Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

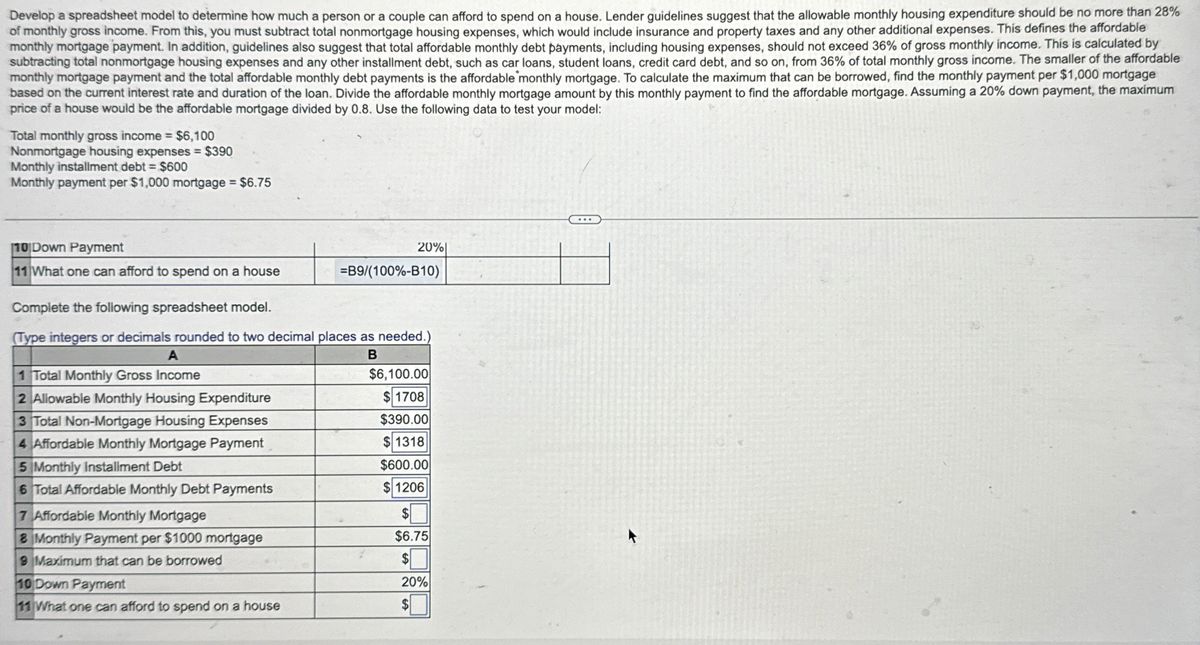

Transcribed Image Text:Develop a spreadsheet model to determine how much a person or a couple can afford to spend on a house. Lender guidelines suggest that the allowable monthly housing expenditure should be no more than 28%

of monthly gross income. From this, you must subtract total nonmortgage housing expenses, which would include insurance and property taxes and any other additional expenses. This defines the affordable

monthly mortgage payment. In addition, guidelines also suggest that total affordable monthly debt payments, including housing expenses, should not exceed 36% of gross monthly income. This is calculated by

subtracting total nonmortgage housing expenses and any other installment debt, such as car loans, student loans, credit card debt, and so on, from 36% of total monthly gross income. The smaller of the affordable

monthly mortgage payment and the total affordable monthly debt payments is the affordable monthly mortgage. To calculate the maximum that can be borrowed, find the monthly payment per $1,000 mortgage

based on the current interest rate and duration of the loan. Divide the affordable monthly mortgage amount by this monthly payment to find the affordable mortgage. Assuming a 20% down payment, the maximum

price of a house would be the affordable mortgage divided by 0.8. Use the following data to test your model:

Total monthly gross income = $6,100

Nonmortgage housing expenses = $390

Monthly installment debt = $600

Monthly payment per $1,000 mortgage = $6.75

10 Down Payment

20%

11 What one can afford to spend on a house

=B9/(100%-B10)

Complete the following spreadsheet model.

(Type integers or decimals rounded to two decimal places as needed.)

A

1 Total Monthly Gross Income

2 Allowable Monthly Housing Expenditure

3 Total Non-Mortgage Housing Expenses

4 Affordable Monthly Mortgage Payment

5 Monthly Installment Debt

6 Total Affordable Monthly Debt Payments

7 Affordable Monthly Mortgage

8 Monthly Payment per $1000 mortgage

9 Maximum that can be borrowed

10 Down Payment

11 What one can afford to spend on a house

B

$6,100.00

$1708

$390.00

$1318

$600.00

$1206

$

$6.75

$

20%

277

$

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- You attend college and have 2 loans: A SUBSIDIZED loan for $40,000 with 3.88% APR, and anUNSUBSIDIZED loan for $28,000 with 4.06% APR. You plan to elect standard repayment. Calculate yourtotal monthly payment for both loans.arrow_forwardUse Worksheet 5.3. Rachel and Alexander Harrison need to calculate the amount they can afford to spend on their first home. They have a comt annual income of $67,500 and have $37,000 available for a down payment and closing costs. The Harrisons estimate that homeowner's insurance property taxes will be $250 per month. They expect the mortgage lender to use a 30 percent (of monthly gross income) mortgage payment afford ratio, to lend at an interest rate of 6 percent on a 30-year mortgage, and to require a 10 percent down payment. Based on this information, use th home affordability analysis form in Worksheet 5.3 to determine the highest-priced home the Harrisons can afford. Assume that closing costs are o of the down payment. Round the answer to the nearest dollar.arrow_forwardVijayarrow_forward

