ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

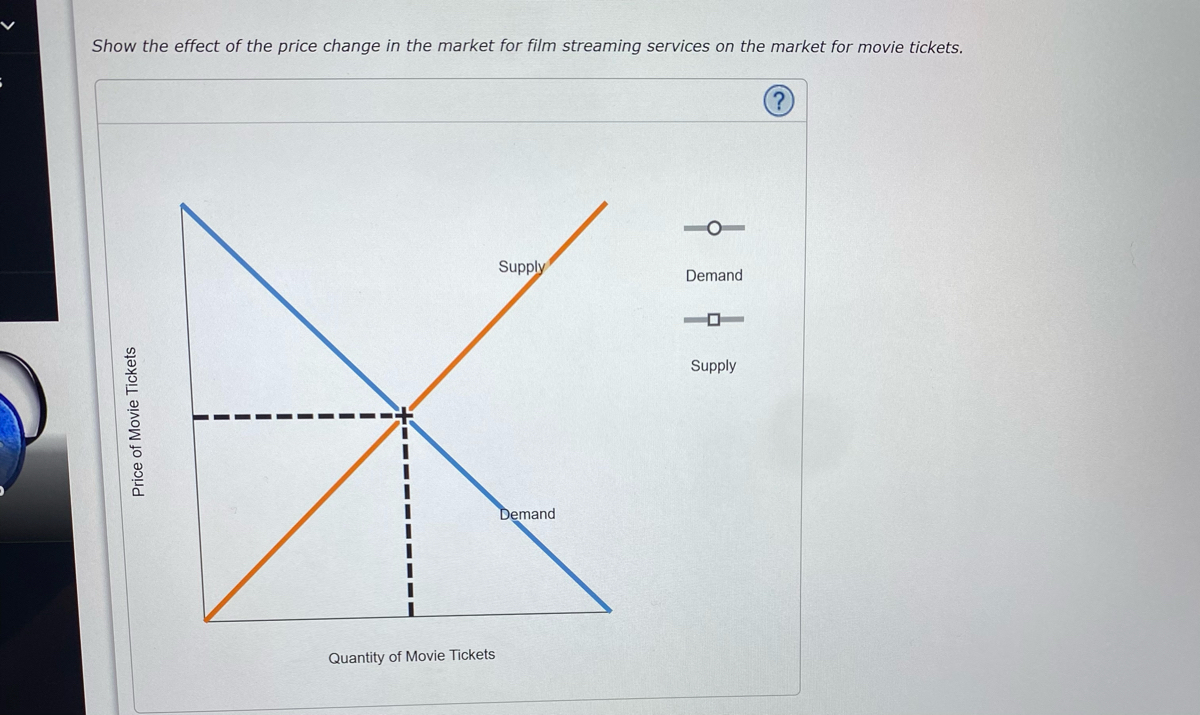

Transcribed Image Text:Show the effect of the price change in the market for film streaming services on the market for movie tickets.

Price of Movie Tickets

Quantity of Movie Tickets

Supply

Demand

Demand

Supply

Transcribed Image Text:Consider the relationship between film streaming services and Internet services.

Show the effect of the price change in the market for film streaming services on the market for Internet services.

Price of Internet Services

I

Supply

Demand

Quantity of Internet Services

Demand

Supply

Expert Solution

arrow_forward

Step 1: Define demand and supply

The demand is the desire of the individual to buy a product or good based on willingness and ability to pay. It depends upon the income of the consumers. The supply is the amount of goods that is produced by a producer to consumers. The supplied goods are purchased by consumers in the market.

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Which of the following causes a shift in the supply of golf clubs? golf courses reduce the fee they charge to play golf balls become more expensive O golf carts are banned golf club manufacturers no longer have to provide health insurance for their workersarrow_forwardThe price of tea cakes goes up by 1%. As a result, the quantity purchased of tea falls by 1.5%. Tea and tea cakes are complements Tea cakes are an inferior good relative to tea Total revenue associated with tea will rise Tea and tea cakes are substitutesarrow_forwardConsider the market for potato, if potatoes are considered as inferior good and income rises at the same time that low temperature kills some potato buds. Change in Demand Increase Decrease Did not Change Indeterminate Change in Supply Increase Decrease Did not Change Indeterminatearrow_forward

- Please no written by hand and no image The market demand curve represents the sum of the quantities demanded by all the buyers at each price of the good. is found by vertically adding the individual demand curves. represents the sum of the prices that all the buyers are willing to pay for a given quantity of the good. slopes upward.arrow_forwardIf the price of rubber falls, how will that affect the demand for rubber tires? a) demand will not shift b) demand will shift to the left c)demand will shift to the right d) Demand shifts depends on the if tires are inferior or normalarrow_forwardA demand curve shows the relationship between price and _________________ on a graph. quantity demanded quantity produced economies of scale costsarrow_forward

- Write down the factors affecting demand. Which of the following factors will cause the following products to increase or decrease? Convenience food (sold in food shops and supermarkets) Products purchased in the internet Mobile phones Pay-per - view- television programming Books Airline travel within Us; air travel with UKarrow_forwardwhich of the following does not directly influence the demand for a good? the size of the population consumer preferences the cost of producing the good average consumer incomearrow_forwardDemand for the desired quantity of a good that is backed by the ability to buy that good is known as: A. Effective Demand B. Derived Demandarrow_forward

- Exhibit: The Demand for Bungalow Bob's Bagels Price Quantity per period 30 Demand is price elastic between: $0.30 and $0.40. $0.80 $0.70 $0.60 $0.50 40 50 60 $0.40 and $0.50. $0.50 and $0.60. $0.60 and $0.70. $0.40 70 $0.30 80arrow_forwardThe following graph displays four demand curves (LL, MM, NN, and 00) that intersect at point A. 200 180 N. 160 M 140 E 120 t. 100 80 60 40 N. 20 20 40 60 80 100 120 140 160 180 200 QUANTITY (Units) A + PRICE (Dollars per unit)arrow_forwardWhich of the following is least likely to increase the demand for new tires? a decrease in the price of tires a decrease in the price of cars an increase in consumer income an increase in the number of miles people drive per yeararrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education