MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

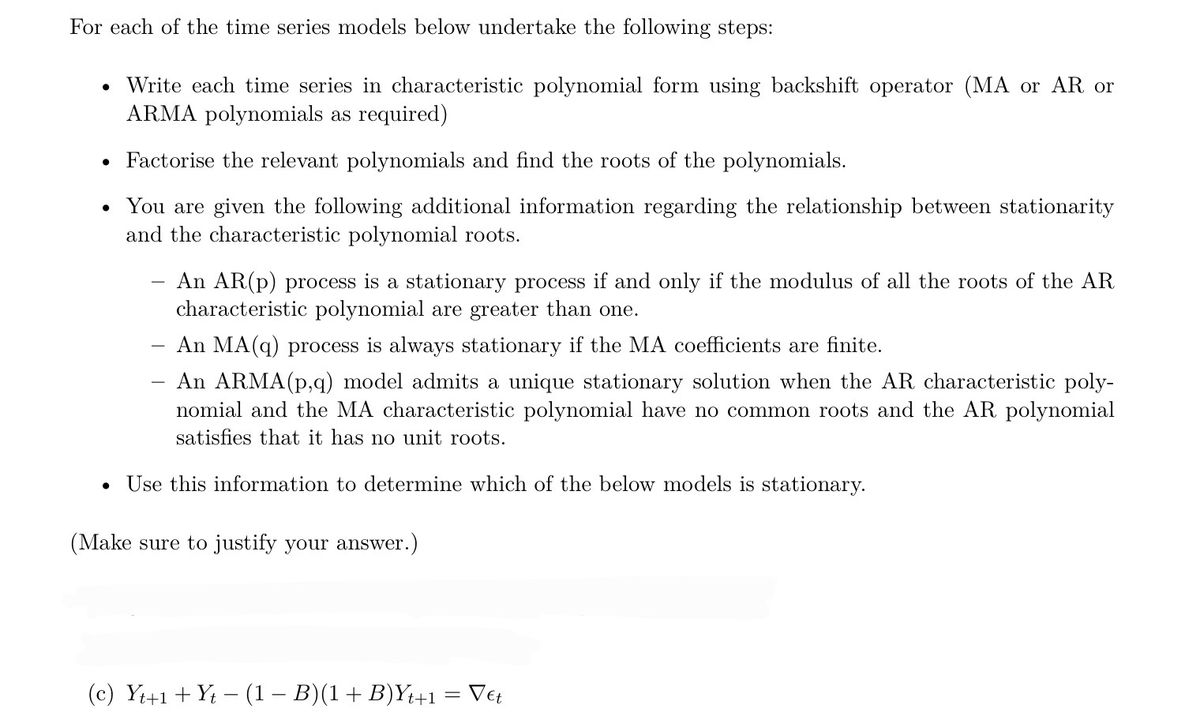

Transcribed Image Text:For each of the time series models below undertake the following steps:

Write each time series in characteristic polynomial form using backshift operator (MA or AR or

ARMA polynomials as required)

• Factorise the relevant polynomials and find the roots of the polynomials.

• You are given the following additional information regarding the relationship between stationarity

and the characteristic polynomial roots.

●

An AR(p) process is a stationary process if and only if the modulus of all the roots of the AR

characteristic polynomial are greater than one.

- An MA(q) process is always stationary if the MA coefficients are finite.

An ARMA (p,q) model admits a unique stationary solution when the AR characteristic poly-

nomial and the MA characteristic polynomial have no common roots and the AR polynomial

satisfies that it has no unit roots.

• Use this information to determine which of the below models is stationary.

(Make sure to justify your answer.)

(c) Yt+1+ Yt - (1 − B)(1 + B)Yt+1 = Vet

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- For each of the time series models below undertake the following steps: Write each time series in characteristic polynomial form using backshift operator (MA or AR or ARMA polynomials as required) Factorise the relevant polynomials and find the roots of the polynomials. • You are given the following additional information regarding the relationship between stationarity and the characteristic polynomial roots. ● ● An AR(p) process is a stationary process if and only if the modulus of all the roots of the AR characteristic polynomial are greater than one. An MA(q) process is always stationary if the MA coefficients are finite. An ARMA (p,q) model admits a unique stationary solution when the AR characteristic poly- nomial and the MA characteristic polynomial have no common roots and the AR polynomial satisfies that it has no unit roots. ● Use this information to determine which of the below models is stationary. (Make sure to justify your answer.) (e) Let {Y} be a stationary process with…arrow_forwardFor each of the time series models below undertake the following steps: • Write each time series in characteristic polynomial form using backshift operator (MA or AR or ARMA polynomials as required) • Factorise the relevant polynomials and find the roots of the polynomials. • You are given the following additional information regarding the relationship between stationarity and the characteristic polynomial roots. An AR(p) process is a stationary process if and only if the modulus of all the roots of the AR characteristic polynomial are greater than one. An MA(q) process is always stationary if the MA coefficients are finite. An ARMA (p,q) model admits a unique stationary solution when the AR characteristic poly- nomial and the MA characteristic polynomial have no common roots and the AR polynomial satisfies that it has no unit roots. Use this information to determine which of the below models is stationary. (Make sure to justify your answer.) (a) VY + ²3 (Yt + 5Y₁-1) = € - €t-1 − −2+ 3…arrow_forwardAn engineer designs a circuit, seen below. In this system, if the first component fails, the functionality moves immediately to the second component and so on. The system only fails when the fifth component fails. Each component has a lifetime that is exponentially distributed with λ = 0.01 and components fail independently of one another. Define A, to be the length of time component i lasts. Let Y = the time at which the new system fails. Given 2 لنا 5 A-Exponential (0.01) Y=A1+A2+A3+A4+A5 1. Find the probability that this new system will last fewer than 50 hours.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman