FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

Additionally, provide an analysis of the transaction. Use a chart like the one from question to advise the affect that the transaction will have on Assets, Liabilities or Owner's equity. Please also include the account that is affected for the category (Cash, Unearned Revenue etc)

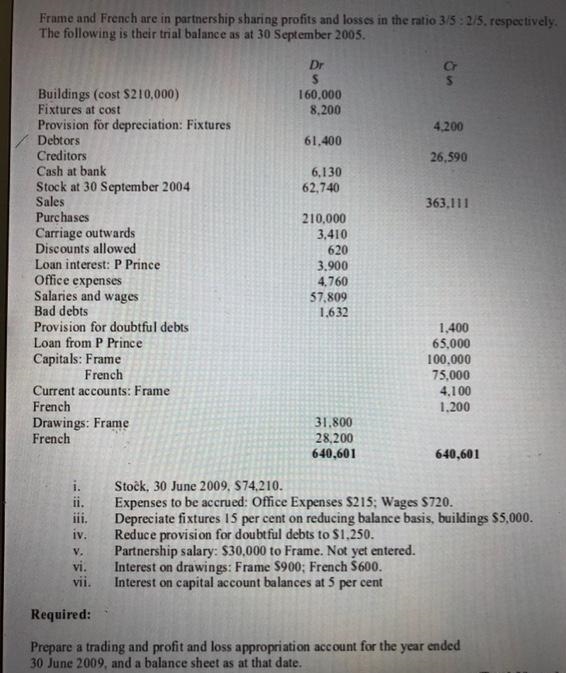

Transcribed Image Text:Frame and French are in partnership sharing profits and losses in the ratio 3/5:2/5. respectively.

The following is their trial balance as at 30 September 2005.

Dr

Buildings (cost $210,000)

Fixtures at cost

Provision för depreciation: Fixtures

Debtors

Creditors

Cash at bank

160,000

8,200

4,200

61,400

26,590

6,130

62,740

Stock at 30 September 2004

Sales

Purchases

Carriage outwards

Discounts allowed

Loan interest: P Prince

Office expenses

Salaries and wages

Bad debts

Provision for doubtful debts

Loan from P Prince

363,111

210,000

3,410

620

3.900

4,760

57,809

1.632

1,400

65,000

100,000

75,000

4,100

Capitals: Frame

French

Current accounts: Frame

French

1,200

Drawings: Frame

French

31.800

28,200

640,601

640,601

Stočk, 30 June 2009, $74,210.

Expenses to be accrued: Office Expenses $215; Wages $720.

Depreciate fixtures

Reduce provision for doubtful debts to $1.250.

Partnership salary: $30,000 to Frame. Not yet entered.

Interest on drawings: Frame $900; French $600.

Interest on capital account balances at 5 per cent

ii.

iii.

per cent on reducing balance basis, buildings $5,000.

iv.

V.

Vi.

vii.

Required:

Prepare a trading and profit and loss appropriation account for the year ended

30 June 2009, and a balance sheet as at that date.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Which accounts commonly requires both debit and credit entries?arrow_forwardWhich of the following items is considered an original source document? Select one: a. accounts receivable b. company expense account c. purchase order d. general ledgerarrow_forwardSelect the item that best completes each of the descriptions below. a. A collection of accounts and account balances is referred to as a(n) b. A(n). such as a bank statement, is objective evidence of transactions and their amounts. c. Increases and decreases in a specific asset, liability, equity, revenue, or expense are recorded in a(n) d. A(n) _ асcount has a complete record of every transactions recorded. journal e. A list of all ledger accounts and identification numbers, not including account balances, is called a(n). of accounts.arrow_forward

- How does the data flow from the transaction (e.g. MRI scan) to financial statements? Use the following key terms in your response: transaction, journal entry, general ledger, financial statement.arrow_forwardDefine the followings? a. Real Account. b. Temporary Account.arrow_forwardHow do I identify a transaction and whether it is debited or credited?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education