Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

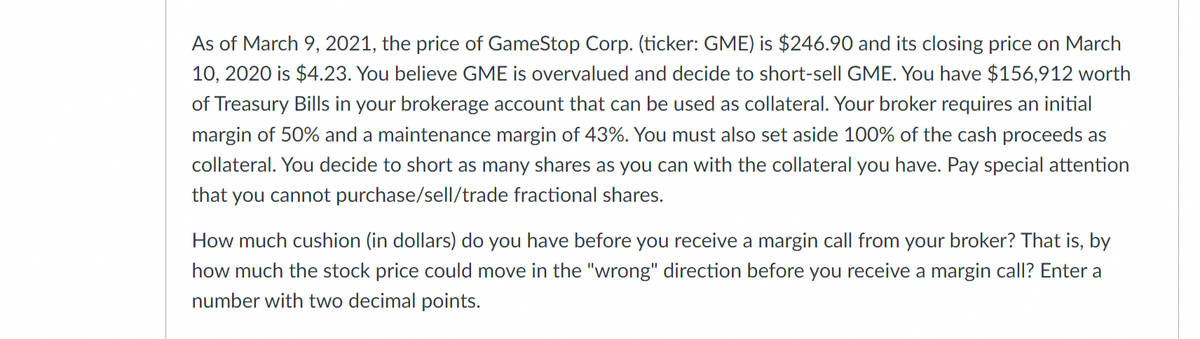

Transcribed Image Text:As of March 9, 2021, the price of GameStop Corp. (ticker: GME) is $246.90 and its closing price on March

10, 2020 is $4.23. You believe GME is overvalued and decide to short-sell GME. You have $156,912 worth

of Treasury Bills in your brokerage account that can be used as collateral. Your broker requires an initial

margin of 50% and a maintenance margin of 43%. You must also set aside 100% of the cash proceeds as

collateral. You decide to short as many shares as you can with the collateral you have. Pay special attention

that you cannot purchase/sell/trade fractional shares.

How much cushion (in dollars) do you have before you receive a margin call from your broker? That is, by

how much the stock price could move in the "wrong" direction before you receive a margin call? Enter a

number with two decimal points.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Which of the following is the best reason why the price-earnings method is often used by investors to estimate the fair price of a stock? a) Because the earning multiples are easily found in online financial databases. b) Earnings per share is a known amount that is related to the payment of future dividends. c) Because the price-earnings method gives the same answer as the constant growth method and is easier to compute. d) The price-earnings method has been shown to provide the most accurate price estimate.arrow_forwardp) demonstrate an understanding of the constructions of a synthetic call by identifying the breakeven stock price, the maximum profit, and the maximum loss. q) Define the following terms: combination, spread, buying the spread (debit spread), selling the spread (credit spread), money (vertical or strike) spread, calendar (horizontal or time) spread r) demonstrate an understanding of bull spreads by defining bull spreads, discussing the circumstances under which investors would use a bull spread strategy. s) demonstrate an understanding of bear spreads by defining bear spreads, discussing the circumstances under which investors would use a bear spread strategy. t) demonstrate an understanding of collars by defining collars, discussing the circumstances under which investors would use a collar strategy.arrow_forwardQuestion 1. Let St be the current price of a stock that pays no dividends. a)Let rbid be the interest rate at which one can invest/lend money, and roff be theinterest rate at which one can borrow money, rbid≤roff. Both rates are continuously compounded. Using arbitrage arguments, find upper and lower bounds for the forwardprice of the stock for a forward contract with maturity T > t. b)How does your answer change if the stock itself has bid price St,bid and offer price St,off?arrow_forward

- What factors affect current market interest rate? Why does the slope of the yield curve provide an important clue to the direction of future short-term interest rates?Given the forward rate available to the company, discuss the factors that it should consider at the outset when deciding whether to fix the future interest rate. The word-count for this element should be 500-600 words.arrow_forwardAn arrangement with a broker to borrow stocks from them and then sell it in the market, with the hope that they earn a profit by buying the stock back again after it has fallen in price is called Select one: a. smart money. Ob. short sales. Oc. behavioral finance. Od. random walk.arrow_forwardWhich of the following statements is most correct? Why?* a. If a market is weak-form efficient, this means that prices rapidly reflect all available public information. b. If a market is weak-form efficient, this means that you can expect to beat the market by using technical analysis that relies on the charting of past prices. c. If a market is strong-form efficient, this means that all stocks should have the same expected return. d. All of the statements above are correct. c. None of the statements above is correct.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education