FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

thumb_up100%

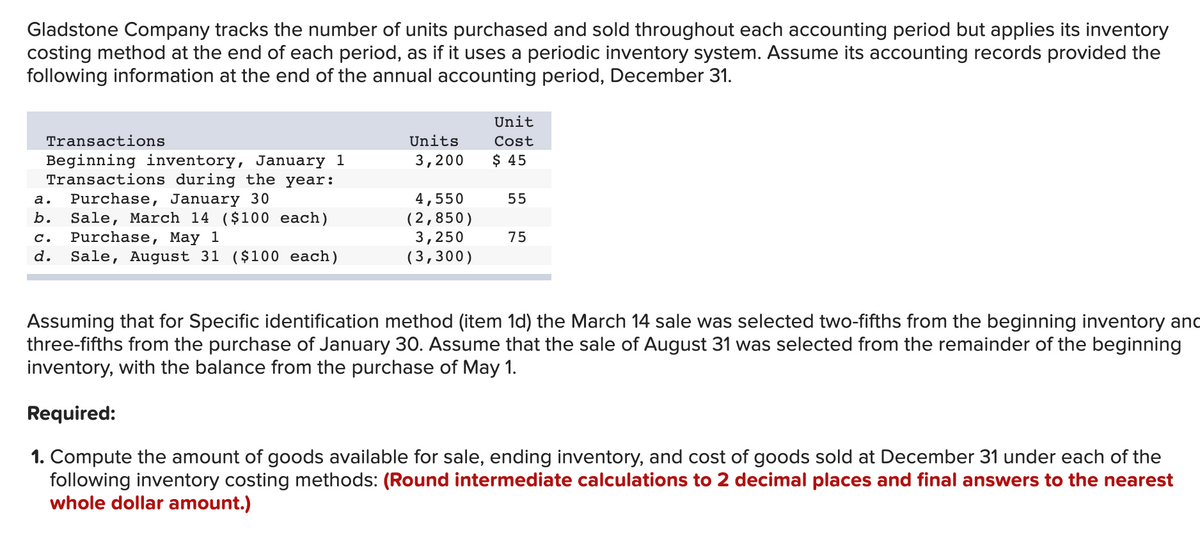

Gladstone Company tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the end of each period as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31.

| Transactions | Units | Unit Cost | |||||

| Beginning inventory, January 1 | 3,200 | $ | 45 | ||||

| Transactions during the year: | |||||||

| a. | Purchase, January 30 | 4,550 | 55 | ||||

| b. | Sale, March 14 ($100 each) | (2,850 | ) | ||||

| c. | Purchase, May 1 | 3,250 | 75 | ||||

| d. | Sale, August 31 ($100 each) | (3,300 | ) | ||||

Assuming that for the Specific identification method (item 1d) the March 14 sale was selected two-fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the sale of August 31 was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1.

Transcribed Image Text:Gladstone Company tracks the number of units purchased and sold throughout each accounting period but applies its inventory

costing method at the end of each period, as if it uses a periodic inventory system. Assume its accounting records provided the

following information at the end of the annual accounting period, December 31.

Unit

Transactions

Units

Cost

$ 45

Beginning inventory, January 1

Transactions during the year:

Purchase, January 30

Sale, March 14 ($100 each)

Purchase, May 1

Sale, August 31 ($100 each)

3,200

4,550

(2,850)

3,250

(3,300)

а.

55

b.

с.

75

d.

Assuming that for Specific identification method (item 1d) the March 14 sale was selected two-fifths from the beginning inventory and

three-fifths from the purchase of January 30. Assume that the sale of August 31 was selected from the remainder of the beginning

inventory, with the balance from the purchase of May 1.

Required:

1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at December 31 under each of the

following inventory costing methods: (Round intermediate calculations to 2 decimal places and final answers to the nearest

whole dollar amount.)

Transcribed Image Text:Assuming that for Specific identification method (item 1d) the March 14 sale was selected two-fifths from the beginning inventory and

three-fifths from the purchase of January 30. Assume that the sale of August 31 was selected from the remainder of the beginning

inventory, with the balance from the purchase of May 1.

Required:

1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at December 31 under each of the

following inventory costing methods: (Round intermediate calculations to 2 decimal places and final answers to the nearest

whole dollar amount.)

