Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

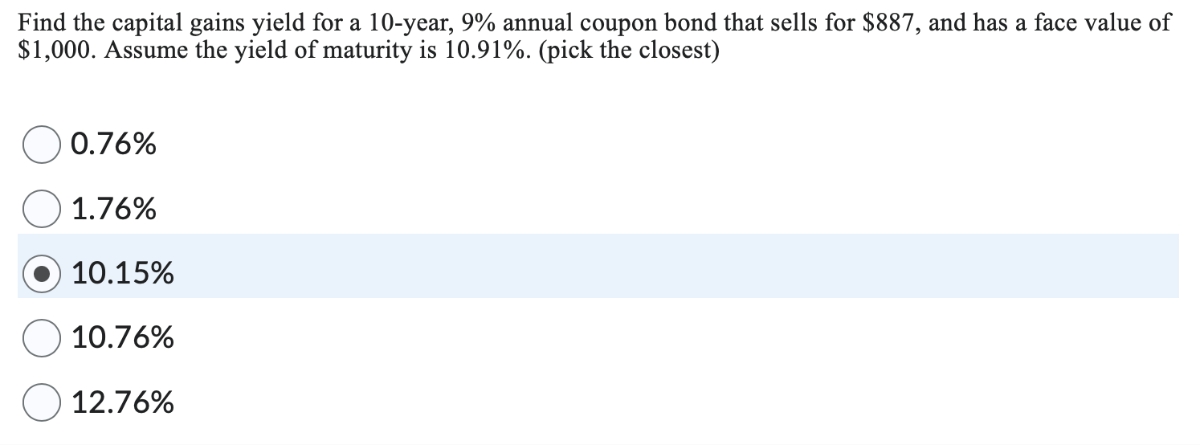

Transcribed Image Text:Find the capital gains yield for a 10-year, 9% annual coupon bond that sells for $887, and has a face value of

$1,000. Assume the yield of maturity is 10.91%. (pick the closest)

0.76%

1.76%

10.15%

10.76%

12.76%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- What is the coupon rate for a bond with a face value of $1,000, 24 years to maturity, a current price of $993, and a yield to maturity (YTM) of 9.09%?arrow_forwardWhat is the coupon rate of a ten-year, $10,000 bond with semiannual coupons and a price of $9,558.57, if it has a yield to maturity of 6.6%? OA. 7.188% OB. 5.99% OC. 4.792% OD. 8.386%arrow_forwardGive typing answer with explanation and conclusionarrow_forward

- A 12% bond of Alpha Company with 15 year to maturity is selling in the market for $955, it has a $1,000 par value and pays interest annually. a. Calculate the both bond's yield to maturity (YTM).b. If your required rate of return is 12% would you buy this bond or not.b. Describe the relationship between the coupon rate and yield to maturity and market value of a bond.arrow_forwardA firm raises capital by selling $10,000 worth of debt with flotation costs equal to 2% of its par value. If the debt matures in 10 years and has an annual coupon interest rate of 11%, what is the bond's YTM? Question content area bottom Part 1 The bond's YTM is enter your response here%. (Round to two decimal places.)arrow_forwardSuppose you are given the following information about the default-free, coupon-paying yield curve: Maturity (years) Coupon rate (annual payment) YTM 1 0.00% 2.587% a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4? Note: Assume annual compounding. 2 11.00% 4.008% a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. The yield to maturity of a two-year, zero-coupon bond is %. (Round to two decimal places.) b. What is the zero-coupon yield curve for years 1 through 4? The yield to maturity for the three-year and four-year zero-coupon bond is found in the same manner as the two-year zero-coupon bond. The yield to maturity on the three-year, zero-coupon bond is %. (Round to two decimal places.) The yield to maturity on the four-year, zero-coupon bond is %. (Round to two decimal places.) Which graph best depicts the yield curve of the zero-coupon bonds? (Select the…arrow_forward

- What must be the price of a $5,000 bond with a 6.5% coupon rate, semiannual coupons, and five years to maturity if it has a yield to maturity of 9% APR? ..... O A. $6,308 B. $3,604 C. $5,407 D. $4,505arrow_forwardSunnyfax Publishing pays out all its earnings and has a share price of $37.00. In order to expand, Sunnyfax Publishing decides to cut its dividend from $3.00 to $2.00 per share and reinvest the retained funds. Once the funds are reinvested, they are expected to grow at a rate of 14%. If the reinvestment does not affect Sunnyfax's equity cost of capital, what is the expected share price as a consequence of this decision? O$45.87 $40.14 $68.81 $57.34arrow_forwardYou are given the following expected 1-year rates for each of the next 5 years and the cash flows for Bond A (assume that it pays an annual coupon). Based on this information, determine the yield-to- maturity for Bond A. Year 1 23 3 4 5 7.17% 6.80% O 7.54% O6.43 % O 7.91% Expected 1-Year Rate 9.00% 8.00% 7.00% 6.00% 5.00% Bond A Cash Flow $ 100.00 $ 100.00 $ 100.00 $ 100.00 $1,100.00 4arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education