Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

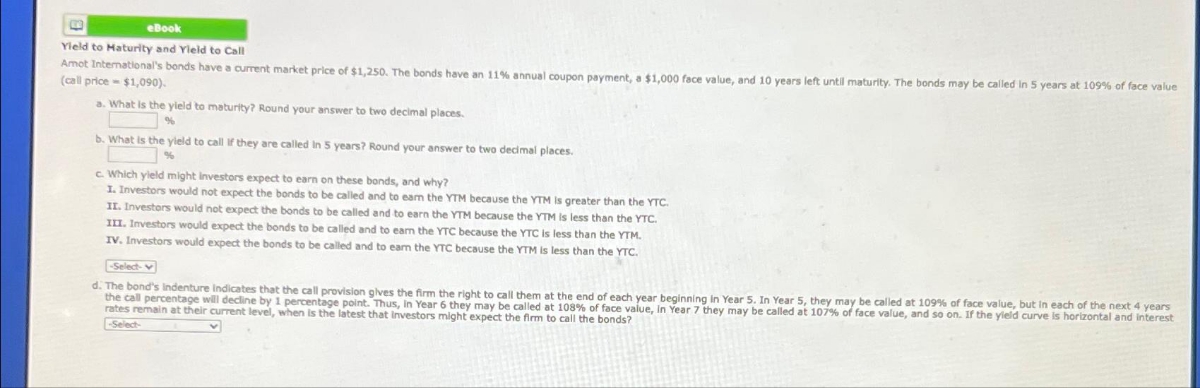

Transcribed Image Text:eBook

Yield to Maturity and Yield to Call

Amot International's bonds have a current market price of $1,250. The bonds have an 11% annual coupon payment, a $1,000 face value, and 10 years left until maturity. The bonds may be called in 5 years at 109% of face value

(call price - $1,090).

a. What is the yield to maturity? Round your answer to two decimal places.

%

b. What is the yield to call if they are called In 5 years? Round your answer to two decimal places.

c. Which yield might investors expect to earn on these bonds, and why?

I. Investors would not expect the bonds to be called and to earn the YTM because the YTM is greater than the YTC.

II. Investors would not expect the bonds to be called and to earn the YTM because the YTM is less than the YTC.

III. Investors would expect the bonds to be called and to earn the YTC because the YTC is less than the YTM.

IV. Investors would expect the bonds to be called and to earn the YTC because the YTM is less than the YTC.

-Select-

d. The bond's Indenture indicates that the call provision gives the firm the right to call them at the end of each year beginning in Year 5. In Year 5, they may be called at 109% of face value, but in each of the next 4 years

the call percentage will decline by 1 percentage point. Thus, In Year 6 they may be called at 108% of face value, In Year 7 they may be called at 107% of face value, and so on. If the yield curve is horizontal and interest

rates remain at their current level, when is the latest that investors might expect the firm to call the bonds?

-Select-

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Savitaarrow_forwardFind the value of the following two corporate bonds then discuss how the value of the bonds change when time maturity changesarrow_forwardQuestion a 3Ts Corp. issued a 21-year bond on Sept. 1, 2003. The bonds have semiannual coupon payments, an annual coupon rate of 7.5%, and a par value of $1,000. The yield to maturity (YTM) for this bond is 10%. Today is March 1, 2017. Please include formula for finding dates. Full explain this question and text typing work only We should answer our question within 2 hours takes more time then we will reduce Rating Dont ignore this line..arrow_forward

- Yield to Maturity and Current Yield You just purchased a bond that matures in 15 years. The bond has a face value of $1,000 and an 8% annual coupon. The bond has a current yield of 8.37%. What is the bond's yield to maturity? Do not round intermediate calculations. Round your answer to two decimal places.arrow_forwardYield to Maturity and Call with Semiannual Payments Thatcher Corporation's bonds will mature in 18 years. The bonds have a face value of $1,000 and an 8.5% coupon rate, paid semiannually. The price of the bonds is $950. The bonds are callable in 5 years at a call price of $1,050. What is their yield to maturity? What is their yield to call? Do not round intermediate calculations. Round your answers to two decimal places.arrow_forwardSuppose a Google.com bond will pay $4,000 ten years from now. If the going interest rate on safe 9-year bonds is 4.20%, how much is the bond worth today? Group of answer choices $3,066.38 $2,613.77 $2,887.56 $2,762.17 $2,660.65arrow_forward

- Part B: At t=0, you purchase a four-year, 5 percent coupon bond (paid annually) that is priced to yield 6 percent continuously compounded (YTM = 6% continuously compounded). The face value of the bond is $1,000. The bond issuer is the U.S. government (no liquidity risk). You are also given that your holding period (investment horizon) equals to 3.70 years (t=T=3.70 years). Suppose that the market interest rate changes to 5.50 percent continuously compounded during the first year of your purchase (within year 1), and it remains at that level for the remaining life of the bond. Assume that, the reinvestment rate for the first coupon payment is the new interest rate that is, 5.50 percent continuously compounded. In addition, you will reinvest the coupor payments in a zero-coupon bond. What is your continuously compounded Holding Period Return of your investment at the end of your investment horizon (t=3.70) years? (Round-off to four decimal places, to obtain as accurate answer as possible…arrow_forwardView Policies Current Attempt in Progress Carla Vista, Inc., has four-year bonds outstanding that pay a coupon rate of 7.0 percent and make coupon payments semiannually. If these bonds are currently selling at $921.69. What is the yield to maturity that an investor can expect to earn on these bonds? Assume face value is $1,000. (Round answer to 1 decimal place, e.g. 15.2%) Yield to maturity % What is the effective annual yield? (Round answer to 1 decimal place, eg. 15.2%) Effective annual yield. %arrow_forwardeBook The real risk-free rate, r*, is 1.55%. Inflation is expected to average 2.25% a year for the next 4 years, after which time inflation is expected to average 3.3% a year. Assume that there is no maturity risk premium. An 11-year corporate bond has a yield of 11.45%, which includes a liquidity premium of 0.85%. What is its default risk premium? Do not round intermediate calculations. Round your answer to two decimal places. %arrow_forward

- eBook One-year Treasury securities yield 3.8%. The market anticipates that 1 year from now, 1-year Treasury securities will yield 6.15%. If the pure expectations theory is correct, what is the yield today for 2-year Treasury securities? Calculate the yield using a geometric average. Do not round intermediate calculations. Round your answer to two decimal places. %arrow_forwardYield to Maturity and Current Yield You just purchased a bond that matures in 15 years. The bond has a face value of $1,000 and an 8% annual coupon. The bond has a current yield of 8.37%. What is the bond's yield to maturity? Do not round intermediate calculations. Round your answer to two decimal places. % Please advise on this questionarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education