Practical Management Science

6th Edition

ISBN: 9781337406659

Author: WINSTON, Wayne L.

Publisher: Cengage,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Discuss at least three alternatives for improving the overall profitability of the daycare facility. How would you implement those three alternatives and the potential results?

Transcribed Image Text:Truman State University

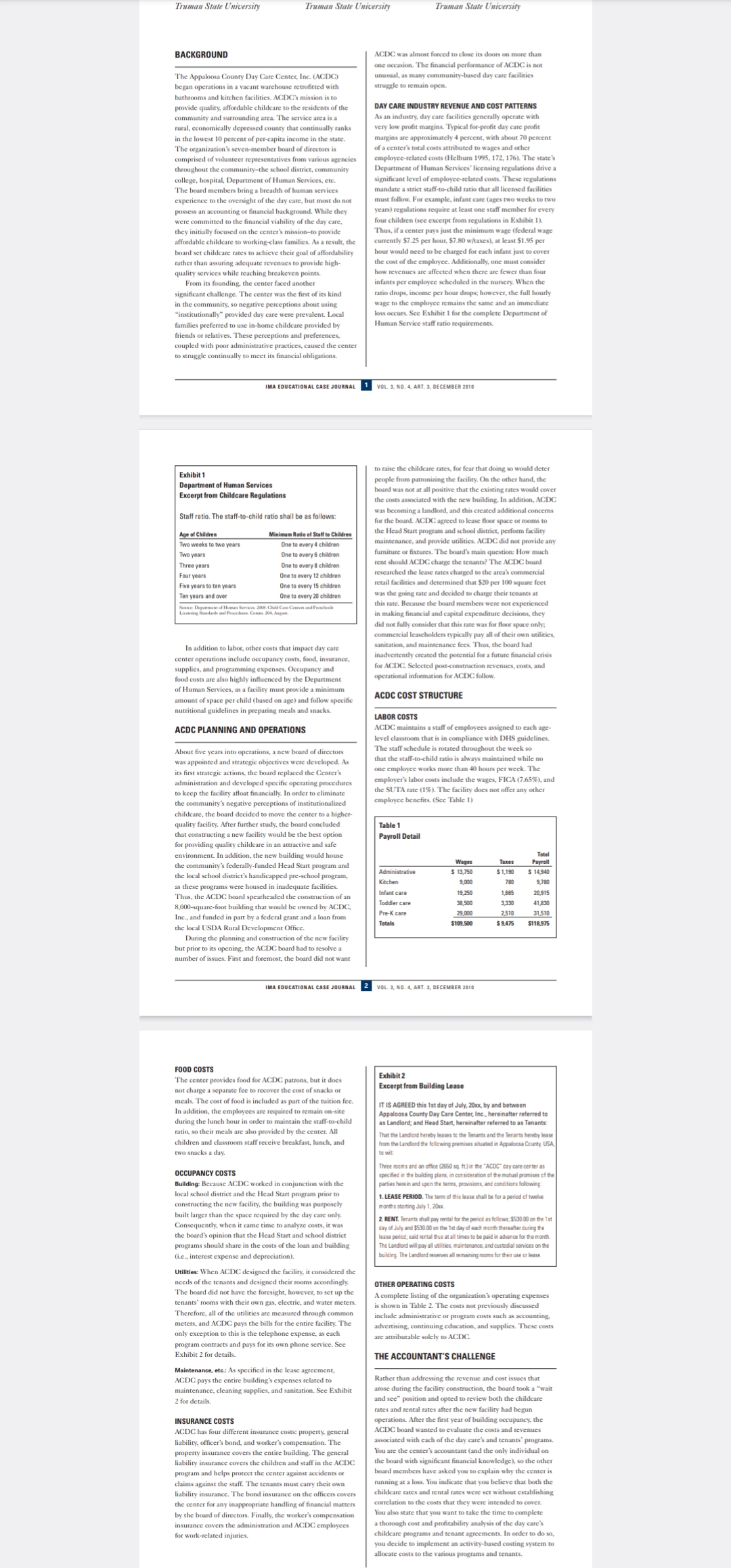

BACKGROUND

The Appaloosa County Day Care Center, Inc. (ACDC)

began operations in a vacant warehouse retrofitted with

bathrooms and kitchen facilities. ACDC's mission is to

provide quality, affordable childcare to the residents of the

community and surrounding area. The service area is a

rural, economically depressed county that continually ranks

in the lowest 10 percent of per-capita income in the state.

