ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

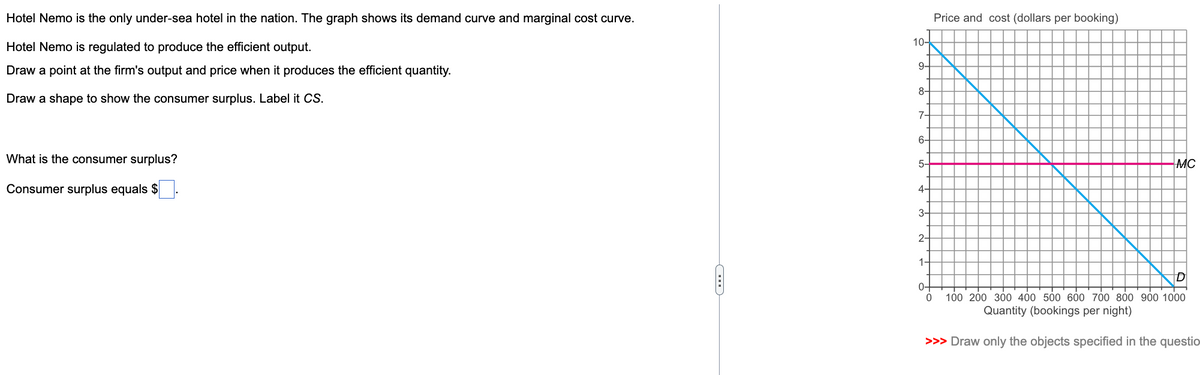

Transcribed Image Text:Hotel Nemo is the only under-sea hotel in the nation. The graph shows its demand curve and marginal cost curve.

Hotel

Nemo is regulated to produce the efficient output.

Draw a point at the firm's output and price when it produces the efficient quantity.

Draw a shape to show the consumer surplus. Label it CS.

What is the consumer surplus?

Consumer surplus equals $

(...)

10-

9-

8-

7-

6-

5-

4-

3-

2-

1-

0-

Price and cost (dollars per booking)

0

MC

100 200 300 400 500 600 700 800 900 1000

Quantity (bookings per night)

>>> Draw only the objects specified in the questio

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The following graph shows Sparkle's demand curve, marginal-revenue (MR) curve, average-total-cost (ATC) curve, marginal-cost (MC) curve, and profit-maximizing output and price. Demand ATC C MC MR Quantity of Sparkle Toothpaste Indicate which of the labeled areas represent consumer surplus derived from the purchase of Sparkle toothpaste or deadweight loss relative to the efficient level of output. A B D Consumer Surplus Deadweight Loss Suppose the government required Sparkle to produce the efficient level of output. Which of the following describes what would happen to the firm and Sparkle's customers? O Sparkle would earn negative profit, forcing it to shut down, and Sparkle's customers would gain no consumer surplus. O Sparkle would earn zero profit, and its customers would be just as well off as before. O Sparkle would earn positive profit and increase production, boosting consumer surplus. Price, Cost, Revenuearrow_forwardPrice ($ per Can) $2.00 1.75 1.50 1.25 1.00 0.75 0.50 0.25 $ per can Quantity Demanded (per Day) b. monopolized market? per can 30 40 50 60 70 80 90 100 Total Revenue A If the marginal cost of supplying a soda is constant and equal to $0.50, what price will students end up paying in a. perfectly competitive market? $ 75.00 Marginal Revenue ($ per Can)arrow_forwardWhat is meant by consumer surplus and producer surplus? Using a diagram show that there is a deadweight loss to society from monopoly in terms of total surplus.arrow_forward

- VALUES GIVEN ON GRAPH. PLEASE HELP ASAP, THANK YOU!arrow_forwardSketch a graph of the theater's demand functions, marginal revenue, and marginal cost to find the following: 1. The firm's profit-maximizing price = $____? 2. Ticket output = ____? 3. Economic profit = $ ____? 4. Compute consumer surplus, producer surplus, and deadweight lossarrow_forwardQuestión 10 óf 18 Holiday Beach is a world-renowned beach operated by Holiday Town. The beach is remotely located and the only parking area for the beach is controlled by the town government. The graphs depict the marginal revenue (MR) and demand (D) for daily parking passes for tourists and residents. Tourists Residents Price per day Price per day $20 $207 18 18 16 14 14 12 12 D 10 - 10 8 8 6 6 MR 4 4 MR 2 1 2 3 4 6. 7 8 9. 10 1 2 3 4 7 8 9 10 Quantity of passes Quantity of passes Suppose Holiday Town issues registration plates to its residents to make it easy to determine which cars belong to residents and which cars belong to tourists. Assume the marginal cost of providing a daily parking pass is a constant $4 and Holiday Town wishes to price discriminate. What price will town residents be charged for a daily pass? $ %24arrow_forward

- Question: Explain the concept of consumer surplus and producer surplus. How are these measures related to market efficiency?Don't use chatgpt please provide valuable answer otherwise be ready for disupvotearrow_forwardSupposed that solar panels are produced in a perfectly competitive industry, which of the following statement on solar panels is correct? a. Consumers do not consider all panels to be identical b. There is no barrier to entry for new firms wanting to produce the identical quantity of solar panels c. Assuming there are no sources of market failure, the equilibrium point maximises the sum of consumer plus producer surplus. d. The equilibrium maximises producer’s surplus.arrow_forwardPlease help me to answer part B of Question 1.arrow_forward

- 1 Fill in the blank with the correct answer by typing in the box. Innovation can end a monopoly and bring - prices.arrow_forwardThe diagram below represents a monopoly market with one privately owned power generator. P 90 75 60 45 30 15 10 20 30 40 ATC 50 b1. Show the expected social losses from having a monopoly. Draw in any extra lines you need to show your solution. b2. If a law is passed requiring marginal cost pricing in the above market, what problem would there be for this privately owned power generator. Support your answer with a diagram.arrow_forwardHomework (Ch 06) Back to Assignment Attempts Do No Harm / 1 3. Effects of rent control Rent controls force landlords to price apartments below the equilibrium price level. An immediate effect is a shortage (excess demand) of apartments, because the quantity of apartments demanded is greater than the quantity supplied at the regulated price. When cities prevent landlords from charging market rents, which of the following are common long-run outcomes? Check all that apply. O Landlords earn lower profits from renting housing units, but the rent charged has no effect on either the quantity or quality of rental units. O The future supply of rental housing units increases. O Black markets develop. O The quality of rental housing units falls.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education