ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

4 . Conditions for monopolistic competition

PLEASE HELP ME

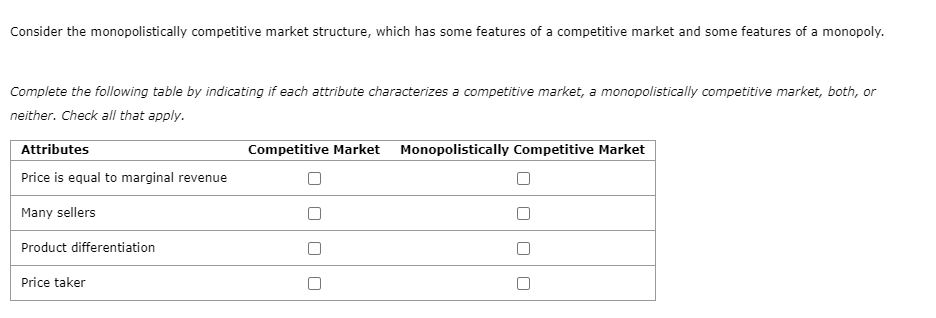

Transcribed Image Text:Consider the monopolistically competitive market structure, which has some features of a competitive market and some features of a monopoly.

Complete the following table by indicating if each attribute characterizes a competitive market, a monopolistically competitive market, both, or

neither. Check all that apply.

Attributes

Competitive Market Monopolistically Competitive Market

Price is equal to marginal revenue

Many sellers

Product differentiation

Price taker

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Price and costs Consider the diagram below depicting the demand and cost conditions faced by a monopolistically competitive firm. a. Use the graph to show how price and output will vary depending upon which point the firm produces. Indicate the levels that will be produced under profit maximization, productive efficiency, and allocative efficiency. Instructions: (1) Use the tool provided 'Profit maximizing' to plot a point showing the price-quantity combination when the firm is maximizing profit. (2) Use the tool provided 'Productive efficiency' to plot a point showing the price-quantity combination when the firm is producing the productively efficient output level. (3) Use the tool provided 'Allocative efficiency' to plot a point showing the price-quantity combination when the firm is producing the allocatively efficient output level. Demand MR Quantity MC Tools -9 --i Productive eff Profit maximiz ATC Allocative effiarrow_forwardls uccess Tips ■ccess Tips NOUT Actumpto Koup the Highest/3 3. Is monopolistic competition efficient? Suppose that a firm produces baseball bats in a monopolistically competitive market. The following graph shows its demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. PRICE (Dollars par bat) 80 70 60 20 MO о о 10 20 40 ATC 60 QUANTITY (Thousands of bas) Demand Man Camp Outcome Min Unit Cost Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that optimal quantity. Furthermore, the quantity the firm produces in long-run equilibrium is average total cost. at the the quantity at which…arrow_forward1.How short-run profit or losses induce entry or exit Fantastique Bikes is a company that manufactures bikes in a monopolistically competitive market. The following graph shows Fantastique's demand curve, marginal revenue curve (MR), marginal cost curve (MC), and average total cost curve (ATC).on the graph to indicate the short-run profit-maximizing price and quantity for this monopolistically competitive company. PLEASE HELP MEarrow_forward

- 1. Briefly discuss the various ways monopolistically competitive firms can differentiate their products? 2. In the long-run, a perfectly competitive firm will earn what kind of economic profit?arrow_forwardPlease only Typing answer I need ASAParrow_forwardWhich of these markets is most likely to be identified as monopolistic competition? Group of answer choices a. shoes b. corn c. gasoline d. shoes, corn and gasoline are all like monopolistic competitionarrow_forward

- Which of the following is an example of a monopolistically competitive industry A. wheat farming B. the local electricity producer C. colleges and universities D. the domestic auto industryarrow_forwarddraw and explain a diagram to show the long run equilibrium in a monopolistically competitive market.how does this equilibrium differ from that in a perfectly competitive market?arrow_forwardI need both answers typing no chatgptarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education