Amount of Goods

Cost of Goods

Ending Inventory

Available for Sale

Sold

638,000 $

638,000 $

Last-in, first-out

$

234,750 $

403,250

a.

b. Weighted average cost

$

281,300 $

356,700

c. First-in, first-out

$

638,000

d. Specific identification

$

638,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A company reports the following beginning inventory and two purchases for the month of January. On January 26, the company sells 310 units. Ending inventory at January 31 totals 130 units. Units Unit Cost Beginning inventory on January 1 280 $ 2.60 Purchase on January 9 60 2.80 Purchase on January 25 100 2.94 Required:Assume the perpetual inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on LIFO.arrow_forwardNittany Company uses a periodic inventory system. At the end of the annual accounting period, December 31 of the current year, the accounting records provided the following information for product 1: Ending inventory Cost of goods sold Inventory, December 31, prior year For the current year: Purchase, March 21 Purchase, August 1 Inventory, December 31, current year Required: Compute ending inventory and cost of goods sold for the current year under FIFO, LIFO, and average cost inventory costing methods. Note: Round "Average cost per unit" to 2 decimal places and final answers to nearest whole dollar amount. FIFO Units 1,870 LIFO 5,030 2,980 4,090 Unit Cost $4 Average Costarrow_forwardSandhill Company uses the gross profit method to estimate inventory for monthly reporting purposes. Presented below is information for the month of May. Inventory, May 1 Purchases (gross) Freight in Sales revenue Sales returns Purchase discounts (a) $156,000 576,100 (b) 29,300 998,400 72,100 11.900 Your answer is correct Compute the estimated Inventory at May 31, assuming that the gross profit is 25% of sales The estimated inventory at May 31 $ eTextbook and Media The estimated inventory at May 31 54775 $ Assistance Used Compute the estimated inventory at May 31, assuming that the gross profit is 25% of cost Round percentage of sales to 2 decimal places, eg 78.74% and final answer to 0 decimal places, eg 6,225) Attempts: 1 of 12 usedarrow_forward

- Please make a weighted average- perpetual chartarrow_forwardA company reports the following beginning inventory and two purchases for the month of January. On January 26, the company sells 280 units. Ending inventory at January 31 totals 130 units. Beginning inventory on January 1 Purchase on January 9 Purchase on January 25 Perpetual FIFO: Required: Assume the perpetual inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on the FIFO method. Date January 1 January 9 January 25 January 26 Totals Goods purchased # of units Cost per unit Units Unit Cost 250 60 100 # of units sold $2.30 2.50 2.64 Cost of Goods Sold Cost per Cost of Goods unit Sold Inventory Balance Cost per unit # of units Inventory Balancearrow_forwardAircard Corporation tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the end of each period as if it uses a periodic inventory system. The following are the transactions for the month of July. Units Unit Cost July 1 Beginning Inventory 2,000 $ 35 July 5 Sold 1,000 July 13 Purchased 6,000 39 July 17 Sold 3,000 July 25 Purchased 8,000 41 July 27 Sold 5,000 Calculate the cost of goods available for sale, ending inventory, and cost of goods sold if Aircard uses (a) FIFO, (b) LIFO, or (c) weighted average cost. (Round "Cost per Unit" to 2 decimal places.)\arrow_forward

- answer in text form please (without image)arrow_forwardNittany Company uses a periodic inventory system. At the end of the annual accounting period, December 31 of the current year, the accounting records provided the following information for product 1: Unit Units Cost Inventory, December 31, prior year. 1,860 $ 3 For the current year: Purchase, March 21 5,180 5 Purchase, August 1 Inventory, December 31, current year 2,980 4,030 6 Required: Compute ending inventory and cost of goods sold for the current year under FIFO, LIFO, and average cost inventory costing methods. Note: Round "Average cost per unit" to 2 decimal places and final answers to nearest whole dollar amount. Ending inventory Cost of goods sold FIFO LIFO Average Costarrow_forwardDineshbhaiarrow_forward

- Please helparrow_forwardKirtland Corporation uses a periodic inventory system. At the end of the annual accounting period, December 31, the accounting records for the most popular item in inventory showed the following: Assessment Tool iFrame Transactions Beginning inventory, January 1 Transactions during the year: a. Purchase, January 30 b. Purchase, May 1 c. Sale ($5 each) d. Sale ($5 each) Units 400 Unit Cost $ 3.00 300 460 3.40 4.00 (160) (700) Required: a. Compute the amount of goods available for sale. b. & c. Compute the amount of ending inventory and cost of goods sold at December 31, under Average cost, First-in, first-out, Last-in, first-out and Specific identification inventory costing methods. For Specific identification, assume that the first sale was selected two- fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1. Complete this…arrow_forwardNittany Company uses a periodic inventory system. At the end of the annual accounting period, December 31 of the current year, the accounting records provided the following information for product 1: Inventory, December 31, prior year For the current year: Purchase, March 21 Purchase, August 1 Inventory, December 31, current year Required: Unit Units Cost 1,850 $ 3 5,040 2,930 56 4,140 Compute ending inventory and cost of goods sold for the current year under FIFO, LIFO, and average cost inventory costing methods. Note: Round "Average cost per unit" to 2 decimal places and final answers to nearest whole dollar amount. Ending inventory Cost of goods sold FIFO LIFO Average Costarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education