FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

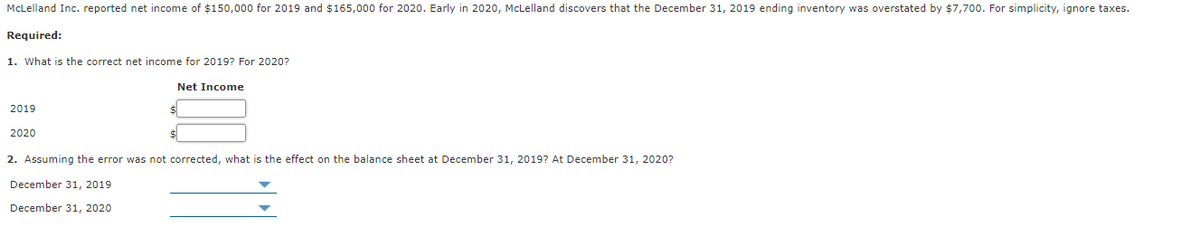

Transcribed Image Text:McLelland Inc. reported net income of $150,000 for 2019 and $165,000 for 2020. Early in 2020, McLelland discovers that the December 31, 2019 ending inventory was overstated by $7,700. For simplicity, ignore taxes.

Required:

1. What is the correct net income for 2019? For 2020?

Net Income

2019

2020

2. Assuming the error was not corrected, what is the effect on the balance sheet at December 31, 2019? At December 31, 2020?

December 31, 2019

December 31, 2020

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Dunbar sold 590 units of inventory during the month. Ending inventory assuming weighted-average cost would E decimal places and final answer to the nearest dollar amount.)arrow_forwardCrane Company had 100 units in beginning inventory at a total cost of $8,000. The company purchased 200 units at a total cost of $22,000. At the end of the year, Crane had 60 units in ending inventory. Crane Company uses a periodic inventory system. Compute the cost of the ending inventory and the cost of goods sold under FIFO, LIFO, and average-cost. (Round average-cost per unit and final answers to 0 decimal places, e.g. 1,250.) FIFO LIFO Average-cost The cost of the ending inventory $enter a dollar amount rounded to 0 decimal places $enter a dollar amount rounded to 0 decimal places $enter a dollar amount rounded to 0 decimal places The cost of goods sold $enter a dollar amount rounded to 0 decimal places $enter a dollar amount rounded to 0 decimal places $enter a dollar amount rounded to 0 decimal placesarrow_forwardNord Store’s perpetual accounting system indicated ending inventory of $20,000, cost of goodssold of $100,000, and net sales of $150,000. A year-end inventory count determined that goodscosting $15,000 were actually on hand. Calculate (a) the cost of shrinkage, (b) an adjusted costof goods sold (assuming shrinkage is charged to cost of goods sold), (c) gross profit percentagebefore shrinkage, and (d) gross profit percentage after shrinkage. Round gross profit percentagesto one decimal placearrow_forward

- Blue Corporation's April 30 inventory was destroyed by fire. January 1 inventory was $155,000, and purchases for January through April totaled $467,300. Sales revenue for the same period was $684,500. Blue's normal gross profit percentage is 25% on sales. Using the gross profit method, estimate Blue's April 30 inventory that was destroyed by fire. Estimated ending inventory destroyed in fire $arrow_forwardEnding inventory for the year ended December 31, 2017, is understated by $15,000. How will this error affect net income for 2018? Net income will be understated by $30,000. Net income will be understated by $15,000. O Net income will be overstated by $15,000. O Net income will be overstated by $30,000. O The understatement of inventory in 2017 will not affect income in 2018.arrow_forward(i)The inventory costing $ 150,000 being ordered by customers before the year end was excluded from the ending inventory balance as they are set aside for delivery after year end. The ending balance of inventory as on the statement of financial position was $ 600,000. (ii) Inventory list shows 40 boxes of rice but only 38 boxes were found in the warehouse. (iii) The inventory has a cost of $600,000 and realizable value of $540,000 as the items are outdated. The ending balance of inventory as on the statement of financial position was $ 600,000. Q) For each misstatement above, explain which of the above assertions is violated. (Each assertion can only be used once.) Also, give the relevant audit objective the auditor should focus on when detecting the misstatement if the assertion is "Valuation and Allocation "arrow_forward

- A noninterest-bearing note is issued on February 12 of a non-leap year in the amount of $14,250. It has a term of 10 months. It is sold on September 22 with a negotiated interest rate of 2%. Determine the proceeds of the sale. Add 3 days grace period. Select one: a. $14184.71 b. $12193.87 c. none d. $13189.29 Checkarrow_forwardHow many units must be in ending inventory if beginning inventory was 16,924 units, 31,777 units were started, and 34,076 units were completed and transferred out?arrow_forwardI needarrow_forward

- Martha Inc. had 20,000 units of ending inventory that were recorded at the cost of five dollars per unit using the FIFO method. The current replacement cost is $4.25 per unit which of the following amounts would be reported as ending merchandise inventory in the balance sheet, using the lower of cost or market rule. A) $85,000 B) $100,000 C) $120,000 D) $185,000 arrow_forwardSunland Company had 140 units in beginning inventory at a total cost of $11,200. The company purchased 280 units at a total cost of $30,800. At the end of the year, Sunland had 75 units in ending inventory. (a) Partially correct answer icon Your answer is partially correct. Compute the cost of the ending inventory and the cost of goods sold under FIFO, LIFO, and average-cost. (Round average-cost per unit and final answers to 0 decimal places, e.g. 1,250.) FIFO LIFO Average-cost The cost of the ending inventory $ $ $ The cost of goods sold $ $ $arrow_forwardThe Red Sun Corporation has ending inventory of $250,000, and cost of goods sold for the year just ended was $800,000. Inventory Turnover is _______.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education