer. (You will find it helpful to draw a graph for each case.) • If consumers’ income increases, and the wage of the laborers in the industry falls, the quantity purchased in the market will rise and the price will fall. • If orange prices decrease, and a new agro-chemical increases the productivity of tangerine trees, the quantity will fall and the price will rise. • If the price of canning machinery (a complement) increases, and the growing season is unusually cold, both quantity and price will fall.arrow_forwardConsider a market in which the demand curve is given by P= 1000-50, and the supply curve is given by P=7.20. Suppose there is a positive supply shock and the supply curve shifts to the right, so that quantity supplied increases by 100 at each price. What is the new equilibrium price? Give your answer to 2 decimal places. 590.2arrow_forward

- From the graph, it is clear that the demand for gasoline is relatively (unit elastic, elastic, inelastic) and the supply for gasoline is relatively (unit elastic, elastic, inelastic). This is an example of a (positive or negative) supply shock and, referencing the graph below, is best represented by the shift (from curve 1 to curve 2 or from curve 2 to curve 1). If there's a price-gouging law in effect preventing gas stations from raising prices, then there will be an excess (supply, or demand) of _____ million gallons of gas. Suppose the government wants to alleviate the market imbalance. The best policy solution is to impose (import tariffs, production subsidies, import quotas, or purchasing limits) and the (cost or revenue) would be $______ million.arrow_forwardConsider a market in which the demand curve is given by P= 1000-50, and the supply curve is given by P = 7.20. Suppose there is a positive supply shock and the supply curve shifts to the right, so that quantity supplied increases by 100 at each price. What is the new equilibrium price? Give your answer to 2 decimal places.arrow_forwardQ6. Give one example when there is an increase in the supply curve.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education