ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

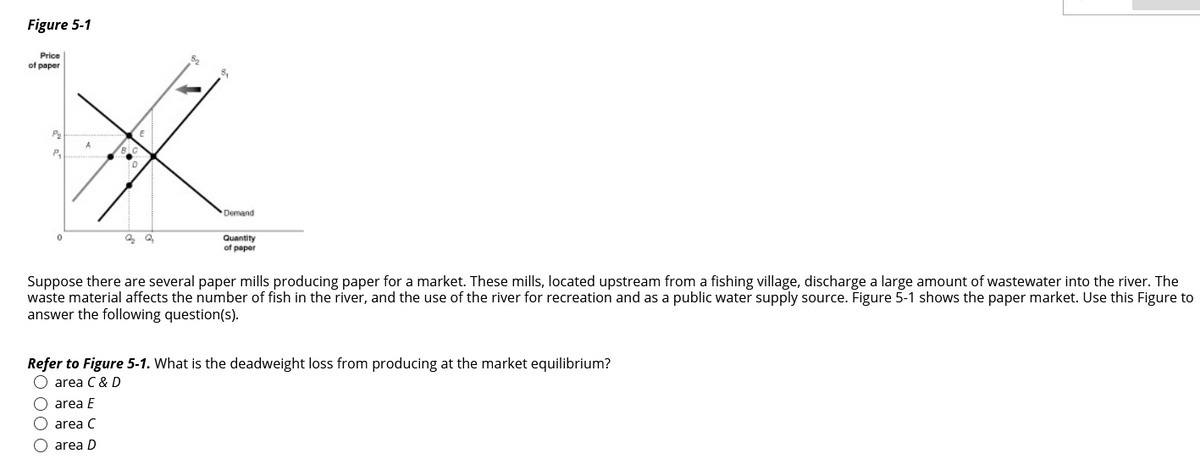

Transcribed Image Text:Figure 5-1

Price

of paper

P2

P,

Demand

Quantity

of paper

Suppose there are several paper mills producing paper for a market. These mills, located upstream from a fishing village, discharge a large amount of wastewater into the river. The

waste material affects the number of fish in the river, and the use of the river for recreation and as a public water supply source. Figure 5-1 shows the paper market. Use this Figure to

answer the following question(s).

Refer to Figure 5-1. What is the deadweight loss from producing at the market equilibrium?

area C & D

area E

area C

O area D

Expert Solution

arrow_forward

Step 1

DEADWEIGHT LOSS:

A deadweight loss could be a price to society as a full that's generated by an economically inefficient allocation of resources among the market. Deadweight loss may also be noted as an “excess burden.”

A deadweight loss arises sometimes once supply and demand, the two most basic forces driving the economy–are unbalanced. That is, they do not attain equilibrium. The result is that the allocative potency isn't as high because it could be. It doesn't reach its optimum level. With lower levels of trade, resource allocation across the economy is probably going to reduce economically.

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Include correctly labeled diagrams, if useful or required, in explaining your answers. A correctly labeled diagram must have all axes and curves clearly labeled and must show directional changes. If the question prompts you to “Calculate,” you must show how you arrived at your final answer. Assume that sugar-based soft drinks are produced in a market shown on the graph above. Answer the following questions based on the information given in the graph. (a) To reduce the consumption of sugary soft drinks, suppose the government imposes a $2 per-unit sales tax on soft drinks. (i) Will the price of soft drinks increase by the full amount of the sales tax? Explain. (ii) Calculate the tax revenue the government can collect from the sale of soft drinks. Show your work. (iii) Will the consumer surplus increase, decrease, or stay the same after the tax? (iv) Calculate the deadweight loss created by the tax. Show your work. (b) Suppose that instead of imposing the per-unit sales tax,…arrow_forwardplease do it quick i need it as soon as possible.(3) Sketch a supply and demand model of the housing (home ownership) market. Label the equilibrium price and equilibrium quantity. Now sketch in TWO changes on the same graph: an increase in demand; a reduction in supply.arrow_forwarde Price -Q₁ Quantity Which of the following scenarios is BEST represented in the graph? A number of sellers increase B decrease in government taxes C resource costs increase D technology improvesarrow_forward

- Government-imposed taxes cause reductions in the activity that is being taxed, which has important implications for revenue collections. To understand the effect of such a tax, consider the monthly market for cigarettes, which is shown on the following graph. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. PRICE (Dollars per pack) 10 9 8 6 2 1 0 0 # Supply Demand 10 20 30 40 50 60 70 80 90 100 QUANTITY (Packs) Graph Input Tool Market for Cigarettes 31- Quantity (Packs) Demand Price (Dollars per pack) (Dollars per pack) Suppose the government imposes a $2-per-pack tax on suppliers. At this tax amount, the equilibrium quantity of cigarettes is Tax 40 6.00 2.00 Supply Price (Dollars per pack) packs, and the government collects $ ? 4.00 in tax revenue.arrow_forwardQuestion 2: Suppose you have the following information about the demand and supply of cotton in the U.S.: Price 9 15 25 35 U.S. Supply 4 12 17 U.S. Demand 40 36 30 20 10 (a) Determine the equations of the supply and demand curves. Assume that the two equations are linear. (b) Determine the market equilibrium price and quantity. (c) Now suppose that the US can import an arbitrary quantity of cotton at a price of 15 Dollars. How many units will the U.S. import?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education