The organization's seven-member board of directors is

comprised of volunteer representatives from various agencies

throughout the community-the school district, community

college, hospital, Department of Human Services, etc.

The board members bring a breadth of human services

experience to the oversight of the day care, but most do not

possess an accounting or financial background. While they

were committed to the financial viability of the day care,

they initially focused on the center's mission-to provide

affordable childcare to working-class families. As a result, the

board set childcare rates to achieve their goal of affordability

rather than assuring adequate revenues to provide high-

quality services while reaching breakeven points.

Truman State University

From s founding, the center faced another

significant challenge. The center was the first of its kind

in the community, so negative perceptions about using

"institutionally" provided day care were prevalent. Local

families preferred to use in-home childcare provided by

friends or relatives. These perceptions and preferences,

coupled with poor administrative practices, caused the center

to struggle continually to meet i financial obligations.

Exhibit 1

Department of Human Services

Excerpt from Childcare Regulations

IMA EDUCATIONAL CASE JOURNAL

Staff ratio. The staff-to-child ratio shall be as follows:

Age of Children

Two weeks to two years

Two years

Three years

Four years

Five years to ten years

Ten years and over

Minimum Ratio of Staff to Children

One to every 4 children

One to every 6 children

One to every 8 children

One to every 12 children

One to every 15 children

One to every 20 children

Source Department of Human Services, 2008. Child Care Center and Preschools

Licensing Standards and Procedures Comm. 204, Augas.

In addition. labor, other costs that impact day care

center operations include occupancy costs, food, insurance,

supplies, and programming expenses. Occupancy and

food costs are also highly influenced by the Department

of Human Services, as a facility must provide a minimum

amount of space per child (based on age) and follow specific

nutritional guidelines in preparing meals and snacks.

ACDC PLANNING AND OPERATIONS

About five years into operations, a new board of directors

was appointed and strategic objectives were developed. As

its first strategic actions, the board replaced the Center's

administration and developed specific operating procedures

to keep the facility afloat financially. In order to eliminate

the community's negative perceptions of institutionalized

childcare, the board decided to move the center to a higher-

quality facility. After further study, the board concluded

that constructing a new facility would be the best option

for providing quality childcare in an attractive and safe

environment. In addition, the new building would house

the community's federally-funded Head Start program and

the local school district's handicapped pre-school program,

as these programs were housed in inadequate facilities.

Thus, the ACDC board spearheaded the construction of an

8,000-square-foot building that would be owned by ACDC,

Inc., and funded in part by a federal grant and a loan from

the local USDA Rural Development Office.

During the planning and construction of the new facility

but prior to its opening, the ACDC board had to resolve a

number of issues. First and foremost, the board did not want

IMA EDUCATIONAL CASE JOURNAL

FOOD COSTS

The center provides food for ACDC patrons, but it does

not charge a separate fee to recover the cost of snacks or

meals. The cost of food is included as part of the tuition fee.

In addition, the employees are required to remain on-site

during the lunch hour order to maintain the staff-to-child

ratio, so their meals are also provided by the center. All

children and classroom staff receive breakfast, lunch, and

two snacks a day.

OCCUPANCY COSTS

Building: Because ACDC worked in conjunction with the

local school district and the Head Start program prior to

constructing the new facility, the building was purposely

built larger than the space required by the day care only.

Consequently, when it came time to analyze costs, it was

the board's opinion that the Head Start and school district

programs should share in the costs of the loan and building

(i.e., interest expense and depreciation).

