FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

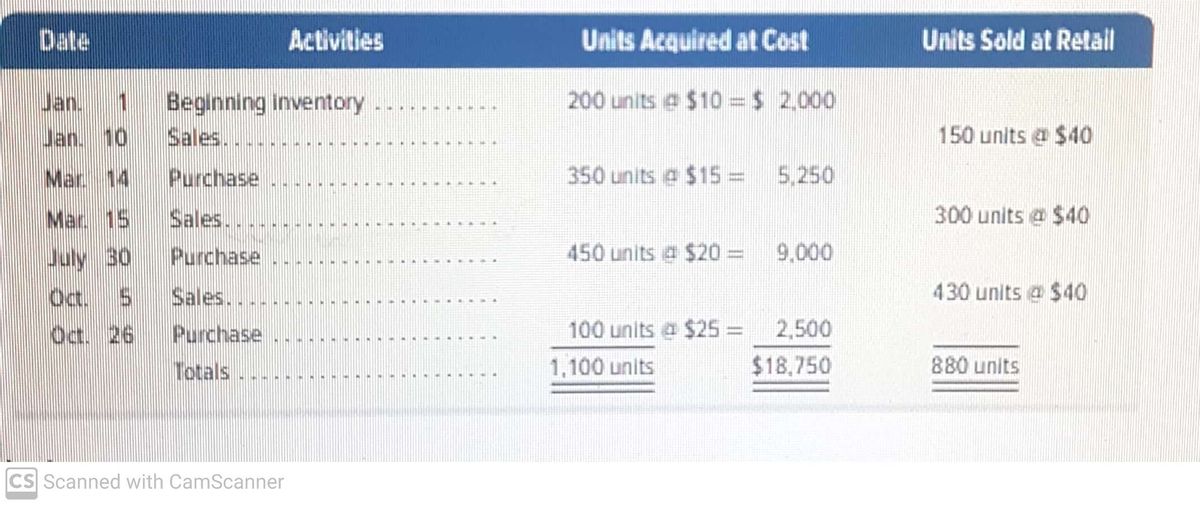

Determine the costs assigned to ending inventory and to cost of goods sold using (a) FIFO and (b) LIFO. Then (c) compute the gross margin for each method

Transcribed Image Text:Date

Activities

Units Acquired at Cost

Units Sold at Retail

Jan. 1

200 units e $10 = $ 2.000

Beginning inventory

Sales...

14.

Jan. 10

150 units @ $40

Mar 14

Purchase

350 units a $15 =

5,250

Mar. 15

Sales..

300 units e $40

July 30

Purchase

450 units a $20 =

9,000

Oc. 5

Sales...-

430 units a $40

Oct. 26

Purchase

100 units a $25% =

2,500

%3D

Totals

1,100 units

$18,750

880 units

CS Scanned with CamScanner

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- How do i calculate ending inventory and cost of goods sold using LIFO?arrow_forwardFIFO, Average cost, and LIFO are often used for inventory valuation purposes. Compare these methods and discuss the effects of each method in the determination of income and asset managementarrow_forwardExplain the gross profit method of estimating ending inventory.arrow_forward

- According to our authors, define “cost” as it relates to determining the value of inventory. Provide examples.arrow_forwardIdentify each item as describing the FIFO method, LIFO method, or average cost method of inventory valuation. A. Involves calculating the total number of units in the warehouse FIFO LIFO Average cost B. To determine cost of goods sold, begin with the earliest goods acquired FIFO LIFO Average cost C. To determine merchandise inventory balance, begin with the earliest goods acquired FIFO LIFO Average costarrow_forwardThe cost of goods sold is based on the oldest purchases under which method of calculating inventory cost? O A. weighted average method O B. first in, first out (FIFO) O C. gross profit method O D. last in, first out (LIFO)arrow_forward

- Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and cost of goods sold.arrow_forwardIdentify four inventory costing methods for assigning cost to ending inventory and cost of goods sold and briefly explain the difference in the methods.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education