ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

thumb_up100%

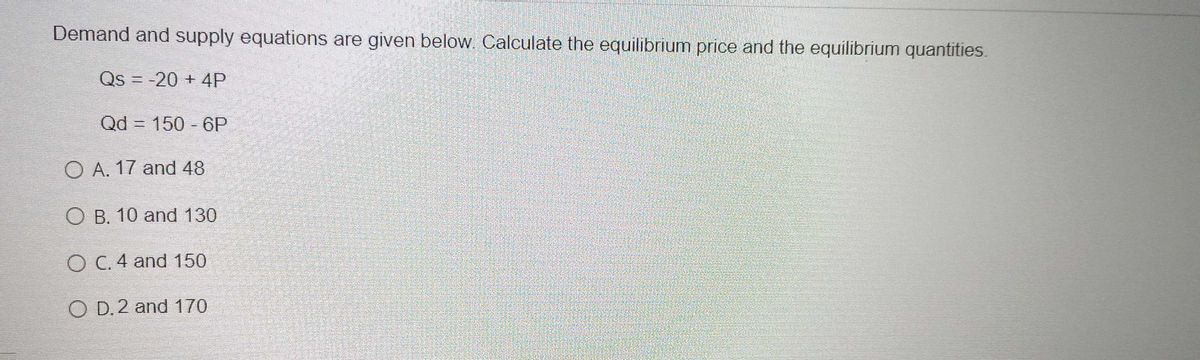

Transcribed Image Text:Demand and supply equations are given below Calculate the equilibrium price and the equilibrium quantities.

Qs = -20 + 4P

Qd = 150 - 6P

O A. 17 and 48

O B. 10 and 130

O C. 4 and 150

O D. 2 and 170

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- ADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P = 80 – 2Qd. Supply is represented by the equation P = -20 + 2Qs, where Qgand Qg are quantity demanded and quantity supplied, respectively, and Pis price. Instructions: Round your answer for price to 2 decimal places and enter your answer for quantity as a whole number. Using the equilibrium condition Qs = Qd, solve the equations to determine equilibrium price and equilibrium quantity. Equilibrium price = $ Equilibrium quantity = unitsarrow_forwardThe following questions pertain to analysis of the supply and demand scenario derived from the schedules below: Candy Canes QD QS 20 2. 14 14 21 4 28 Create a graph of the supply and curves from this chart for use in your analysis. 19. What would be the result of a government-imposed price celling orn candy canes set at the price of 1 dollar? O a A surplus of candy canes would occur, and this is evident because of the quantity of candy canes supplied at the price of 1 dollar is much greater than the quantity of candy canes demanded. A shortage of candy canes would occur, and this is evident because the quantity of candy canes d is much greater than the quantity of candy canes supplied. There would be no result. The price ceiling is set above equilibrlum and is therefore not binding. O b ...arrow_forwardQuantity Demanded 6 7 8 9 10 11 12 Price $8 7 6 5 4 3 2 Refer to the above table. If demand decreased by 4 units at each price and supply decreased by 2 units at each price, what would the new equilibrium price and quantity be? Multiple Choice O $6 and 6 units $5 and 5 units O $4 and 6 units Quantity Supplied 10 9 8 7 6 5 4 $7 and 7 unitsarrow_forward

- Which of the following is consistent with the law of supply? O A. An increase in the market price of oranges causes an increase in the production of oranges. OB. A decline in labor productivity leads to fewer apartment buildings being constructed. OC. A doubling of the price of salt led to a 5 percent drop in the quantity of salt consumed. OD. More passengers chose to travel by airplane after strong price competition. 23arrow_forwardAsaaaparrow_forwardA shortage will occur if a is set the equilibrium price. O A)price ceiling, below B) price floor, below C) price ceiling, above D) price floor, abovearrow_forward

- ADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P=80−2Qd.P=80−2Qd. Supply is represented by the equation P=−20+2Qs,P=−20+2Qs, where Qd and Qs are quantity demanded and quantity supplied, respectively, and P is price.Instructions: Round your answer for price to 2 decimal places and enter your answer for quantity as a whole number. Using the equilibrium condition Qs = Qd, solve the equations to determine equilibrium price and equilibrium quantity.arrow_forwardO A to C. OB to A. Price of coconuts OB to E. E Reference: Ref 3-1 Figure: Supply of Coconuts OC to A. S3 B An increase in coconut farmers wages could be represented in the figure as a movement from S₁ Quantity of coconuts S2 Book Proarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education