Utilities: When ACDC designed the facility, it considered the

needs of the tenants and designed their rooms accordingly.

The board did not have the foresight, however, to set up the

tenants' rooms with their own gas, electric, and water meters.

Therefore, all of the utilities are measured through common

meters, and ACDC pays the bills for the entire facility. The

only exception to this is the telephone expense, as each

program contracts and pays for its own phone service. See

Exhibit 2 for details.

Maintenance, etc.: As specified in the lease agreement,

ACDC pays the entire building's expenses related to

maintenance, cleaning supplies, and sanitation. See Exhibit

2 for details.

INSURANCE COSTS

ACDC has four different insurance costs: property, general

liability, officer's bond, and worker's compensation. The

property insurance covers the entire building. The general

liability insurance covers the children and staff in the ACDC

program and helps protect the center against accidents or

claims against the staff. The tenants must carry their own

liability insurance. The bond insurance on the officers covers

the center for any inappropriate handling of financial matters

by the board of directors. Finally, the worker's compensation

insurance covers the administration and ACDC employees

for work-related injuries.

ACDC was almost forced to close its doors on more than

one occasion. The financial performance of ACDC is not

unusual, s many community-based day care facilities

struggle to remain open.

Truman State University

DAY CARE INDUSTRY REVENUE AND COST PATTERNS

As an industry, day care facilities generally operate with

very low profit margins. Typical for-profit day care profit

margins are approximately 4 percent, with about 70 percent

of a center's total costs attributed to wages and other

employee-related costs (Helbumn 1995, 172, 176). The state's

Department of Human Services' licensing regulations drive a

significant level of employee-related costs. These regulations

mandate a strict staff-to-child ratio that all licensed facilities

must follow. For example, infant care (ages two weeks to two

years) regulations require at least one staff member for every

mom recams

four children (see excerpt from regulations in Exhibit 1).

Thus, if a center pays just the minimum wage (federal wage

currently $7.25 per hour, $7.80 w/taxes), at least $1.95 per

hour would need to be charged for each infant just to cover

the cost of the employee. Additionally, one must consider

how revenues are affected when there are fewer than four

infants per employee scheduled in the nursery. When the

ratio drops, income per hour drops; however, the full hourly

wage to the employee remains the same and an immediate

loss ccurs. See Ex ibit 1 the complete Department of

Human Service staff ratio requirements.

VOL. 3, NO. 4, ART. 3, DECEMBER 2010

to raise the childcare rates, for fear that doing so would deter

people from patronizing the facility. On the other hand, the

board was not at all positive that the existing rates would cover

the costs associated with the new building. In addition, ACDC

was becoming a landlord, and this created additional concerns

for the board. ACDC agreed to lease floor space or rooms to

the Head Start program and school district, perform facility

maintenance, and provide utilities. ACDC did not provide any

furniture or fixtures. The board's main question: How much

rent should ACDC charge the tenants? The ACDC board

researched the lease rates charged to the area's commercial

retail facilities and determined that $20 per 100 square feet

was the going rate and decided to charge their tenants at

this rate. Because the board members were not experienced

in making financial and capital expenditure decisions, they

did not fully consider that this rate was for floor space only;

commercial leaseholders typically pay all of their own utilities,

sanitation, and maintenance fees. Thus, the board had

inadvertently created the potential for a future financial crisis

for ACDC. Selected post-construction revenues, costs, and

operational information for ACDC follow.

ACDC COST STRUCTURE

LABOR COSTS

ACDC maintains a staff of employees assigned to each age-

level classroom that is in compliance with DHS guidelines.

