ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

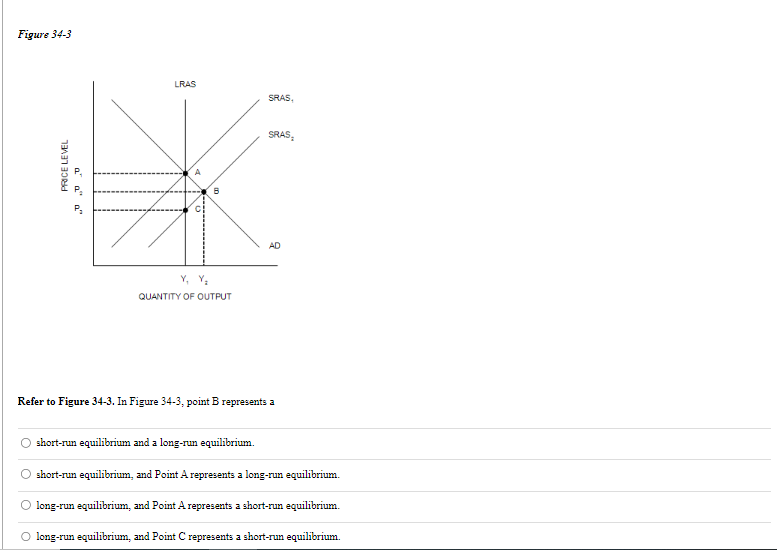

Transcribed Image Text:Figure 34-3

PRICE LEVEL

aaa"

LRAS

B

Y, Y₂

QUANTITY OF OUTPUT

SRAS.

SRAS

AD

Refer to Figure 34-3. In Figure 34-3, point B represents a

short-run equilibrium and a long-run equilibrium.

short-run equilibrium, and Point A represents a long-run equilibrium.

long-run equilibrium, and Point A represents a short-run equilibrium.

long-run equilibrium, and Point C represents a short-run equilibrium.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- K How will an increase in the number of sellers of tablets affect the market for this product? A. Demand will increase causing the equilibrium price to increase and the equilibrium quantity to increase. OB. Supply will increase causing the equilibrium price to decrease and the equilibrium quantity to increase. OC. Supply will decrease causing the equilibrium price to decrease and the equilibrium quantity to increase. O D. Supply will increase causing the equilibrium price to increase and the equilibrium quantity to decrease.arrow_forwardThe blue curve on the following graph represents the demand curve facing a firm that can set its own prices. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. Graph Input Tool Market for Goods 200 I Quantity Demanded 180 10 (Units) 160 140 Demand Price 100.00 (Dollars per unit) 120 100 80 60 Demand 40 20 6 8 10 QUANTITY (Units) 0 2 4 8 12 14 16 18 20 On the graph input tool, change the number found in the Quantity Demanded field to determine the prices that correspond to the production of 0, 4, 8, 10, 12, 16, and 20 units of output. Calculate the total revenue for each of these production levels. Then, on the following graph, use the green points (triangle symbol) to plot the results. 1000 900 Total Revenue 800 700 600 500 400 300 200 100 + 2 4 6 8 10 12 14 16 18 20 QUANTITY…arrow_forwardImagine there is a market for erasers. This market has many companies selling identical erasers. After several years, however, many of these firms combine and become a few large companies. Now this market for erasers is only served by five firms selling erasers. Because of this, you would anticipate O an increase in total erasers sold and a decrease in the price of erasers. an increase in total erasers sold and an increase in the price of erasers. O a decrease in total erasers sold and a decrease in the price of erasers. O a decrease in total erasers sold and an increase in the price of erasers.arrow_forward

- If the price of cream (an input into ice cream production) increases, then an ice cream store's curve shifts to the Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer. a supply; right supply; left demand; right demand; left Parrow_forwardThe relationship between quantity supplied and the price of output is such that O an increase in quantity will automatically lead to a reduction in price. O quantity will decrease as the number of firms increases. O an increase in price will produce an inward shift in the supply curve. O an increase in price will lead to an increase in quantity supplied.arrow_forward33arrow_forward

- Question 2arrow_forwardSupply and Demand: End of Chapter Problems 6. Suppose the market for tomatoes is in equilibrium, and events occur that simultaneously shift both the demand and supply curves to the right. If this is the only information you have, what can you say about how the equilibrium price or quantity would be affected? The equilibrium O quantity would increase, whereas the direction of the change in equilibrium price would be indeterminate. price would increase, whereas the direction of the change in equilibrium quantity would be indeterminate. O price and quantity would both decrease. price and quantity would both increase. Question Source: Chiang 4e - Economics Principles For A Changing World Publisher: Worth Publishers a 9:39 PM 64°F 10/13/2021 SParrow_forwardQuestion 25 Many consumer items eventually go out of style, and because fewer people want these items, demand for them drops. When this happens, we usually see production of these items stop. What happens to the equilibrium price and equilibrium quantity in a market like this? The equilibrium price is indeterminate and equilibrium quantity goes up. The equilibrium price is indeterminate and equilibrium quantity goes down. O The equilibrium price goes down and equilibrium quantity is indeterminate. O The equilibrium price goes up and equilibrium quantity goes up. O The equilibrium price goes up and equilibrium quantity is indeterminate.arrow_forward

- 8. Short-run and long-run effects of a shift in demand Suppose that the tempeh industry is initially operating in long-run equilibrium at a price level of $5 per pound of tempeh and quantity of 100 million pounds per year. Suppose a leading foodie video blogger raises awareness for a scholarly article that links tempeh consumption to premature hair loss and unhealthy skin. The viral video is expected to cause consumers to demand less tempeh at every price. In the short run, firms will respond by producing the same amount of tempeh and running at a loss Shift the demand curve, the supply curve, or both on the following graph to illustrate these short-run effects of the viral video. PRICE (Dollars per pound) 10 9 8 1 0 0 20 Supply 40 60 80 100 120 140 QUANTITY (Millions of pounds) In the long run, some firms will respond by D. D₂ 160 180 200 consumer demand returns to its original level Demand Supply (?) exiting the industry until and unhealthy skin. The viral video is expected to cause…arrow_forwardHomework (Ch 09) 1. The supply curve in the very short run The following graph shows the annual demand for tortilla chip consumption, which is initially in long-run equilibrium at point D. Suppose that tortilla chips are sold in a perfectly competitive market, and tastes shift away from tortilla chips so that demand shifts leftward from D₁ to D₂. Use the purple line (diamond symbol) to illustrate the supply curve in the very short run. Make sure the line passes through two of the starred points on the graph. PRICE (Dollars per bag) 10 9 0 1 2 C D A B D₂ 3 4 5 6 7 8 QUANTITY (Millions of bags per year) 9 D. 10 Short-Run Supply Curve ?arrow_forward# For a firm, the supply curve is given to be as:- 2P - 30 = Q And the demand curve is give to be as:- 15 - P = Q Calculate the equilibrium price and equilibrium Quantityarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education