FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:**Understanding Double Taxation in Corporate Dividends (2018)**

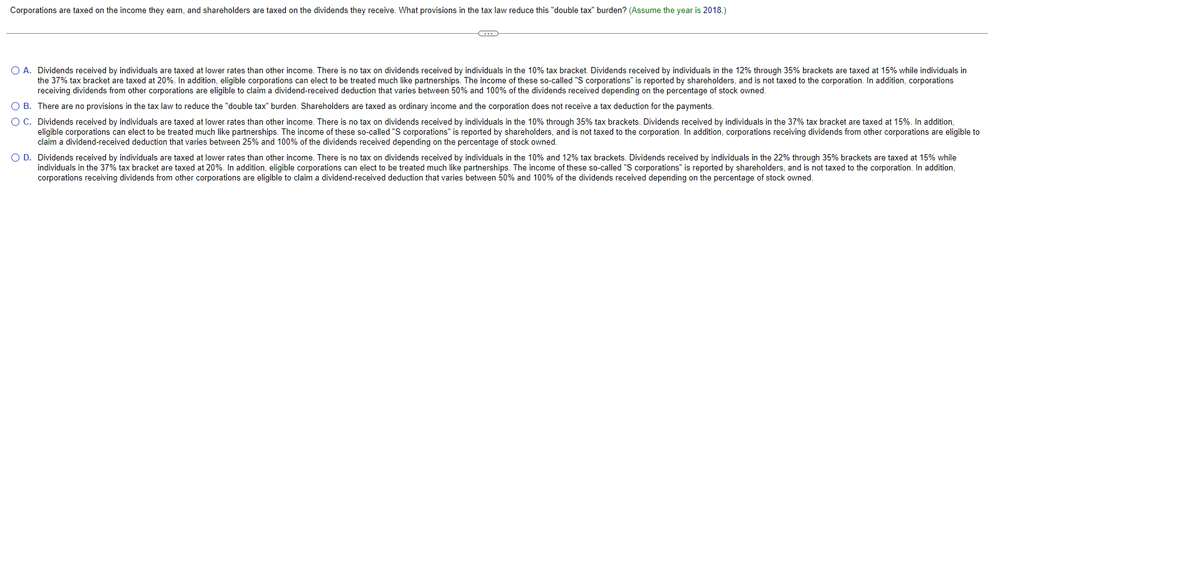

Corporations are taxed on their income, and shareholders are taxed on the dividends they receive. What provisions in the tax law reduce this "double tax" burden?

1. **Option A**:

- Dividends received by individuals are taxed at lower rates than other income.

- No tax on dividends in the 10% tax bracket.

- Dividends in the 12% through 35% brackets are taxed at 15%.

- Dividends in the 37% tax bracket are taxed at 20%.

- Eligible corporations can elect to be treated like partnerships ("S corporations"), with income reported by shareholders, not taxed to the corporation.

- Corporations receiving dividends can claim a deduction between 50% and 100% of the dividends, depending on stock ownership.

2. **Option B**:

- No tax law provisions to reduce the "double tax" burden.

- Shareholders are taxed as ordinary income, and corporations receive no tax deduction for payments.

3. **Option C**:

- Dividends received by individuals are taxed at lower rates than other income.

- No tax on dividends in the 10% through 35% tax brackets.

- Dividends in the 37% tax bracket taxed at 15%.

- Eligible corporations can elect to be treated like partnerships ("S corporations"), with income reported by shareholders and not taxed to the corporation.

- Corporations receiving dividends can claim a deduction between 25% and 100%, depending on stock ownership.

4. **Option D**:

- Dividends received by individuals are taxed at lower rates than other income.

- No tax on dividends in the 10% and 12% tax brackets.

- Dividends in the 22% through 35% brackets taxed at 15%.

- Dividends in the 37% tax bracket taxed at 20%.

- Eligible corporations can elect to be treated like partnerships, with similar provisions as "S corporations."

- Corporations receiving dividends can claim a deduction between 50% and 100%, depending on stock ownership.

This information helps clarify how tax laws aim to alleviate the impact of double taxation on corporate dividends, particularly through varied taxation strategies and possible deductions.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- True or False Corporations are required to file a tax return annually regardless of their taxable income.arrow_forwardIf XYZ Corporation is a shareholder of BCD Corporation, how many times will BCD's before-tax income potentially be taxed? Has Congress provided any tax relief for this result? Explain.arrow_forwardNonearrow_forward

- Why would a corporation purchase the stock of another corporation? a. To prevent double taxation of its shareholders b. Because dividends received by a corporation are partially tax-exempt c. It is equivalent to a tax carried forward d. It is equivalent to a tax carried backarrow_forwardGreen Corporation is required to change its method of accounting for federal income tax purposes. The change will require an adjustment to income to be made over three tax periods. Joe, the sole shareholder of Green, wants to better understand the implications of this adjustment for E&P purposes, because he anticipates a distribution from Green in the current year. Explain to Joe the impact of the adjustment on E&P.arrow_forwardAll resident corporations (except tax-exempt Crown corporations and registered charities) have to file a corporation income tax (T2) return every tax year even if there is no tax payable. True Falsearrow_forward

- Is it possible for shareholders to defer or avoid the second level of tax on corporate income altogether? Briefly explain.arrow_forwardThis answer is wrong . please give me the right answer.arrow_forwardWhich of the following accurately describes the tax implications of C corporations and their shareholders? a) Pass-through taxation b) Double taxation c) Tax-exempt status d) Reduced capital gains tax ratearrow_forward

- In each of the following cases, compute the corporation's regular tax, average tax rate and marginal tax rate: Use 2017 tax rate schedule if needed. Required: a. Silva Corporation has $168,000 taxable income for its tax year ended December 31, 2017. b. Goyal Corporation has $168,000 taxable income for its tax year ended December 31, 2018. c. Carver Corporation has $168,000 taxable income for its tax year ended October 31, 2018. Note: For all requirements, Do not round intermediate calculations. Round your final answer to nearest whole dollar amount and average tax rate answer to 2 decimal places. a. b. C. Corporation's Regular Tax $ LA LA X Answer is complete but not entirely correct. Corporation's Marginal Tax Rate 39 % 21 % 37 X % $ $ 48,770 35,280 168,000 X Corporation's Average Tax Rate 35.00 21.00 0.00 % % %arrow_forward1)During the year, CDE Corporation earned enough profits to pay dividends to its shareholders. CDE is a C corporation. What are the tax consequences of this distribution? The corporation will increase their earnings and profits by the amount distributed. The corporation will reduce its taxable income by the amount distributed to the shareholders. The corporation will pay a flat tax of 21% on the amount distributed. The shareholders also include their dividends received in taxable income. There are no direct tax consequences for either the corporation or the shareholders. 20 Choose the response that correctly describes a guaranteed payment. A loan payment from the partnership to pay back a loan from a partner. A loan payment from the partner to pay back a loan from a partnership. A payment made to a partner from the profits of the partnership. A payment made to a partner without regard to the income of the partnership. 3)Which of the following expenses may a partnership…arrow_forwardShareholders in a corporation are obligated to pay income tax twice on one stream of income in a process called double taxation. Other than personal income taxes, which type of tax must shareholders pay? a) Self Employment Tax b) Corporate Dividend Tax c) Federal Income Tax d) Capital Gains Taxarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education