The staff schedule is rotated throughout the week so

that the staff-to-child ratio is always maintained while no

one employee works more than 40 hours per week. The

employer's labor costs include the wages, FICA (7.65%), and

the SUTA rate (1%). The facility does not offer any other

employee benefits. (See Table 1)

Table 1

Payroll Detail

Administrative

Kitchen

Infant care

Toddler care

Pre-K care

Totals

Wages

$ 13,750

9,000

19,250

38,500

29,000

$109,500

VOL. 3, NO. 4, ART. 3, DECEMBER 2010

Exhibit 2

Excerpt from Building Lease

Taxes

$1,190

780

1,665

Total

Payroll

$ 14,940

9,780

20,915

3,330

41,830

2510

31,510

$9,475 $118,975

IT IS AGREED this 1st day of July, 20xx, by and between

Appaloosa County Day Care Center, Inc., hereinafter referred to

as Landlord; and Head Start, hereinafter referred to as Tenants:

That the Landlord hereby leases to the Tenants and the Tenants hereby lease

from the Landlord the following premises situated in Appaloosa County, USA

Three rooms and an office (2650 sq. ft.) in the "ACDC" day care center as

specified in the building plans, in consideration of the mutual promises of the

parties here in and upon the terms, provisions, and conditions following:

1.LEASE PERIOD. The term of this lease shall be for a period of twelve

months starting July 1, 20xx

2. RENT. Tenants shall pay rental for the period as follows: $530.00 on the 1st

day of July and $530.00 on the 1st day of each month thereafter during the

lease pericd; said rental thus at all times to be paid in advance for the month.

The Landlord will pay all utilities, maintenance, and custodial services on the

building. The Landlord reserves all remaining rooms for their use or lease.

OTHER OPERATING COSTS

A complete listing of the organization's operating expenses

is shown in Table 2. The costs not previously discussed

include administrative or program costs such as accounting.

advertising, continuing education, and supplies. These costs

are attributable solely to ACDC.

THE ACCOUNTANT'S CHALLENGE

Rather than addressing the revenue and cost issues that

arose during the facility construction, the board took a "wait

and see" position and opted to review both the childcare

rates and rental rates after the new facility had begun

operations. After the first year of building occupancy, the

ACDC board wanted to evaluate the costs and revenues

associated with each of the day care's and tenants' programs.

A

You are the center's accountant (and the only individual on

the board with significant financial knowledge), so the other

board members have asked you to explain why the center is

running at a loss. You indicate that you believe that both the

childcare rates and rental rates were set without establishing

correlation to the costs that they were intended to cover.

You also state that you want to take the time to complete

a thorough cost and profitability analysis of the day care's

childcare programs and tenant agreements. In order to do so,

you decide to implement an activity-based costing system to

allocate costs to the various programs and tenants.

Transcribed Image Text:Appaloosa County Day Care Center, Inc.

Kristen Irwin

Truman State University

BACKGROUND

The Appaloosa County Day Care Center, Inc. (ACDC)

began operations in a vacant warehouse retrofitted with

bathrooms and kitchen facilities. ACDC's mission is to

provide quality, affordable childcare to the residents of the

community and surrounding area. The service area is a

rural, economically depressed county that continually ranks

in the lowest 10 percent of per-capita income in the state.

The organization's seven-member board of directors is

comprised of volunteer representatives from various agencies

throughout the community-the school district, community

college, hospital, Department of Human Services, etc.

The board members bring a breadth of human services

experience to the oversight of the day care,

possess an accounting or financial background. While they

were committed to the financial viability of the day care,

they initially focused on the center's mission-to provide

affordable childcare to working-class families. As a result, the

board set childcare rates to achieve their goal of affordability

rather than assuring adequate revenues to provide high-

quality services while reaching breakeven points.

most do not

From its founding, the center faced another

significant challenge. The center was the first of its kind

in the community, so negative perceptions about using

"institutionally" provided day care were prevalent. Local

Debra Kerby

Truman State University

families preferred to use in-home childcare provided by

friends or relatives. These perceptions and preferences,

coupled with poor administrative practices, caused the center

to struggle continually to meet its financial obligations.

Exhibit 1

Department of Human Services

Excerpt from Childcare Regulations

IMA EDUCATIONAL CASE JOURNAL

Four years

Five years to ten years

Ten years and over

Staff ratio. The staff-to-child ratio shall be as follows:

Age of Children

Two weeks to two years.

