ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

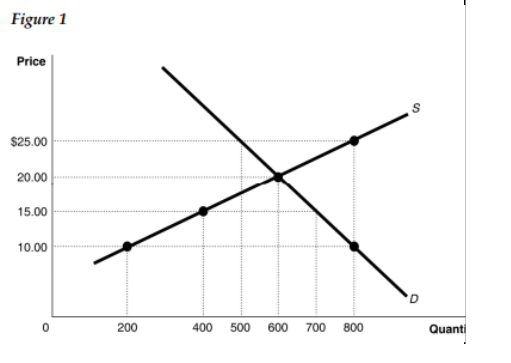

Question

If the current market

Group of answer choices:

a price decrease, decreasing the supply and increasing the demand

a price increase, increasing the supply and decreasing the demand.

a price decrease, decreasing the quantity demanded and increasing the quantity supplied.

a price decrease, decreasing quantity supplied and increasing quantity demanded.

a price increase, increasing the quantity supplied and decreasing the quantity demanded.

Transcribed Image Text:Figure 1

Price

$25.00

20.00

15.00

10.00

200

400

500

600

700

800

Quanti

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- which of the following does not directly influence the demand for a good? the size of the population consumer preferences the cost of producing the good average consumer incomearrow_forwardWhich of the following will produce a price increase for Good X? For each case, plot a chart with supply and demand curves to show your idea. Demand rises while Supply falls. Demand falls while Supply is constant. Supply falls while Demand is constant. Demand falls faster than Supply falls. Supply rises while Demand falls. Demand rises faster than Supply rises.arrow_forwardAn increase in supply and a decrease in demand occur in a market. What happens to the equilibrium price and quantity?arrow_forward

- If the quantity supplied in a market exceeds the quantity demanded, a shortage will exist. True or False True Falsearrow_forwardIf supply is upward sloping, a decrease in demand with no change in supply will lead to a(n) _____ in equilibrium quantity and a(n) _____ in equilibrium pricearrow_forwardIf both supply and demand decrease, the equilibrium price A) does not change. B) cannot be predicted. C) rises. D) falls.arrow_forward

- A decrease in both the equilibrium price and the equilibrium quantity of pasta is best explained by an: increase in the expected future price of pasta. increase in the cost of producing pasta. decrease in income if pasta is an inferior good. decrease in the price of rice if pasta and rice are substitutes.arrow_forwardWhen supply and demand meet at the equilibrium point, then prices in the market willarrow_forwardThe nature of demand indicates that as the price of a good increases: suppliers wish to sell less of it. more of it is produced. more of it is desired. buyers desire to purchase less of it.arrow_forward

- What happens to the market for "rescue" pets after a local food brings many more dogs & cats into local shelters? Circle one answer for each: Demand, Supply, Price, and Quantity. Demand: Up, Down, Unchanged Supply: Up, Down, Unchanged Price: Up, Down, Unchanged Quantity: Up, Down, Unchangedarrow_forwardOne of the following factors that can best explain why there has been a decline in the equilibrium price and the equilibrium quantity of corn:A) an increase in the demand for corn.B) a decrease in the demand for corn.C) a decrease in the supply of corn.D) an increase in the supply of corn.arrow_forwardIf equilibrium price increases while equilibrium quantity decreases, then we know that: market demand has decreased. market demand has increased. market supply has decreased. market supply has increased.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education