ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

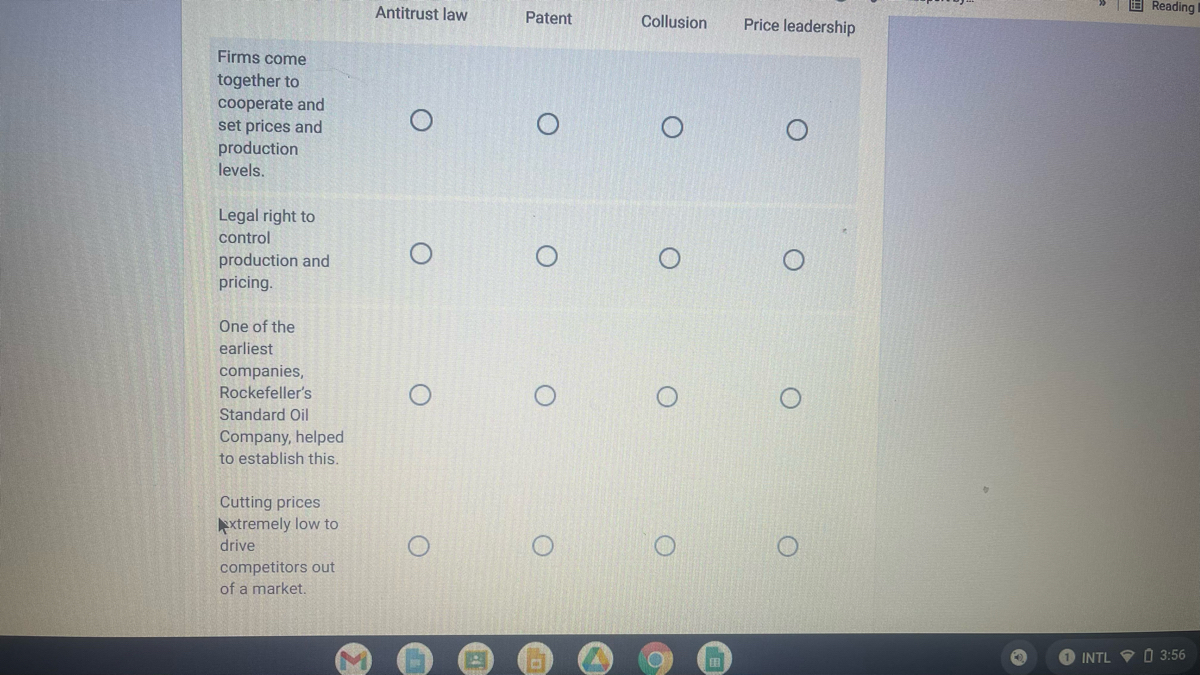

Transcribed Image Text:Firms come

together to

cooperate and

set prices and

production

levels.

Legal right to

control

production and

pricing.

One of the

earliest

companies,

Rockefeller's

Standard Oil

Company, helped

to establish this.

Cutting prices

Extremely low to

drive

competitors out

of a market.

M

Antitrust law

O

O

Patent

O

O

0

Collusion

O

O

●

Price leadership

O

O

CO

Reading

INTL 3:56

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- O Macmillan Learning (Figure: Determining Monopolist Profit) Based on the graph, the profit-maximizing price is at point Price and Cost h Of. O g. d. C MR Output MC ATCarrow_forwardAnswer the question by referring to the table below. The table shows the demand curve facing a monopolistwho produces at constant marginal cost of 6. In short-run equilibrium, the monopolist will produceQuantity Price10 1020 930 840 750 660 5a) 20 unitsb) 30 unitsc) 40 unitsd) 50 unitsarrow_forwardPlease no written by hand solutions 1. Assume the cost function for a monopolist is given by TC(q) = 30Q; the inverse demand function for the firms' output is p = 120 - Q, where Q is the total output. a. Find the profit-maximizing combination of price and quantity b. Estimate consumer surplus, producer surplus and the deadweight loss associated with this monopolist C. If this industry became perfectly competitive, explain and estimate the consumer surplus, producer surplus and deadweight loss of the industry d. Graph your answers for a, b, and c 2. Now assume that the monopolist above splits into two. Each of two firms has the cost function TC(q) = 30q. a. What are the firms' outputs in a Nash equilibrium of Cournot's model? b. Estimate the economic profits for each firm c. If firm 1 is the leader and firm 2 the follower, find the equilibrium outputs for the Stackelberg solution.arrow_forward

- Question 30 Demand: P=120-Q Marginal Revenue: MR=120-2Q Total Cost: TC=Q² Marginal Cost: MC=2Q For this monopolist, the profit-maximizing price is and the profit-maximizing quantity is 90, 30 30, 90 40, 80 None of these answers O O Oarrow_forwardWhat are conditions conducive to a natural monopoly? Select one: a. Extensive economies of scale. b. Rapid diseconomies of scale c. Patents Od. Small market sizearrow_forwardExplain the incorrect options also. Please. Tyarrow_forward

- An unregulated monopolist would not use which of the following: marginal cost pricing O the profit-maximizing rule O price discrimination economies of scalearrow_forwardIn a monopoly situation, the more inelastic is the demand, Seleccione una: a. higher is going to be the equilibrium price b. lower is going to be the equilibrium price c. lower is going to be the unbalance between demand and supply d. higher is going to be the unbalance between demand and supplyarrow_forwardanswer quicklyarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education