Two years

Three years

Minimum Ratio of Staff to Children

One to every 4 children.

One to every 8 children

One to every 8 children

One to every 12 children

One to every 15 children

One to every 20 children

Souce Department of Human Services 2008 Child Care Cenon and Preschools

Licensing Standards and Procedures. Comm 34, August

In addition to labor, other costs that impact day care

center operations include occupancy costs, food, insurance,

supplies, and programming expenses. Occupancy and

food costs are also highly influenced by the Department

of Human Services, as a facility must provide a minimum

amount of space per child (based on age) and follow specific

nutritional guidelines in preparing meals and snacks.

ACDC PLANNING AND OPERATIONS

About five years into operations, a new board of directors

was appointed and strategic objectives were developed. As

its first strategic actions, the board replaced the Center's

administration and developed specific operating procedures

to keep the facility afloat financially. In order to eliminate

the community's negative perceptions of institutionalized.

childcare, the board decided to move the center to a higher-

quality facility. After further study, the board concluded.

that construct a new facility would be the best option

for providing quality childcare in an attractive and safe

environment. In addition, the new building would house

the community's federally-funded Head Start program and

the local school district's handicapped pre-school program,

as these programs were housed in inadequate facilities.

Thus, the ACDC board spearheaded the construction of an

8,000-square-foot building that would be owned by ACDC,

Inc., and funded in part by a federal grant and a loan from

the local USDA Rural Development Office.

During the planning and construction of the new facility

but prior to its opening, the ACDC board had to resolve a

number of issues. First and foremost, the board did not want

IMA EDUCATIONAL CASE JOURNAL

FOOD COSTS

The center provides food for ACDC patrons, but it does

not charge a separate fee to recover the cost of snacks or

meals. The cost of food is included as part of the tuition fee.

In addition, the employees are required to remain on-site

during the lunch hour in order to maintain the staff-to-child

ratio, so their meals are also provided I y the center. All

children and classroom staff receive breakfast, lunch, and

two snacks a day.

OCCUPANCY COSTS

Building: Because ACDC worked in conjunction with the

local school district and the Head Start program prior to

constructing the new facility, the building was purposely

built larger than the space required by the day care only.

Consequently, when it came time to analyze costs, it was

the board's opinion that the Head Start and school district

programs should share in the costs of the loan and building

(i.e., interest expense and depreciation).

Utilities: When ACDC designed the facility, it considered the

needs of the tenants and designed their rooms accordingly.

The board did not have the foresight, however, to set up the

tenants' rooms with their own gas, electric, and water meters.

Therefore, all of the utilities are measured through common

meters, and ACDC pays the bills for the entire facility. The

only exception this is the telephone expense, as each

program contracts and pays for its own phone service. See

Exhibit 2 for details,

Maintenance, etc.: As specified in the lease agreement,

ACDC pays the entire building's expenses related to

maintenance, cleaning supplies, and sanitation. See Exhibit

2 for details.

INSURANCE COSTS

ACDC has four different insurance costs: property, general

liability, officer's bond, and worker's compensation. The

property insurance covers the entire building. The general

liability insurance covers the children and staff in the ACDC

program and helps protect the center against accidents or

claims against the staff. The tenants must carry their own

liability insurance. The bond insurance on the officers covers

the center for any inappropriate handling of financial matters

by the board of directors. Finally, the worker's compensation

insurance covers the administration and ACDC employees

for work-related injuries.

ACDC was almost forced to close its doors on more than

one occasion. The financial performance of ACDC is not

unusual, as many community-based day care facilities

struggle to remain open.

DAY CARE INDUSTRY REVENUE AND COST PATTERNS

As an industry, day care facilities generally operate with

very low profit margins. Typical for-profit day care profit

margins are approximately 4 percent, with about 70 percent

of a center's total costs attributed to wages and other

employee-related costs (Helburn 1995, 172, 176). The state's

Department of Human Services' licensing regulations drive a

significant level of employee-related costs. These regulations

mandate a strict staff-to-child ratio that all licensed facilities

must follow. For example, infant care (ages two weeks to two

years) regulations require at least one staff member for every

four children (see excerpt from regulations in Exhibit 1).