- Suppose you earn a gross income of $2,920.00 per month and apply for a mortgage with a monthly PITI of $908.12. You have other financial obligations totaling $169.36 per month. If the lending ratio guidelines are as given in the table below, what type of mortgage, if any, would you qualify for? Mortgage Type Housing Expense Ratio Total Obligations Ratio FHA 29% 41% Conventional 28% 36% A. FHA only B. Conventional only C. FHA and Conventional D. None of the abovearrow_forwardThat calculated monthly expense should include all housing costs (such as insurance, property taxes, etc), let’s estimate this means they would have around $950 a month for their mortgage payment and they have poor credit so qualify for a loan with an APR of 5.481%. What size 30 year home mortgage loan could they pay off with a monthly payment of $950?arrow_forwardAnswer the following question using a spreadsheet and the material in the appendix. You would like to buy a house. Assume that given your income, you can afford to pay $12,000 a year to a lender for the next 30 years. If the interest rate is 7% how much can you borrow today based on your ability to pay? What about if the interest rate is 3%? Maximum mortgage at 7%: $ Maximum mortgage at 3%: $arrow_forward

- Michelle Duncan wants to know what price home she can afford. Her annual gross income is $49,800. She owes $840 per month on other debts and expects her property taxes and homeowners insurance to cost $310 per month. She knows she can get an 9.50%, 30-year mortgage so her mortgage payment factor is 8.41. She expects to make a 25% down payment. What is Michelle's affordable home purchase price? (Round your answer to the nearest dollar amount.)arrow_forwardA family needs to take out a 15-year home mortgage loan of $170,000 through a local bank. Annual interest rates for 15-year mortgages at the bank are 3.5% compounded monthly. (a) Compute the family's monthly mortgage payment under this loan. (b) How much interest will the family pay over the life of the loan?arrow_forwardBased on the following data, calculate the items requested: Buying Costs Annual mortgage payments Property taxes Down payment/closing costs Growth in equity Insurance/maintenance Estimated annual appreciation Rental Costs Annual rent Insurance Security deposit $ 8,230 $ 230 $ 1,075 Assume an after-tax savings interest rate of 7 percent and a tax rate of 32 percent. Assume this individual has other tax deductions that exceed the standard deduction amount. Rental cost Buying cost a. Calculate total rental cost and total buying cost. (Do not round intermediate calculations. Round your answers to the nearest whole dollar.) $ 10,450 (10,000 is interest) $ 2,120 $ 5,150 $ 450 $1,900 $ 2,550 b. Would you recommend buying or renting? O Renting O Buyingarrow_forward

- Suppose you earn a gross income of $2,710.00 per month and apply for a mortgage with a monthly PITI of $501.35. You have other financial obligations totaling $428.18 per month. If the lending ratio guidelines are as given in the table below, what type of mortgage, if any, would you qualify for? Mortgage Type Housing Expense Ratio Total Obligations Ratio FHA 29% 41% Conventional 28% 36% O FHA only O Conventional only O FHA and Conventional O None of the abovearrow_forwardInstructions Answer the journal prompts according to the scenario below: Joe-Bob wants to buy a car and will need to take out a loan in order to make the purchase. His current monthly income is $3,500 per month. His mortgage payment is $900 per month, and his student loan payment is $350 per month. Note: You do not need to take taxes into consideration for this journal. According to the affordability formulas given, can he afford to take out another loan? • When should he follow the affordability formulas? In what cases should he not? • How could taking out the car loan impact his other priorities?arrow_forward13) Some financial advisors recommend that your monthly mortgage payment be no higher than 28% of your monthly net income. What is 28% of your monthly net income, as determined in question twelve? This is the estimated amount you can afford per month for a mortgage. 4,518*0.28 $1,265 28% of my monthly net income is $1,265. 14) We can calculate how much of a house you can afford using the loan formula. In question thirteen, you determined the monthly mortgage payment you can afford. Using this value for the regular monthly payment, calculate the present value (P), assuming you receive a 30-year mortgage (loan) with an annual interest rate of 6.328% with monthly compounding. (Note: This rate is realistic for a mortgage initiated in January 2024.) I need to use Loan formula to find the present value (P). please help mearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education