Thus, if a center pays just the minimum wage (federal wage

currently $7.25 per hour, $7.80 w/taxes), at least $1.95 per

hour would need to be charged for each infant just to cover

the cost of the employee. Additionally, one must consider

how revenues are affected when there are fewer than four

infants per employee scheduled in the nursery. When the

ratio drops, income per hour drops; however, the full hourly

wage to the employee remains the same and an immediate

loss occurs. See Exhibit 1 for the complete Department of

Human Service staff ratio requirements.

VOL. 3, NO. 4, ART. 3, DECEMBER 2010

Sandra Weber

Truman State University

to raise the childcare rates, for fear that doing so would deter

people from patronizing the facility. On the other hand, the

board was not at all positive that the existing rates would cover

the costs associated with the new building. In addition, ACDC

was becoming a landlord, and this created additional concerns

for the board. ACDC agreed to lease floor space or rooms to

the Head Start program and school district, perform facility

maintenance, and provide utilities. ACDC did not provide any

furniture or fixtures. The board's main question: How much

rent should ACDC charge the tenants? The ACDC board

researched the lease rates charged to the area's commercial

retail facilities and determined that $20 per 100 square feet

was the going rate and decided to charge their tenants at

this rate. Because the board members were not experienced

in making financial and capital expenditure decisions, they

did not fully consider that this rate was for floor space only;

commercial leaseholders typically pay all of their own utilities,

sanitation, and maintenance fees. Thus, the board had

inadvertently created the potential for a future financial crisis

for ACDC. Selected post-construction revenues, costs, and

operational information for ACDC follow.

ACDC COST STRUCTURE

Table 1

Payroll Detail

LABOR COSTS

ACDC maintains a staff of employees assigned to each age-

level classroom that is in compliance with DHS guidelines.

The staff schedule is rotated throughout the week so

that the staff-to-child ratio is always maintained while no

one employee works more than 40 hours per week. The

employer's labor costs include the wages, FICA (7.65%), and

the SUTA rate (1%). The facility does not offer any other

employee benefits. (See Table 1)

Administrative

Kitchen

Infant care

Pre-K care

Totals

ISSN 1940-204X

Wages

$ 13.750

9,000

19,250

38,500

29,000

$109,500

VOL. 3, NO. 4, ART. 3, DECEMBER 2010

Exhibit 2

Excerpt from Building Lease

Taxes

$1,190

780

1.665

3,330

$9,475

Total

Payroll

$14,940

9,780

20,915

41,830

31.510

$118.975

IT IS AGREED this 1st day of July, 20xx, by and between

Appaloosa County Day Care Center, Inc., hereinafter referred to

as Landlord; and Head Start, hereinafter referred to as Tenants:

That the Landlord hereby leases to the Tenants and the Tenants hereby lease

from the Landlord the following premises situated in Appaloosa County, USA,

Three rooms and an office (2650 sq. ft.) in the "ACDC" day care center as

specified in the building plans, in consideration of the mutual promises of the

parties herein and upon the terms, provisions, and conditions following:

1.LEASE PERIOD. The term of this lease shall be for a period of twelve

months starting July 1, 20

2. RENT. Tenants shall pay rental for the period as follows $530.00 on the 1st

day of July and $530.00 on the 1st day of each month thereafter during the

lease period, said rental thus at all times to be paid in advance for the month.

The Landlord will pay all utilities, maintenance, and custodial services on the

building. The Landlord reserves all remaining rooms for their use or lease.

OTHER OPERATING COSTS

A complete listing of the organization's operating expenses

is shown in Table 2. The costs not previously discussed

include administrative or program costs such as accounting.

advertising, continuing education, and supplies. These costs

are attributable solely to ACDC,

THE ACCOUNTANT'S CHALLENGE

Rather than addressing the revenue and cost issues that

arose during the facility construction, the board took a "wait

and see" position and opted to review both the childcare

rates and rental rates after the new facility had begun

operations. After the first year of building occupancy, the

ACDC board d to evaluate the costs

associated with each of the day care's and tenants' programs.

You are the center's accountant (and the only individual on

the board with significant financial knowledge), so the other

board members have asked you to explain why the center is

running at a loss. You indicate that you believe that both the

childcare rates and rental rates were set without establishing

correlation to the costs that they were intended to cover

You also state that you want to take the time to complete

a thorough cost and profitability analysis of the day care's

childcare programs and tenant agreements. In order to do so,

you decide to implement an activity-based costing system to

allocate costs to the various programs and tenants.

revenues

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- Many organizations have differentiated themselves in the marketplace by their "low cost" value proposition to customers (i.e. Spirit Airlines, Dollar Tree, Walmart, and Aldi). To achieve this, the organization fine-tunes their business model to remove as many overhead costs and unnecessary costs so it may pass those savings on to its customers. Select a domestic or international business that has a "low cost" value proposition to its customers and consider the following questions: How does it market itself? How does a low-cost operating structure make them stand out and succeed in the market? Is "low cost" a sustainable model for this company? Evaluate this strategy from an ethical perspective.arrow_forwardCase Studies in Management: Bank of America Corporation - 2011 Briefly discuss the organization and its product and services. Discuss the strategic dilemma that your company is facing. Show existing vision, mission, objectives and strategies. Evaluate the mission statement. If the mission statement does not exist or needs to be revised, please craft one or revise the existing mission and tell why it needed to be improved. Identify all of the organization's external opportunities and threats. Highlight and explain the three most significant opportunities and the three most significant threats. Identify and discuss at least 3 major competitors. Compare your organizations performance with the performance of their competitors. Identify all of the organization's internal strengths and weaknesses. Highlight and explain the three most significant strengths and the three most significant weaknesses. Calculate and discuss key financial ratios. Please include at least one ratio from each…arrow_forwardelect a Balanced Scorecard publicly available on the internet and discuss how it can benefit the entity and any concerns you have regarding how this particular scorecard could potentially not benefit the entity or in fact add negative value to the entity. Financial Component of Scorecard IF OPTION 1 (FOUND A SCORECARD) Clear, detailed explanation of the strengths and potential weaknesses of this component of the scorecard. Learning and Growth Component of Scorecard IF OPTION 1 (FOUND A SCORECARD) Clear, detailed explanation of the strengths and potential weaknesses of this component of the scorecard. Customer Perspective Component of Scorecard IF OPTION 1 (FOUND A SCORECARD) Clear, detailed explanation of the strengths and potential weaknesses of this component of the scorecard. Customer Perspective Component of Scorecard IF OPTION 1 (FOUND A SCORECARD) Clear, detailed explanation of the strengths and potential weaknesses of this component of the scorecard. Internal Processes Component…arrow_forward

- Many cities, counties and public safety organizations list their strategic plan on the web. Search the web for a city, county or public safety strategic plan. Describe the details of the plan, to include goals, objectives, mission and any a supporting data.arrow_forwardKeep in mind that you are acting in the role of the Strategic Management Consultant, whose job is to recommend based on your knowledge and expertise, suitable and appropriate recommendations to Management. Be convincing, use supporting examples of where your recommendations have been used before. Justify, Justify, Justify! Scenario: Maria is considering operating a local business in the beauty and cosmetology sector in the island of Trinidad. She has completed research into the operations of similar businesses locally and intends to market and sell her products initially at the local level, with the possibility of extending at the regional level in the near future. Maria understands that to shape the business’s overall strategy there are various strategic drivers both internally and externally which must be considered and wants expert advice on these drivers relevant to her business. She is also struggling with deciding on the best structure for the organization, as well as the…arrow_forwardIdentify the three most important factors to consider when selecting the strategies you will use to implement problem solutions. Justify your selections by providing specific business examples that support your ideas.arrow_forward

- Using the Web or library resources, research current threats todata. Write a short essay describing the current threats and brieflydescribe in detail how to mitigate each threat.arrow_forwardplease draw the decision treearrow_forwardList and describe two potential methods or models (mathematical or conceptual) that can be used to predict impacts in an environmental impact assessment (EIA) process. Illustrate your answer with relevant examples.arrow_forward

- Briefly describe a service of your choice. Offer two recommendations for how the company/service provider in your example could manage the characteristics of services to create more value for its customers.arrow_forwardConstruct and submit a Decision Tree that depicts the information provided in the case to either continue developing a new software product or to abandon the project due to its high cost and uncertain market potential. In addition, you must provide an explanation of your decision tree and support your decision with the literature.arrow_forwardKeep in mind that you are acting in the role of the Strategic Management Consultant, whose job is to recommend based on your knowledge and expertise, suitable and appropriate recommendations to Management. Be convincing, use supporting examples of where your recommendations have been used before. Justify, Justify, Justify! Scenario: Maria is considering operating a local business in the beauty and cosmetology sector in the island of Trinidad. She has completed research into the operations of similar businesses locally and intends to market and sell her products initially at the local level, with the possibility of extending at the regional level in the near future. Maria understands that to shape the business’s overall strategy there are various strategic drivers both internally and externally which must be considered and wants expert advice on these drivers relevant to her business. She is also struggling with deciding on the best structure for the organization, as well as the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Practical Management ScienceOperations ManagementISBN:9781337406659Author:WINSTON, Wayne L.Publisher:Cengage,

Operations ManagementOperations ManagementISBN:9781259667473Author:William J StevensonPublisher:McGraw-Hill Education

Operations ManagementOperations ManagementISBN:9781259667473Author:William J StevensonPublisher:McGraw-Hill Education Operations and Supply Chain Management (Mcgraw-hi...Operations ManagementISBN:9781259666100Author:F. Robert Jacobs, Richard B ChasePublisher:McGraw-Hill Education

Operations and Supply Chain Management (Mcgraw-hi...Operations ManagementISBN:9781259666100Author:F. Robert Jacobs, Richard B ChasePublisher:McGraw-Hill Education

Purchasing and Supply Chain ManagementOperations ManagementISBN:9781285869681Author:Robert M. Monczka, Robert B. Handfield, Larry C. Giunipero, James L. PattersonPublisher:Cengage Learning

Purchasing and Supply Chain ManagementOperations ManagementISBN:9781285869681Author:Robert M. Monczka, Robert B. Handfield, Larry C. Giunipero, James L. PattersonPublisher:Cengage Learning Production and Operations Analysis, Seventh Editi...Operations ManagementISBN:9781478623069Author:Steven Nahmias, Tava Lennon OlsenPublisher:Waveland Press, Inc.

Production and Operations Analysis, Seventh Editi...Operations ManagementISBN:9781478623069Author:Steven Nahmias, Tava Lennon OlsenPublisher:Waveland Press, Inc.

Practical Management Science

Operations Management

ISBN:9781337406659

Author:WINSTON, Wayne L.

Publisher:Cengage,

Operations Management

Operations Management

ISBN:9781259667473

Author:William J Stevenson

Publisher:McGraw-Hill Education

Operations and Supply Chain Management (Mcgraw-hi...

Operations Management

ISBN:9781259666100

Author:F. Robert Jacobs, Richard B Chase

Publisher:McGraw-Hill Education

Purchasing and Supply Chain Management

Operations Management

ISBN:9781285869681

Author:Robert M. Monczka, Robert B. Handfield, Larry C. Giunipero, James L. Patterson

Publisher:Cengage Learning

Production and Operations Analysis, Seventh Editi...

Operations Management

ISBN:9781478623069

Author:Steven Nahmias, Tava Lennon Olsen

Publisher:Waveland Press, Inc.